Obverse

Description:

A child left of a crescent, behind the text.

Inscription:

SUOMI

FINLAND

M 20 €

FINLAND

M 20 €

Translation:

Finland

20 €

20 €

Engraver: Roope Määttä

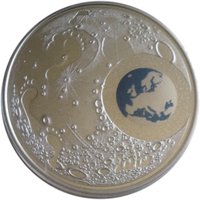

Reverse

Edge

Plain.

Categories

| Map |

Mints

| Name | Mark |

|---|---|

| Mint of Finland | M |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2010 | — | 10,000 | Proof | |

| 2010 | M | 3,500 |

Historical background

In 2010, Finland was a full member of the Eurozone, having adopted the euro as its sole legal tender in 2002. The country's currency situation was therefore intrinsically tied to the monetary policy of the European Central Bank (ECB), which set interest rates and managed the euro for the entire currency bloc. For Finland, this meant relinquishing independent control over its monetary policy, but it also provided stability and eliminated exchange rate risk within its key European trading partners. The Finnish economy, heavily export-dependent on sectors like technology (notably Nokia) and forestry, was influenced by the euro's external value against other major currencies.

The year 2010 was dominated by the aftermath of the global financial crisis and the escalating European sovereign debt crisis. While Finland itself maintained a relatively strong fiscal position with low public debt, the stability of the euro was under severe strain due to the crises in Greece, Ireland, and other peripheral Eurozone nations. This created a challenging environment for Finnish economic policy, as the government had to navigate domestic recessionary pressures while also participating in contentious EU-wide debates about bailout mechanisms and financial stability funds to protect the common currency.

Domestically, the Finnish markka (FIM) was a distant memory for everyday transactions, but the euro's performance was a topic of economic discussion. The euro's depreciation during the debt crisis provided a competitive boost for Finnish exports outside the Eurozone, aiding a fragile recovery. However, the overarching narrative was one of vulnerability to external Eurozone shocks, setting the stage for Finland's later, often stringent, stance during the debt crisis negotiations, driven by a desire to ensure the long-term stability of the currency it had fully embraced.

The year 2010 was dominated by the aftermath of the global financial crisis and the escalating European sovereign debt crisis. While Finland itself maintained a relatively strong fiscal position with low public debt, the stability of the euro was under severe strain due to the crises in Greece, Ireland, and other peripheral Eurozone nations. This created a challenging environment for Finnish economic policy, as the government had to navigate domestic recessionary pressures while also participating in contentious EU-wide debates about bailout mechanisms and financial stability funds to protect the common currency.

Domestically, the Finnish markka (FIM) was a distant memory for everyday transactions, but the euro's performance was a topic of economic discussion. The euro's depreciation during the debt crisis provided a competitive boost for Finnish exports outside the Eurozone, aiding a fragile recovery. However, the overarching narrative was one of vulnerability to external Eurozone shocks, setting the stage for Finland's later, often stringent, stance during the debt crisis negotiations, driven by a desire to ensure the long-term stability of the currency it had fully embraced.

Series: Éthique

💎 Very Rare