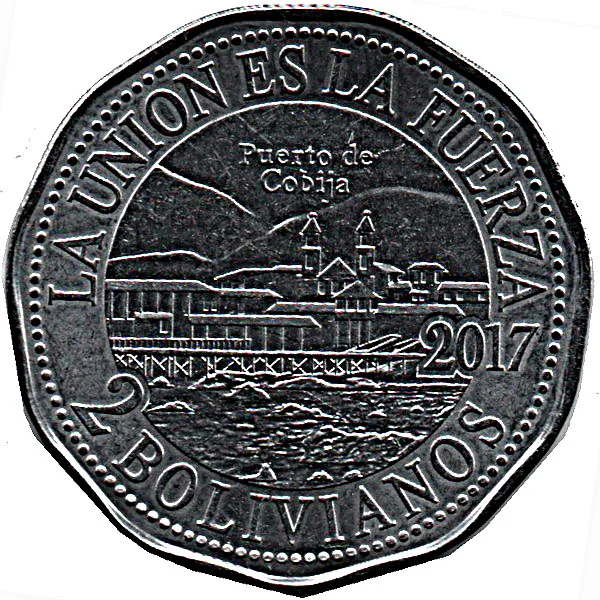

2 bolivianos – Bolivia

Add to wishlist

Circulating commemorative coins

Commemoration: Puerto de Cobija

Bolivia

Context

Year: 2017

Issuer: Bolivia

Issuing organization: Central Bank of Bolivia

Period:

(since 2009)

Currency:

(since 1986)

Total mintage: 4,200,000

Material

Diameter: 29 mm

Weight: 6.4 g

Thickness: 1.4 mm

Shape: Hendecagonal

Composition: Stainless steel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #130204

Value

Exchange value: 2 BOB

Obverse

Reverse

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Mint of Poland | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2017 | — | 4,200,000 |

Historical background

In 2017, Bolivia's currency situation was characterized by notable stability, especially when contrasted with the volatility experienced by many of its regional neighbors. This stability was primarily anchored by a decade of sustained economic growth, prudent fiscal management under President Evo Morales, and significant foreign currency reserves accumulated from high natural gas exports. The Boliviano (BOB) maintained a stable and predictable exchange rate, officially pegged to a basket of currencies but effectively closely managed against the US dollar by the Central Bank of Bolivia (BCB). This managed float, supported by direct intervention in the forex market, kept inflation low and bolstered public confidence in the national currency.

However, this stability was maintained through increasingly costly interventions. As global commodity prices softened from earlier highs, Bolivia began running persistent trade and fiscal deficits, steadily depleting its foreign reserves. The central bank's strategy of selling dollars to support the Boliviano, while successful in the short term, was recognized by economists as unsustainable in the long run without a correction in the country's economic fundamentals. Concerns grew about the rising public debt and the overvaluation of the Boliviano, which hurt the competitiveness of non-hydrocarbon exports like manufacturing and agriculture.

Despite these underlying pressures, for the average Bolivian in 2017, the currency situation remained broadly positive. The strong and stable Boliviano preserved purchasing power and macroeconomic calm, a key political achievement for the government. Nevertheless, analysts and international institutions like the IMF increasingly flagged the dwindling reserves as a vulnerability, warning that the country's economic model required adjustment to avoid future balance-of-payments pressures. Thus, 2017 represented a period of apparent calm but mounting underlying tensions regarding Bolivia's currency and economic sustainability.

However, this stability was maintained through increasingly costly interventions. As global commodity prices softened from earlier highs, Bolivia began running persistent trade and fiscal deficits, steadily depleting its foreign reserves. The central bank's strategy of selling dollars to support the Boliviano, while successful in the short term, was recognized by economists as unsustainable in the long run without a correction in the country's economic fundamentals. Concerns grew about the rising public debt and the overvaluation of the Boliviano, which hurt the competitiveness of non-hydrocarbon exports like manufacturing and agriculture.

Despite these underlying pressures, for the average Bolivian in 2017, the currency situation remained broadly positive. The strong and stable Boliviano preserved purchasing power and macroeconomic calm, a key political achievement for the government. Nevertheless, analysts and international institutions like the IMF increasingly flagged the dwindling reserves as a vulnerability, warning that the country's economic model required adjustment to avoid future balance-of-payments pressures. Thus, 2017 represented a period of apparent calm but mounting underlying tensions regarding Bolivia's currency and economic sustainability.

🌱 Common