20 kroner (Gustav Vigeland's birth) – Norway

Add to wishlist

Circulating commemorative coins

Commemoration: 150th anniversary of Gustav Vigeland’s birth

Norway

Context

Material

References

KM: #

Numista: #165606

Value

Exchange value: 20 NOK

Inflation-adjusted value: 25.09 NOK

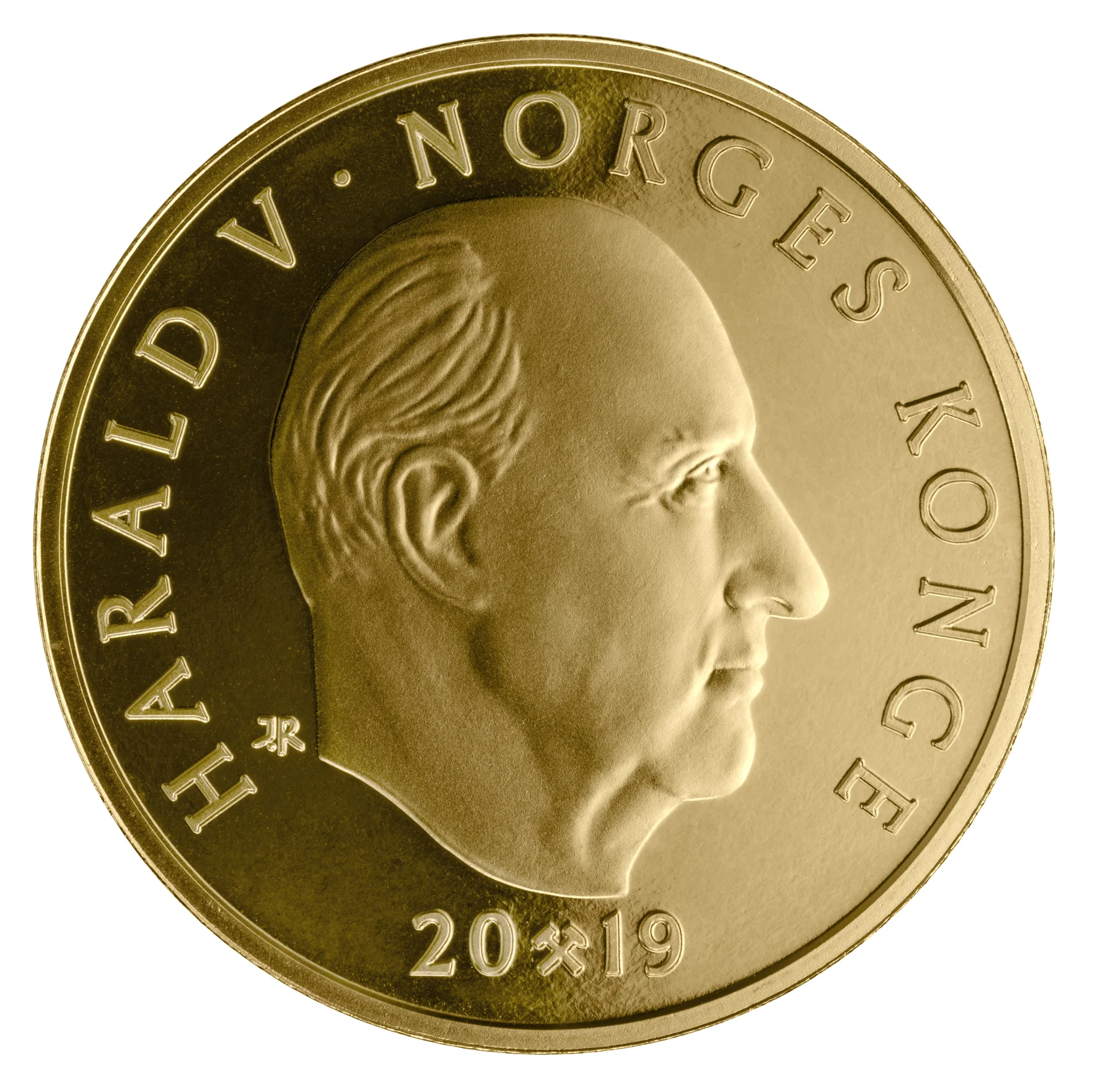

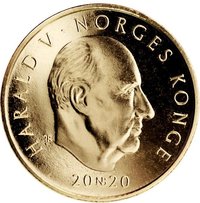

Obverse

Description:

