100 leva – Bulgaria

Add to wishlist

Bulgaria

Context

Material

References

Value

Bullion value: $25.35

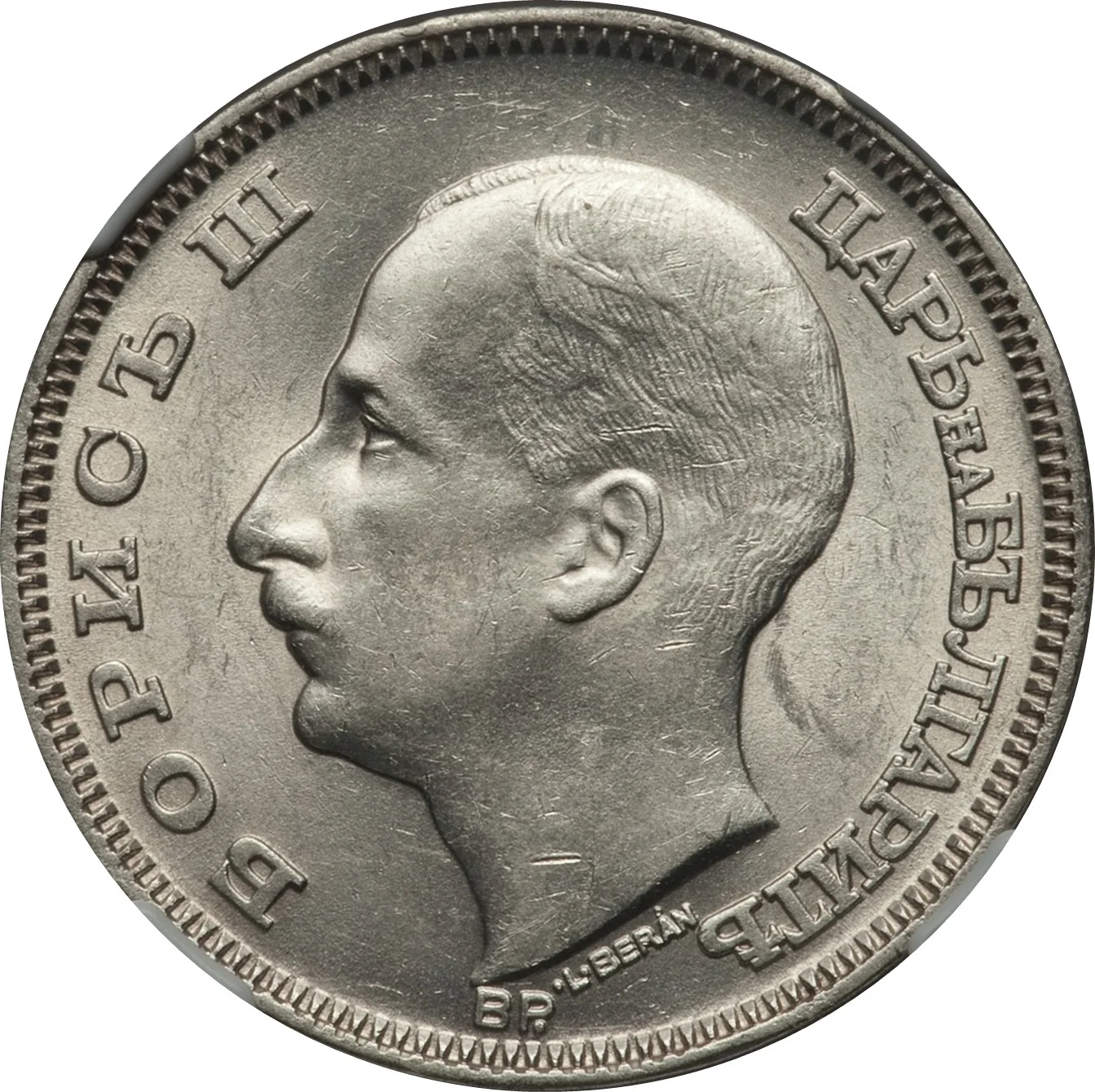

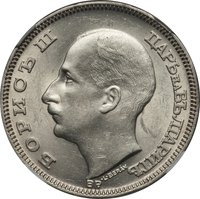

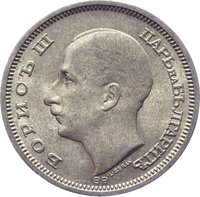

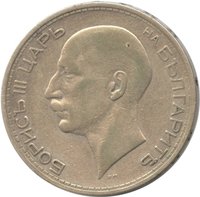

Obverse

Description:

Boris III (1894–1943), Tsar of Bulgaria, facing left.

