100 Zlotys – Poland

Non-circulating coins

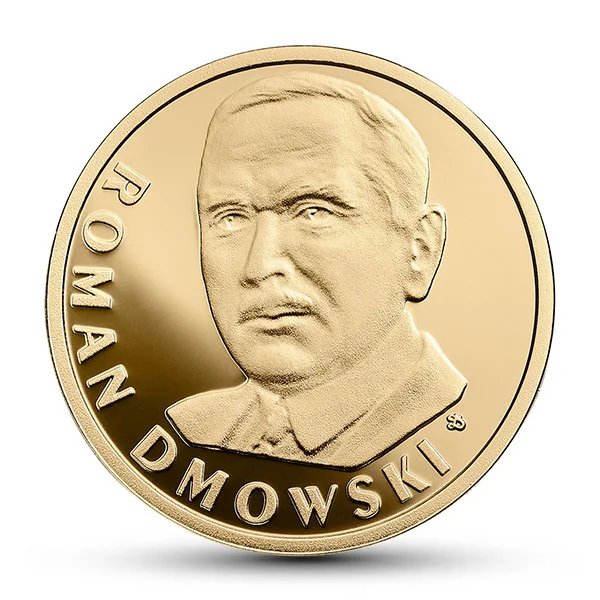

Commemoration: Roman Dmowski

Poland

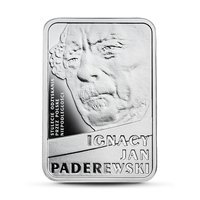

Obverse

Inscription:

RZECZPOSPOLITA POLSKA

2017

mw

100 ZŁ

2017

mw

100 ZŁ

Translation:

REPUBLIC OF POLAND

2017

mw

100 ZŁOTYCH

2017

mw

100 ZŁOTYCH

Script: Latin

Language: Polish

Designer: Dobrochna Surajewska

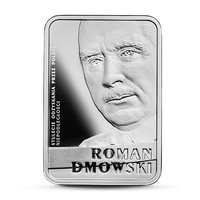

Reverse

Edge

Plain with inscription

Legend:

Stulecie odzyskania przez Polskę niepodległości

Translation:

Centenary of Poland regaining independence

Language: Polish

Categories

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Mint of Poland | (MW) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2017 | MW | 2,000 | Proof |

Historical background

In 2017, Poland's currency, the złoty (PLN), experienced a period of notable appreciation and stability against major currencies like the euro and the US dollar, largely driven by strong economic fundamentals. The year began with the złoty trading at approximately 4.35 to the euro, and it strengthened steadily, breaking the psychologically important 4.20 level by mid-year and ending around 4.18. This robust performance was underpinned by Poland's solid GDP growth (over 4.5% for the year), low unemployment, rising wages, and stable inflation within the National Bank of Poland's (NBP) target range. Furthermore, the country maintained an investment-grade credit rating, attracting consistent foreign capital inflows.

The political and monetary policy landscape played a significant role in shaping market sentiment. Domestically, the ruling Law and Justice (PiS) party's policies, while controversial in the EU, did not trigger the capital flight some investors had initially feared. Internationally, the relative calm in European markets following the 2016 Brexit vote and the French elections reduced risk aversion towards Central and Eastern European currencies. Crucially, the NBP under Governor Adam Glapiński maintained a consistently dovish stance, keeping the key interest rate at a historic low of 1.5% throughout the year. This policy, aimed at supporting growth, also helped temper the złoty's strength to protect export competitiveness.

Despite the overall positive trend, the currency faced intermittent pressures from external factors and regional political concerns. Tensions within the EU regarding rule-of-law issues and the migrant quota dispute created episodes of volatility, reminding markets of geopolitical risks. Additionally, the strength of the złoty became a topic of discussion for exporters, who argued it eroded their profit margins. Nevertheless, 2017 closed as a year of resilience for the złoty, reflecting Poland's economic maturity and its relative safe-haven status within the emerging European landscape, even as observers watched for potential headwinds from EU relations and the eventual start of monetary policy normalization abroad.

The political and monetary policy landscape played a significant role in shaping market sentiment. Domestically, the ruling Law and Justice (PiS) party's policies, while controversial in the EU, did not trigger the capital flight some investors had initially feared. Internationally, the relative calm in European markets following the 2016 Brexit vote and the French elections reduced risk aversion towards Central and Eastern European currencies. Crucially, the NBP under Governor Adam Glapiński maintained a consistently dovish stance, keeping the key interest rate at a historic low of 1.5% throughout the year. This policy, aimed at supporting growth, also helped temper the złoty's strength to protect export competitiveness.

Despite the overall positive trend, the currency faced intermittent pressures from external factors and regional political concerns. Tensions within the EU regarding rule-of-law issues and the migrant quota dispute created episodes of volatility, reminding markets of geopolitical risks. Additionally, the strength of the złoty became a topic of discussion for exporters, who argued it eroded their profit margins. Nevertheless, 2017 closed as a year of resilience for the złoty, reflecting Poland's economic maturity and its relative safe-haven status within the emerging European landscape, even as observers watched for potential headwinds from EU relations and the eventual start of monetary policy normalization abroad.

✨ Legendary