Bust of King Harald V facing right, with engraver's initials behind it. Inscription surrounds the bust, and a mintmark divides the date below. Solid ring on the rim.

Inscription:

HARALD V · NORGES KONGE

IAR

20 ⚒ 19

IAR

20 ⚒ 19

Translation:

HAROLD V · NORWAY'S KING

IAR

20 ⚒ 19

IAR

20 ⚒ 19

Script: Latin

Engraver: Ingrid Austlid Rise

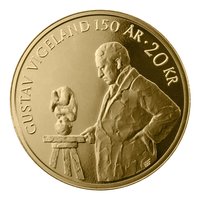

Reverse

Description:

Vigeland contemplating his sculpture "The Foetus," facing left. Inscription and value above; designer's initials on his coat. Solid ring on rim.

Inscription:

GUSTAV VIGELAND 150 ÅR · 20 KR

HAF

HAF

Translation:

Gustav Vigeland 150 Years · 20 Krone

Haf

Haf

Script: Latin

Language: Norwegian

Engraver: Ingrid Austlid Rise

Designer: Håkon Anton Fagerås

Edge

Plain

Categories

| Art> Sculpture |

| Event> Birth anniversary |

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2019 | — | 1,000,000 | ||

| 2019 | — | 2,240 | Proof |

Historical background

In 2019, the Norwegian krone (NOK) experienced a period of significant weakness, reaching historically low levels against both the euro and the US dollar. The primary driver was the monetary policy divergence between Norges Bank, which was in a tightening cycle, and other major central banks that were cutting rates or maintaining ultra-loose policy. Despite Norway's solid economic fundamentals, including low unemployment and high household wealth, the krone failed to strengthen as investors sought higher yields elsewhere, particularly in US dollar assets.

This depreciation was exacerbated by external factors, including global trade tensions and concerns over slowing worldwide growth, which dampened risk appetite and impacted small, open economies like Norway. Furthermore, while oil prices were relatively stable, they did not provide the traditional boost to the currency, as the petroleum sector's direct influence on the krone appeared to be diminishing over time. The weak krone became a key topic for both businesses and households, increasing import costs and travel expenses while benefiting export-oriented industries.

In response, Norges Bank continued its cautious interest rate hikes throughout the year, raising its key policy rate four times to 1.50% by December. The bank explicitly cited the weak krone as a contributing factor to inflation, justifying further tightening to anchor inflation expectations and fulfill its mandate. Consequently, 2019 was characterized by a puzzling disconnect between Norway's strong domestic economy and its underperforming currency, with policymakers walking a fine line between supporting growth and managing inflationary pressures from the depreciated exchange rate.

This depreciation was exacerbated by external factors, including global trade tensions and concerns over slowing worldwide growth, which dampened risk appetite and impacted small, open economies like Norway. Furthermore, while oil prices were relatively stable, they did not provide the traditional boost to the currency, as the petroleum sector's direct influence on the krone appeared to be diminishing over time. The weak krone became a key topic for both businesses and households, increasing import costs and travel expenses while benefiting export-oriented industries.

In response, Norges Bank continued its cautious interest rate hikes throughout the year, raising its key policy rate four times to 1.50% by December. The bank explicitly cited the weak krone as a contributing factor to inflation, justifying further tightening to anchor inflation expectations and fulfill its mandate. Consequently, 2019 was characterized by a puzzling disconnect between Norway's strong domestic economy and its underperforming currency, with policymakers walking a fine line between supporting growth and managing inflationary pressures from the depreciated exchange rate.

🌱 Fairly Common