50 forint – Hungary

Add to wishlist

Circulating commemorative coins

Commemoration: Hungary in the European Union

Hungary

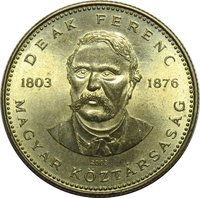

Obverse

Description:

EU Stars; Crowned Hungarian Shield

Inscription:

MAGYAR KÖZTÁRSASÁG

AZ EURÓPAI UNIÓ TAGJA

2004

AZ EURÓPAI UNIÓ TAGJA

2004

Translation:

HUNGARIAN REPUBLIC

MEMBER OF THE EUROPEAN UNION

2004

MEMBER OF THE EUROPEAN UNION

2004

Script: Latin

Language: Hungarian

Designer: István Kósa

Reverse

Edge

Plain

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Hungarian mint | BP. |

Historical background

In 2004, Hungary's currency situation was defined by the challenge of managing the forint (HUF) within a unique "soft peg" system known as the exchange rate band. The forint was not freely floating; instead, it was allowed to fluctuate within a ±15% band around a central parity against the euro. This mechanism, maintained by the National Bank of Hungary (MNB), aimed to provide stability and curb excessive volatility while gradually allowing for greater flexibility in preparation for eventual Eurozone membership, a key strategic goal following the country's EU accession in May 2004.

However, this period was marked by significant pressure. The economy faced large and persistent twin deficits—both a substantial fiscal budget deficit and a high current account deficit. These imbalances, fueled by strong domestic demand and consumer credit growth, led to concerns over sustainability and made the forint vulnerable to shifts in investor sentiment. Consequently, the MNB had to frequently intervene in foreign exchange markets and maintain high interest rates to defend the currency band and attract the capital inflows needed to finance the deficits, creating a tension between supporting growth and ensuring currency stability.

The situation culminated in a major crisis of confidence in early 2003, which forced a one-time 15.2% devaluation and a widening of the fluctuation band. By 2004, the system was stabilizing from this shock, but the underlying vulnerabilities remained. The focus was squarely on implementing fiscal consolidation measures to reduce the deficits, which was a prerequisite not only for maintaining the peg but also for meeting the Maastricht convergence criteria for euro adoption. Thus, the currency regime in 2004 was a transitional and fragile framework, under constant scrutiny from financial markets as Hungary navigated the post-EU accession landscape.

However, this period was marked by significant pressure. The economy faced large and persistent twin deficits—both a substantial fiscal budget deficit and a high current account deficit. These imbalances, fueled by strong domestic demand and consumer credit growth, led to concerns over sustainability and made the forint vulnerable to shifts in investor sentiment. Consequently, the MNB had to frequently intervene in foreign exchange markets and maintain high interest rates to defend the currency band and attract the capital inflows needed to finance the deficits, creating a tension between supporting growth and ensuring currency stability.

The situation culminated in a major crisis of confidence in early 2003, which forced a one-time 15.2% devaluation and a widening of the fluctuation band. By 2004, the system was stabilizing from this shock, but the underlying vulnerabilities remained. The focus was squarely on implementing fiscal consolidation measures to reduce the deficits, which was a prerequisite not only for maintaining the peg but also for meeting the Maastricht convergence criteria for euro adoption. Thus, the currency regime in 2004 was a transitional and fragile framework, under constant scrutiny from financial markets as Hungary navigated the post-EU accession landscape.

🌱 Common