Inscription:

БОРИСЪ III

ЦАРЬнаБЪЛГАРИТѢ

∙L∙BERÁN

BP.

ЦАРЬнаБЪЛГАРИТѢ

∙L∙BERÁN

BP.

Translation:

BORIS III

TSAR OF BULGARIA

L. BERÁN

BP.

TSAR OF BULGARIA

L. BERÁN

BP.

Script: Cyrillic

Engraver: Lajos Berán

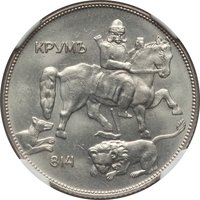

Reverse

Description:

Denomination above date in wreath.

Inscription:

100

ЛЕВА

1930

ЛЕВА

1930

Translation:

One Hundred Leva

1930

1930

Script: Cyrillic

Language: Bulgarian

Engraver: Lajos Berán

Edge

Smooth with inscription

Legend:

БОЖЕ ПАЗИ БЪЛГАРИЯ

Translation:

God Save Bulgaria

Language: Bulgarian

Categories

| Symbols> Coat of Arms |

| Person> Monarch |

Mints

| Name | Mark |

|---|---|

| Hungarian mint | BP |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1930 | BP | 1,556,000 |

Historical background

In 1930, Bulgaria’s currency situation was defined by the long shadow of the First World War and a subsequent severe economic crisis. The country had entered the 1920s with a heavily depreciated currency, the Bulgarian lev, due to wartime inflation and massive reparations imposed by the 1919 Treaty of Neuilly. A period of relative stabilization followed under the guidance of the Financial Committee of the League of Nations, culminating in the 1924 Currency Law which established a new gold-backed lev (zlatni leva), pegged to the French franc. By 1928, this reform appeared successful, having restored some international confidence and allowing Bulgaria to access foreign loans.

However, this stability was fragile and highly dependent on external capital flows. The onset of the Great Depression in 1929 rapidly exposed these vulnerabilities. Global commodity prices collapsed, devastating Bulgaria’s primarily agrarian export economy, which relied on tobacco, grain, and other agricultural products. This led to a sharp decline in foreign exchange earnings just as international credit markets froze. Consequently, the Bulgarian National Bank struggled to maintain the gold peg, as its reserves came under severe pressure from a growing balance of payments deficit and the withdrawal of foreign short-term capital.

By the end of 1930, Bulgaria was thus in a precarious transitional phase, still officially on the gold standard but facing unsustainable pressures. The government and the central bank implemented deflationary policies and import restrictions in a desperate attempt to defend the peg, but these measures only deepened domestic economic hardship. The situation would deteriorate further in the early 1930s, leading to the inevitable abandonment of the gold standard in 1931 and a return to a managed, depreciated currency, marking the end of the brief era of monetary stability inaugurated in the mid-1920s.

However, this stability was fragile and highly dependent on external capital flows. The onset of the Great Depression in 1929 rapidly exposed these vulnerabilities. Global commodity prices collapsed, devastating Bulgaria’s primarily agrarian export economy, which relied on tobacco, grain, and other agricultural products. This led to a sharp decline in foreign exchange earnings just as international credit markets froze. Consequently, the Bulgarian National Bank struggled to maintain the gold peg, as its reserves came under severe pressure from a growing balance of payments deficit and the withdrawal of foreign short-term capital.

By the end of 1930, Bulgaria was thus in a precarious transitional phase, still officially on the gold standard but facing unsustainable pressures. The government and the central bank implemented deflationary policies and import restrictions in a desperate attempt to defend the peg, but these measures only deepened domestic economic hardship. The situation would deteriorate further in the early 1930s, leading to the inevitable abandonment of the gold standard in 1931 and a return to a managed, depreciated currency, marking the end of the brief era of monetary stability inaugurated in the mid-1920s.

Series: 1930 Bulgaria circulation coins

🌱 Common