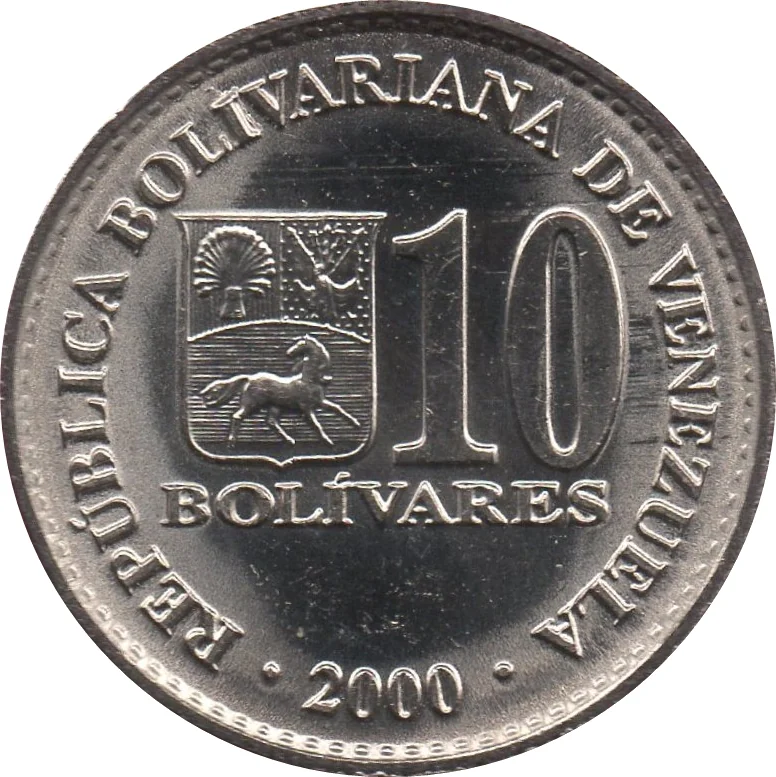

10 bolivars – Venezuela

Add to wishlist

Venezuela

Obverse

Reverse

Edge

Reeded

Categories

| Animal> Horse |

| Person> Military leader |

| Person> Politician |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Casa de la Moneda de Venezuela | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2000 | — | 80,000,000 | ||

| 2001 | — | 70,000,000 | ||

| 2002 | — | — |

Historical background

In 2000, Venezuela's currency situation was one of relative stability, but it existed in the fragile calm between two major periods of crisis. The national currency, the bolívar, operated under a controlled exchange rate regime established in the 1980s. While the country had experienced a banking crisis and capital flight in 1994-95, the high oil prices of 1999-2000 provided a crucial buffer. President Hugo Chávez, who took office in 1999, benefited from this petroleum-driven influx of dollars, which helped maintain the bolívar's official peg and kept foreign reserves adequate, preventing immediate currency pressure.

However, underlying this stability were significant structural vulnerabilities. The economy was already highly dependent on oil exports, and the manufacturing sector had been in decline for years, leading to a growing reliance on imports. Furthermore, the Chávez government began implementing its "Bolivarian Revolution," including a new constitution in 1999 and increased state spending on social programs. While not yet causing hyperinflation, these policies, combined with a fixed exchange rate, sowed the seeds for future distortions by expanding the money supply without corresponding productivity gains.

Consequently, the year 2000 represented a critical inflection point. The temporary relief provided by high oil prices masked the long-term consequences of policy choices and economic imbalances. The rigid exchange control system (known as CADIVI) would be formally instituted in 2003 in response to a severe crisis, but the foundations for that future turmoil—including fiscal deficits, a weakening productive apparatus, and growing political uncertainty—were already perceptible beneath the surface of the stable bolívar in 2000.

However, underlying this stability were significant structural vulnerabilities. The economy was already highly dependent on oil exports, and the manufacturing sector had been in decline for years, leading to a growing reliance on imports. Furthermore, the Chávez government began implementing its "Bolivarian Revolution," including a new constitution in 1999 and increased state spending on social programs. While not yet causing hyperinflation, these policies, combined with a fixed exchange rate, sowed the seeds for future distortions by expanding the money supply without corresponding productivity gains.

Consequently, the year 2000 represented a critical inflection point. The temporary relief provided by high oil prices masked the long-term consequences of policy choices and economic imbalances. The rigid exchange control system (known as CADIVI) would be formally instituted in 2003 in response to a severe crisis, but the foundations for that future turmoil—including fiscal deficits, a weakening productive apparatus, and growing political uncertainty—were already perceptible beneath the surface of the stable bolívar in 2000.

Series: 2000 Venezuela circulation coins

🌱 Common