1 Salung – Thailand

Thailand

Context

Years: 1917–1925

Issuer: Thailand

Ruler: Phra Mongkut Klao

Currency:

(since 1897)

Demonetized: Yes

Total mintage: 13,230,000

Material

References

Y: #Click to copy to clipboard43a

Numista: #12234

Value

Exchange value: 0.25 THB = $0.01

Bullion value: $7.04

Obverse

Reverse

Edge

Reeded

Categories

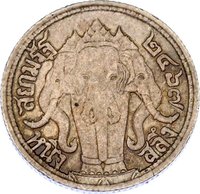

| Animal> Elephant |

| Mythology> Fantastic animal |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1917 | — | 1,100,000 | ||

| 1918 | — | 2,170,000 | ||

| 1919 | — | 7,860,000 | ||

| 1924 | — | 2,100,000 | ||

| 1925 | — | — |

Historical background

In 1917, Thailand, then known as Siam, operated under a complex bimetallic system that was under significant strain due to the global economic disruptions of World War I. The official currency was the baht, defined in law as a specific weight of silver. However, the country also circulated a substantial amount of gold coinage, the tical, creating a de facto dual system. The war caused a sharp rise in the global price of silver, leading to a critical problem: the intrinsic silver value of the baht coins began to exceed their face value. This created a powerful incentive for individuals to melt down or export silver coins for bullion, threatening to drain the kingdom's silver currency from circulation entirely.

To avert a monetary crisis, King Vajiravudh (Rama VI) enacted the Currency Act of 1918 (B.E. 2461), which was prepared and took legal effect from late 1917. This pivotal legislation fundamentally reformed the system by abandoning the silver standard. It established the baht as a decimalized, unitary currency and moved the country onto a gold exchange standard. The law pegged the baht to the British pound sterling at a fixed rate of 13 baht to 1 pound, which indirectly linked it to gold. Crucially, the new baht notes and subsidiary coins issued were token money—their face value was higher than their metallic content, eliminating the profit from melting them down.

This reform, conceived in the pressing circumstances of 1917, was a landmark in Thai economic history. It successfully stabilized the currency, ended the speculative outflow of silver, and modernized the monetary system by centralizing control under the government (later the Bank of Thailand). The move tied Siam's economy more closely to the British-dominated global financial system and laid the institutional foundation for the modern Thai baht, securing monetary stability as the country navigated the turbulent post-war era.

To avert a monetary crisis, King Vajiravudh (Rama VI) enacted the Currency Act of 1918 (B.E. 2461), which was prepared and took legal effect from late 1917. This pivotal legislation fundamentally reformed the system by abandoning the silver standard. It established the baht as a decimalized, unitary currency and moved the country onto a gold exchange standard. The law pegged the baht to the British pound sterling at a fixed rate of 13 baht to 1 pound, which indirectly linked it to gold. Crucially, the new baht notes and subsidiary coins issued were token money—their face value was higher than their metallic content, eliminating the profit from melting them down.

This reform, conceived in the pressing circumstances of 1917, was a landmark in Thai economic history. It successfully stabilized the currency, ended the speculative outflow of silver, and modernized the monetary system by centralizing control under the government (later the Bank of Thailand). The move tied Siam's economy more closely to the British-dominated global financial system and laid the institutional foundation for the modern Thai baht, securing monetary stability as the country navigated the turbulent post-war era.

🌱 Fairly Common