1000 dirhams – United Arab Emirates

Add to wishlist

Non-circulating coins

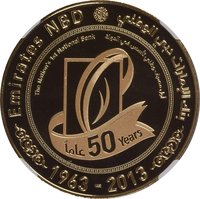

Commemoration: The Golden Jubilee of Emirates NBD

United Arab Emirates

Context

Year: 2013

Issuer: United Arab Emirates

Ruler: Khalifa bin Zayed Al Nahyan

Currency:

(since 1973)

Total mintage: 100

Material

References

KM: #

Numista: #91981

Value

Exchange value: 1000 AED

Bullion value: $5624.21

Obverse

Reverse

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2013 | — | 100 | Proof |

Historical background

In 2013, the United Arab Emirates' currency situation was defined by its long-standing and unwavering peg to the US dollar, established in 1997. The dirham was fixed at a rate of approximately AED 3.6725 per USD, a policy managed by the UAE Central Bank. This peg provided critical stability for the UAE's import-dependent, oil-exporting economy, anchoring inflation expectations and fostering a predictable environment for foreign investment and trade. It was a cornerstone of the country's economic policy, particularly as the UAE continued to solidify its position as a global hub for commerce, tourism, and finance.

The year saw the peg face indirect pressures from external monetary policy, specifically the US Federal Reserve's "taper tantrum." As the Fed signaled a potential rollback of its quantitative easing program, global capital flows shifted, strengthening the US dollar and, by extension, pulling the dirham higher alongside it. This created some economic headwinds, as a stronger dirham made the UAE's non-oil exports slightly less competitive and could dampen tourism from regions with weaker currencies. However, the domestic debate focused not on abandoning the peg, but on managing its side-effects and diversifying the economy to reduce vulnerability to dollar-linked shocks.

Ultimately, 2013 reinforced the UAE's commitment to the dollar peg as a strategic choice outweighing short-term fluctuations. The stability it offered was deemed essential for continued growth in banking, real estate, and major projects like Dubai's preparation for Expo 2020. Discussions around potentially pegging to a basket of currencies, which had surfaced after the 2008 financial crisis, remained on the periphery. The prevailing consensus was that the benefits of dollar stability—especially for a hydrocarbon economy with significant dollar-denominated revenues—far outweighed the costs, a position firmly backed by the UAE's substantial foreign exchange reserves.

The year saw the peg face indirect pressures from external monetary policy, specifically the US Federal Reserve's "taper tantrum." As the Fed signaled a potential rollback of its quantitative easing program, global capital flows shifted, strengthening the US dollar and, by extension, pulling the dirham higher alongside it. This created some economic headwinds, as a stronger dirham made the UAE's non-oil exports slightly less competitive and could dampen tourism from regions with weaker currencies. However, the domestic debate focused not on abandoning the peg, but on managing its side-effects and diversifying the economy to reduce vulnerability to dollar-linked shocks.

Ultimately, 2013 reinforced the UAE's commitment to the dollar peg as a strategic choice outweighing short-term fluctuations. The stability it offered was deemed essential for continued growth in banking, real estate, and major projects like Dubai's preparation for Expo 2020. Discussions around potentially pegging to a basket of currencies, which had surfaced after the 2008 financial crisis, remained on the periphery. The prevailing consensus was that the benefits of dollar stability—especially for a hydrocarbon economy with significant dollar-denominated revenues—far outweighed the costs, a position firmly backed by the UAE's substantial foreign exchange reserves.

✨ Legendary