50 cents – Hong Kong

Add to wishlist

China

Context

Years: 1977–1980

Country: China

Issuer: Hong Kong

Ruler: Elizabeth II

Currency:

(since 1863)

Total mintage: 310,641,000

Material

References

KM: #

Numista: #915

Value

Exchange value: 0.50 HKD

Obverse

Description:

Right-facing crowned bust.

Inscription:

QUEEN ELIZABETH THE SECOND

Script: Latin

Engraver: Arnold Machin

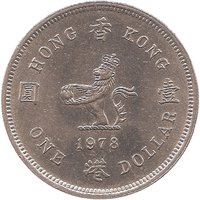

Reverse

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1977 | — | 60,001,000 | ||

| 1978 | — | 70,000,000 | ||

| 1979 | — | 60,640,000 | ||

| 1980 | — | 120,000,000 |

Historical background

In 1977, Hong Kong’s currency situation was defined by stability under a unique and long-standing colonial monetary system. The Hong Kong dollar was not issued by a central bank but by two commercial banks—The Hongkong and Shanghai Banking Corporation (HSBC) and the Chartered Bank—under a "Currency Board" system. This system required the full backing of note issuance with foreign exchange reserves, primarily sterling, ensuring a fixed exchange rate. Since 1935, the Hong Kong dollar had been pegged to sterling at a rate of HK$14.55 to £1, a link that provided predictability for trade and finance but also tied the colony’s monetary fate directly to the British pound.

This sterling peg, however, presented growing vulnerabilities by the late 1970s. The UK economy was struggling with high inflation and sterling had experienced significant volatility and depreciation throughout the 1970s, notably following the 1967 devaluation and the 1972 collapse of the Bretton Woods system. As a trading port with an economy increasingly linked to Asia and the United States, Hong Kong’s tether to a weakening sterling was problematic. It imported inflation from Britain and exposed local reserves to the pound’s decline, creating internal pressure to reconsider the anchor currency. This period saw Hong Kong’s economic gravity shifting away from Britain and towards the United States and Japan.

Consequently, 1977 was a pivotal year of transition, though the formal change would not occur until 1974. In fact, the critical shift had already happened in 1974 when the Hong Kong dollar was officially floated and delinked from sterling. By 1977, the currency was operating under a managed float, but the legacy of the sterling link and the management of the substantial sterling reserves accumulated under the old system remained active concerns. The government and financial institutions were navigating this new environment, setting the stage for the future landmark decision in 1983 to peg the Hong Kong dollar to the US dollar—a move that would ultimately restore the fixed exchange rate regime under a new and more relevant anchor.

This sterling peg, however, presented growing vulnerabilities by the late 1970s. The UK economy was struggling with high inflation and sterling had experienced significant volatility and depreciation throughout the 1970s, notably following the 1967 devaluation and the 1972 collapse of the Bretton Woods system. As a trading port with an economy increasingly linked to Asia and the United States, Hong Kong’s tether to a weakening sterling was problematic. It imported inflation from Britain and exposed local reserves to the pound’s decline, creating internal pressure to reconsider the anchor currency. This period saw Hong Kong’s economic gravity shifting away from Britain and towards the United States and Japan.

Consequently, 1977 was a pivotal year of transition, though the formal change would not occur until 1974. In fact, the critical shift had already happened in 1974 when the Hong Kong dollar was officially floated and delinked from sterling. By 1977, the currency was operating under a managed float, but the legacy of the sterling link and the management of the substantial sterling reserves accumulated under the old system remained active concerns. The government and financial institutions were navigating this new environment, setting the stage for the future landmark decision in 1983 to peg the Hong Kong dollar to the US dollar—a move that would ultimately restore the fixed exchange rate regime under a new and more relevant anchor.

🌱 Very Common