20 Forint – Hungary

Circulating commemorative coins

Commemoration: Deák Ferenc

Hungary

Context

Material

References

KM: #Click to copy to clipboard768

Numista: #8623

Value

Exchange value: 20 HUF = $0.06

Inflation-adjusted value: 56.94 HUF

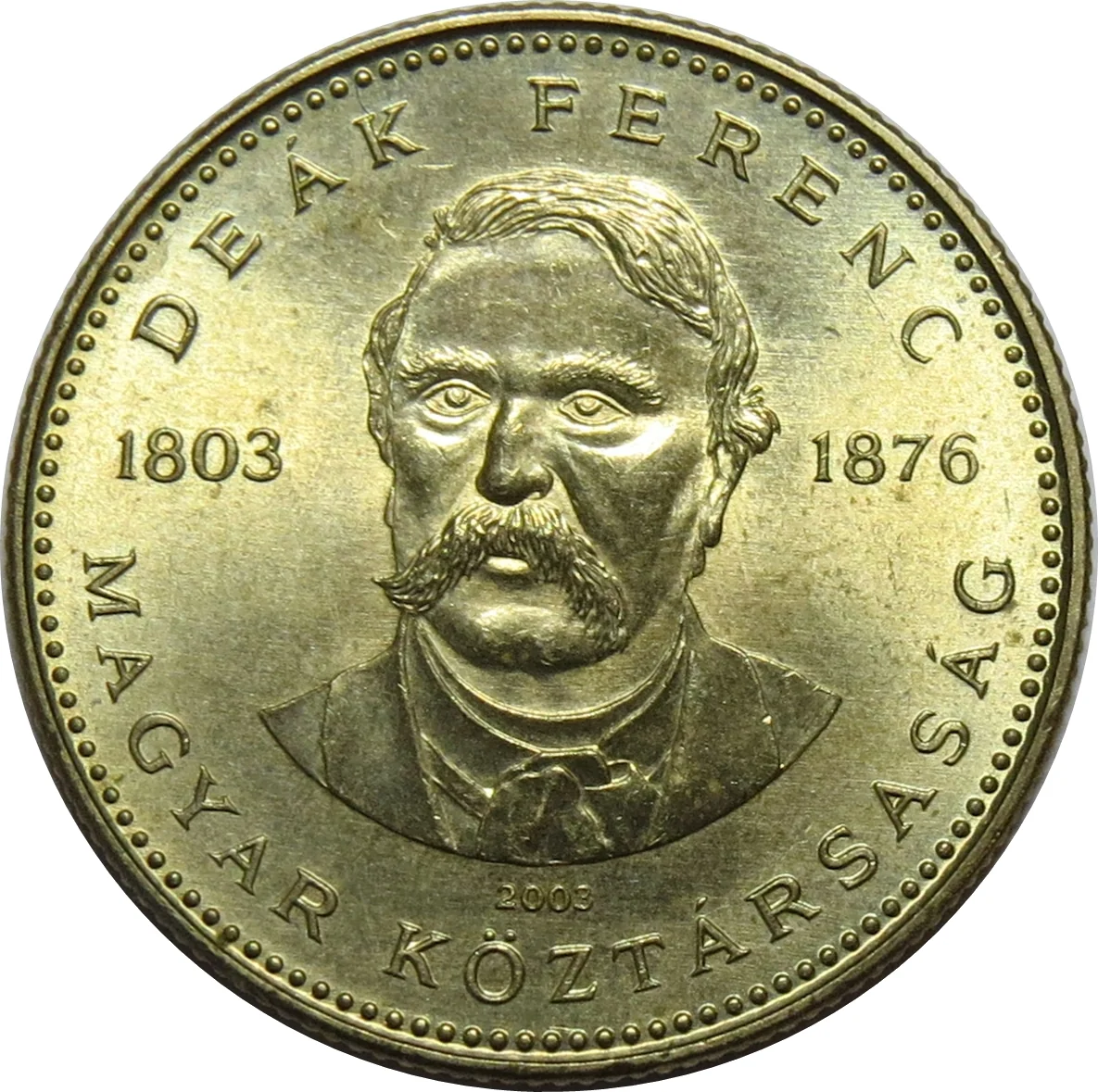

Obverse

Description:

Portrait of Ferenc Deák with his lifespan, and the issue date below.

Inscription:

DEÁK FERENC

1803 1876

2003

MAGYAR KÖZTÁRSASÁG

1803 1876

2003

MAGYAR KÖZTÁRSASÁG

Translation:

Francis Deák

1803 1876

2003

Hungarian Republic

1803 1876

2003

Hungarian Republic

Script: Latin

Language: Hungarian

Designer: István Kósa

Reverse

Description:

Value underlined, mintmark below.

Inscription:

20

FORINT

BP.

FORINT

BP.

Script: Latin

Designer: István Bartos

Edge

Reeded

Categories

| Event> Birth anniversary |

Mints

| Name | Mark |

|---|---|

| Hungarian mint | BP. |

Historical background

In 2003, Hungary's currency situation was defined by a managed floating exchange rate regime for the Hungarian Forint (HUF), operating within a wide ±15% band around a central parity against the Euro. This system, a remnant of earlier pre-EU accession stabilization efforts, aimed to balance exchange rate stability with the flexibility needed to absorb economic shocks. However, it created persistent tension, as the National Bank of Hungary (MNB) frequently intervened to prevent excessive volatility, particularly to curb forint appreciation driven by strong capital inflows from foreign investors attracted by high yields and the country's imminent EU accession.

The core economic challenge was a large and stubborn twin deficit—a substantial budget deficit alongside a significant current account deficit—which exerted downward pressure on the forint and fueled inflationary risks. To defend the currency and maintain macroeconomic stability, the MNB maintained a high benchmark interest rate (around 12.5% for much of the year), one of the highest in Central Europe. This "high interest rate, strong currency" policy was a double-edged sword: it helped control inflation and attract foreign capital but also stifled domestic economic growth and made Hungarian exports less competitive.

By the end of 2003, the system was under growing strain and scrutiny. The wide band was increasingly seen as incompatible with the requirements for future Eurozone membership, and market participants anticipated a regime change. Consequently, in a pivotal move, Hungary abandoned the fluctuation band in February 2008 and shifted to a fully free-floating exchange rate, a transition for which the turbulent dynamics of 2003 had set the stage.

The core economic challenge was a large and stubborn twin deficit—a substantial budget deficit alongside a significant current account deficit—which exerted downward pressure on the forint and fueled inflationary risks. To defend the currency and maintain macroeconomic stability, the MNB maintained a high benchmark interest rate (around 12.5% for much of the year), one of the highest in Central Europe. This "high interest rate, strong currency" policy was a double-edged sword: it helped control inflation and attract foreign capital but also stifled domestic economic growth and made Hungarian exports less competitive.

By the end of 2003, the system was under growing strain and scrutiny. The wide band was increasingly seen as incompatible with the requirements for future Eurozone membership, and market participants anticipated a regime change. Consequently, in a pivotal move, Hungary abandoned the fluctuation band in February 2008 and shifted to a fully free-floating exchange rate, a transition for which the turbulent dynamics of 2003 had set the stage.

🌱 Common