5 centavos – Honduras

Add to wishlist

Honduras

Context

Years: 1995–2007

Issuer: Honduras

Issuing organization: Central Bank of Honduras

Period:

(since 1862)

Currency:

(since 1931)

Total mintage: 360,000,000

Material

References

KM: #

Numista: #8490

Value

Exchange value: 0.05 HNL

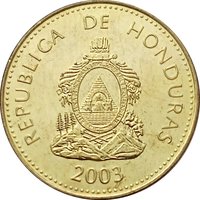

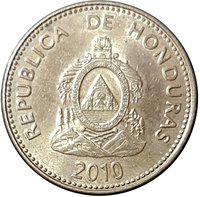

Obverse

Reverse

Edge

Plain

Categories

| Symbols> Coat of Arms |

| Symbol> Wreath |

Mints

| Name | Mark |

|---|---|

| Casa de Moneda de Chile | — |

| Royal Canadian Mint of Winnipeg | — |

| Royal Dutch Mint | — |

| Royal Mint | — |

| Vereinigte Deutsche Nickelwerke | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1995 | — | 50,000,000 | ||

| 1998 | — | 20,000,000 | ||

| 1999 | — | 50,000,000 | ||

| 2002 | — | 10,000,000 | ||

| 2003 | — | 45,000,000 | ||

| 2005 | — | 85,000,000 | ||

| 2006 | — | 20,000,000 | ||

| 2007 | — | 80,000,000 |

Historical background

In 1995, Honduras was navigating a complex monetary landscape defined by the coexistence of two official currencies: the national Honduran lempira (HNL) and the United States dollar (USD). This dual-currency system was a legacy of economic instability from the previous decade, particularly the Latin American debt crisis. While the lempira remained the primary unit for daily transactions and wages, the US dollar was widely used for major commercial contracts, real estate, banking, and international trade. This dollarization was largely informal but deeply entrenched, driven by a historical lack of confidence in the lempira as a stable store of value and a means to hedge against inflation.

The Honduran economy at the time was under a Structural Adjustment Program (SAP) supervised by the International Monetary Fund (IMF) and the World Bank. A key pillar of this program was maintaining a fixed exchange rate, which had been pegged at 7.26 lempiras to one US dollar since 1991. This policy, managed by the Central Bank of Honduras (BCH), aimed to provide stability, curb hyperinflation, and attract foreign investment. However, it also constrained monetary policy, as the BCH was compelled to use its reserves to defend the peg, limiting its ability to respond to domestic economic shocks.

Despite the fixed rate's stabilizing intent, underlying pressures persisted. The economy struggled with poverty, trade deficits, and low foreign reserves. The rigidity of the peg made Honduran exports less competitive and encouraged imports, widening the current account deficit. Furthermore, the informal dollarization created a dichotomy where the financial system's stability was increasingly tied to US monetary policy, while the broader population remained dependent on the lempira. Thus, 1995 represented a period of fragile, externally-imposed stability, setting the stage for future debates about the sustainability of the fixed exchange rate regime in the face of Honduras's structural economic challenges.

The Honduran economy at the time was under a Structural Adjustment Program (SAP) supervised by the International Monetary Fund (IMF) and the World Bank. A key pillar of this program was maintaining a fixed exchange rate, which had been pegged at 7.26 lempiras to one US dollar since 1991. This policy, managed by the Central Bank of Honduras (BCH), aimed to provide stability, curb hyperinflation, and attract foreign investment. However, it also constrained monetary policy, as the BCH was compelled to use its reserves to defend the peg, limiting its ability to respond to domestic economic shocks.

Despite the fixed rate's stabilizing intent, underlying pressures persisted. The economy struggled with poverty, trade deficits, and low foreign reserves. The rigidity of the peg made Honduran exports less competitive and encouraged imports, widening the current account deficit. Furthermore, the informal dollarization created a dichotomy where the financial system's stability was increasingly tied to US monetary policy, while the broader population remained dependent on the lempira. Thus, 1995 represented a period of fragile, externally-imposed stability, setting the stage for future debates about the sustainability of the fixed exchange rate regime in the face of Honduras's structural economic challenges.

🌱 Very Common