1 shilling – Kenya

Add to wishlist

Kenya

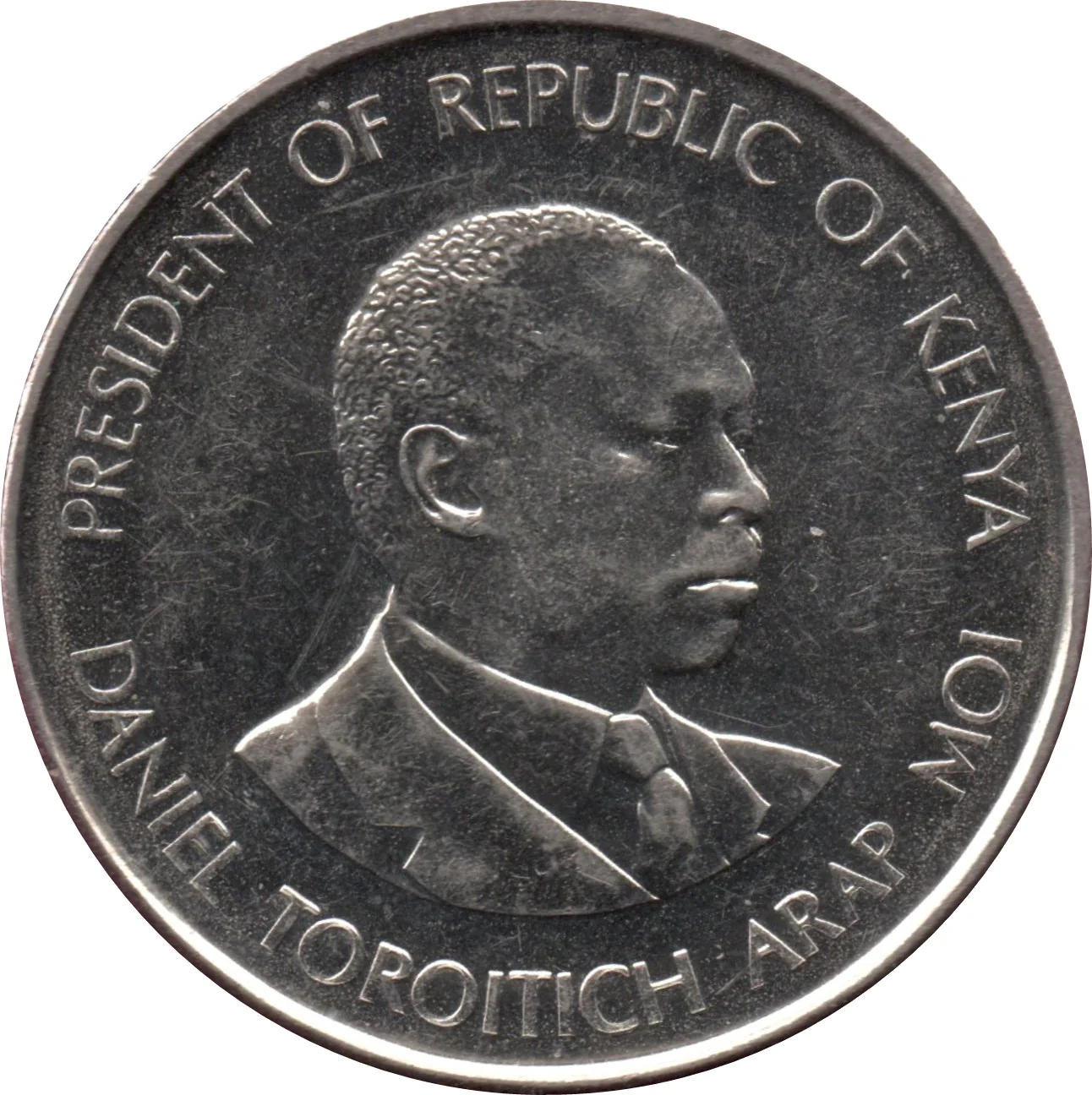

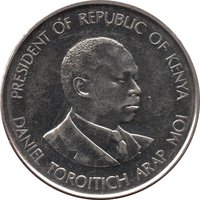

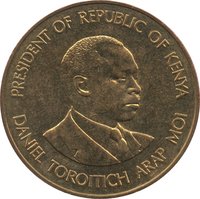

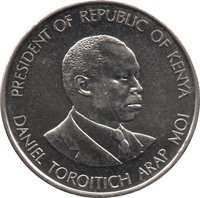

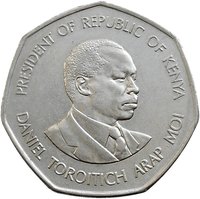

Obverse

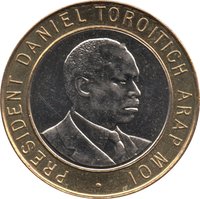

Reverse

Description:

Bust of Daniel Arap Moi facing right.

Inscription:

PRESIDENT OF REPUBLIC OF KENYA

DANIEL TOROITICH ARAP MOI

DANIEL TOROITICH ARAP MOI

Script: Latin

Edge

Reeded

Categories

| Person> Politician |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1994 | — | — |

Historical background

In 1994, Kenya's currency situation was characterized by a managed float of the Kenyan Shilling (KES) under significant pressure, marking a pivotal moment in the country's economic liberalization. Following a major foreign exchange crisis in the early 1990s, the government had abandoned the fixed exchange rate system in 1993 and dissolved the notorious "forex bureaus" that had fueled a parallel black market. The Central Bank of Kenya (CBK) introduced a "retention scheme" and a formal interbank foreign exchange market, allowing the shilling's value to be determined more by market forces, though with substantial official intervention to prevent excessive volatility.

The year saw the shilling depreciate steadily, driven by underlying economic weaknesses. Key pressures included a large and persistent current account deficit, dwindling foreign exchange reserves, and high inflation which eroded the currency's domestic purchasing power. Furthermore, the withdrawal of direct budget support by the International Monetary Fund (IMF) and other donors in late 1993, due to governance concerns and a lack of economic reforms, strained Kenya's external position. This lack of donor inflows exacerbated the shortage of hard currency, forcing the CBK to spend reserves to defend the shilling.

Consequently, 1994 was a year of difficult adjustment. The depreciation, while necessary for correcting imbalances, increased the cost of imports and servicing the country's external debt, contributing to domestic economic hardship. The situation underscored the challenges of transitioning from a controlled to a more market-oriented regime without robust macroeconomic stability. The currency pressures of this period ultimately reinforced the need for the structural and governance reforms that would be more forcefully pursued in subsequent years under donor conditionalities.

The year saw the shilling depreciate steadily, driven by underlying economic weaknesses. Key pressures included a large and persistent current account deficit, dwindling foreign exchange reserves, and high inflation which eroded the currency's domestic purchasing power. Furthermore, the withdrawal of direct budget support by the International Monetary Fund (IMF) and other donors in late 1993, due to governance concerns and a lack of economic reforms, strained Kenya's external position. This lack of donor inflows exacerbated the shortage of hard currency, forcing the CBK to spend reserves to defend the shilling.

Consequently, 1994 was a year of difficult adjustment. The depreciation, while necessary for correcting imbalances, increased the cost of imports and servicing the country's external debt, contributing to domestic economic hardship. The situation underscored the challenges of transitioning from a controlled to a more market-oriented regime without robust macroeconomic stability. The currency pressures of this period ultimately reinforced the need for the structural and governance reforms that would be more forcefully pursued in subsequent years under donor conditionalities.

Series: 1994 series

🌱 Common