500 Nuevos Pesos – Uruguay

Uruguay

Context

Year: 1989

Issuer: Uruguay

Period:

(since 1825)

Currency:

(1975—1993)

Demonetization: 31 August 1995

Total mintage: 22,000,000

Material

References

KM: #Click to copy to clipboard98

Numista: #8578

Value

Exchange value: 500 UYN

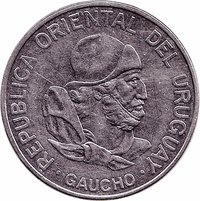

Obverse

Description:

José Artigas effigy, facing right. Country name encircling.

Inscription:

REPUBLICA ORIENTAL DEL URUGUAY

.ARTIGAS.

.ARTIGAS.

Translation:

Eastern Republic of Uruguay

.Artigas.

.Artigas.

Script: Latin

Language: Spanish

Engraver: Miguel Angel Bía

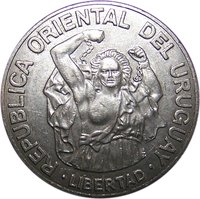

Reverse

Description:

Center value within laurel and olive wreath, tied below with a bow; date above.

Inscription:

N$

500

1989

500

1989

Script: Latin

Engraver: Miguel Angel Bía

Edge

Reeded.

Categories

| Symbol> Wreath |

| Person> Military leader |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1989 | — | 22,000,000 |

Historical background

By 1989, Uruguay was emerging from a prolonged period of economic stagnation and crisis, heavily influenced by the legacy of the 1973-1985 military dictatorship and the broader Latin American debt crisis. The dictatorship had initially stabilized the economy but left behind a burdensome foreign debt, high inflation, and a heavily regulated financial system with multiple exchange rates. Following the return to democracy in 1985, President Julio María Sanguinetti's first administration (1985-1990) faced the immense challenge of managing inflation, which had surged to over 80% annually, while also navigating the social pressures of a recovering democracy demanding higher wages and public spending.

The currency situation was characterized by a complex and unstable system. Uruguay maintained a crawling peg exchange rate regime for the peso uruguayo, where its value was adjusted frequently (devalued) in an attempt to keep pace with high domestic inflation and maintain export competitiveness. However, these devaluations were often insufficient and lagged behind inflation, leading to a significant overvaluation of the currency. This overvaluation hurt the crucial agricultural export sector and encouraged capital flight, as economic actors sought safer havens for their assets. The Central Bank struggled to defend the peg, leading to periodic losses of international reserves.

The situation culminated in a major balance of payments crisis in 1989. Investor confidence waned, and a speculative attack on the peso forced a substantial devaluation. This event starkly revealed the unsustainability of the existing exchange rate policy and underscored the deep structural problems in the Uruguayan economy. The crisis of 1989 set the stage for the more radical market-oriented reforms, including trade liberalization and a move towards greater exchange rate flexibility, that would be implemented in the early 1990s under President Luis Alberto Lacalle.

The currency situation was characterized by a complex and unstable system. Uruguay maintained a crawling peg exchange rate regime for the peso uruguayo, where its value was adjusted frequently (devalued) in an attempt to keep pace with high domestic inflation and maintain export competitiveness. However, these devaluations were often insufficient and lagged behind inflation, leading to a significant overvaluation of the currency. This overvaluation hurt the crucial agricultural export sector and encouraged capital flight, as economic actors sought safer havens for their assets. The Central Bank struggled to defend the peg, leading to periodic losses of international reserves.

The situation culminated in a major balance of payments crisis in 1989. Investor confidence waned, and a speculative attack on the peso forced a substantial devaluation. This event starkly revealed the unsustainability of the existing exchange rate policy and underscored the deep structural problems in the Uruguayan economy. The crisis of 1989 set the stage for the more radical market-oriented reforms, including trade liberalization and a move towards greater exchange rate flexibility, that would be implemented in the early 1990s under President Luis Alberto Lacalle.

Series: 1989 Uruguay circulation coins

🌱 Very Common