50 toea (Bank of Papua New Guinea) – Papua New Guinea

Add to wishlist

Circulating commemorative coins

Commemoration: 25th Anniversary of the Bank of Papua New Guinea

Papua New Guinea

Context

Material

Diameter: 30 mm

Weight: 13.63 g

Thickness: 2.65 mm

Shape: Equilateral curve heptagon

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #15406

Value

Exchange value: 0.50 PGK

Obverse

Description:

A bird-of-paradise above a spear and kundu drum.

Inscription:

PAPUA NEW GUINEA

1998

1998

Script: Latin

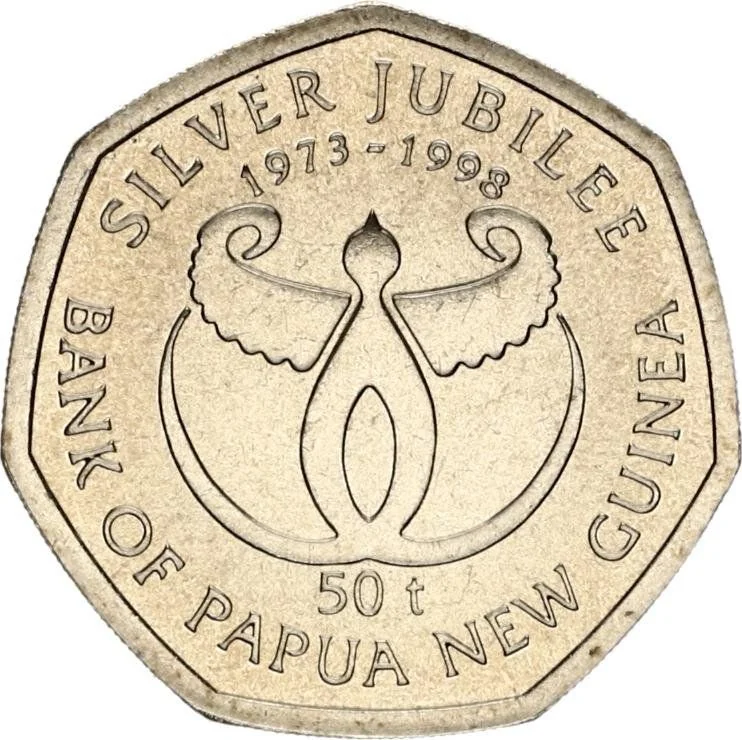

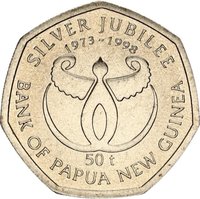

Reverse

Description:

Paradise Bird

Inscription:

SILVER JUBILEE

1973 - 1998

50t

BANK OF PAPUA NEW GUINEA

1973 - 1998

50t

BANK OF PAPUA NEW GUINEA

Script: Latin

Edge

Milled

Categories

| Animal> Bird |

| Art> Music |

| Object> Cold weapons |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1998 | — | — |

Historical background

In 1998, Papua New Guinea (PNG) faced a severe currency crisis, with the kina (PGK) experiencing a dramatic and rapid devaluation. The crisis was precipitated by a combination of external shocks and deep-seated domestic economic weaknesses. A sharp decline in global commodity prices, particularly for key exports like copper, gold, coffee, and palm oil, severely reduced foreign exchange earnings. This was exacerbated by a severe drought induced by the El Niño weather pattern, which crippled agricultural production and hydroelectric power, further straining the economy and investor confidence.

Domestically, the situation was worsened by significant fiscal indiscipline and political instability. The government was running large budget deficits, financed in part by monetary expansion from the Bank of Papua New Guinea. This led to high inflation and eroded the kina's value. Furthermore, a loss of confidence, both internationally and domestically, triggered capital flight and speculative pressure against the currency. Despite the central bank's efforts to defend a managed float by depleting its foreign reserves, market forces overwhelmed the kina, forcing a major devaluation.

The government's initial response, under Prime Minister Bill Skate, was controversial and counterproductive. In June 1998, it imposed a currency "lock," effectively fixing the kina at an overvalued official rate while a vastly depreciated black market flourished. This created a crippling foreign exchange shortage, stranding imports and crippling businesses. Following intense pressure from the International Monetary Fund (IMF) and the resignation of the central bank governor, the government abandoned the lock in September 1998. The kina was allowed to float freely, leading to an immediate and sharp depreciation but eventually restoring some market equilibrium and paving the way for an IMF structural adjustment program.

Domestically, the situation was worsened by significant fiscal indiscipline and political instability. The government was running large budget deficits, financed in part by monetary expansion from the Bank of Papua New Guinea. This led to high inflation and eroded the kina's value. Furthermore, a loss of confidence, both internationally and domestically, triggered capital flight and speculative pressure against the currency. Despite the central bank's efforts to defend a managed float by depleting its foreign reserves, market forces overwhelmed the kina, forcing a major devaluation.

The government's initial response, under Prime Minister Bill Skate, was controversial and counterproductive. In June 1998, it imposed a currency "lock," effectively fixing the kina at an overvalued official rate while a vastly depreciated black market flourished. This created a crippling foreign exchange shortage, stranding imports and crippling businesses. Following intense pressure from the International Monetary Fund (IMF) and the resignation of the central bank governor, the government abandoned the lock in September 1998. The kina was allowed to float freely, leading to an immediate and sharp depreciation but eventually restoring some market equilibrium and paving the way for an IMF structural adjustment program.

🌱 Fairly Common