200 escudos – Portugal

Add to wishlist

Portugal

Context

Year: 1997

Issuer: Portugal

Period:

(since 1974)

Currency:

(1911—2001)

Demonetization: 28 February 2002

Total mintage: 1,017,000

Material

References

KM: #

Numista: #10381

Value

Exchange value: 200 PTE

Inflation-adjusted value: 361.41 PTE

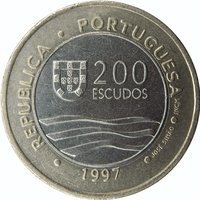

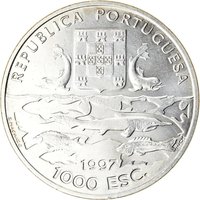

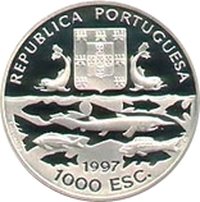

Obverse

Description:

Portuguese shield, central value.

Inscription:

· REPUBLICA · PORTUGUESA ·

200

ESCUDOS

· JOSÉ SIMÃO · INCM

1997

200

ESCUDOS

· JOSÉ SIMÃO · INCM

1997

Translation:

PORTUGUESE REPUBLIC

200

ESCUDOS

JOSÉ SIMÃO INCM

1997

200

ESCUDOS

JOSÉ SIMÃO INCM

1997

Script: Latin

Language: Portuguese

Engraver: José Simão

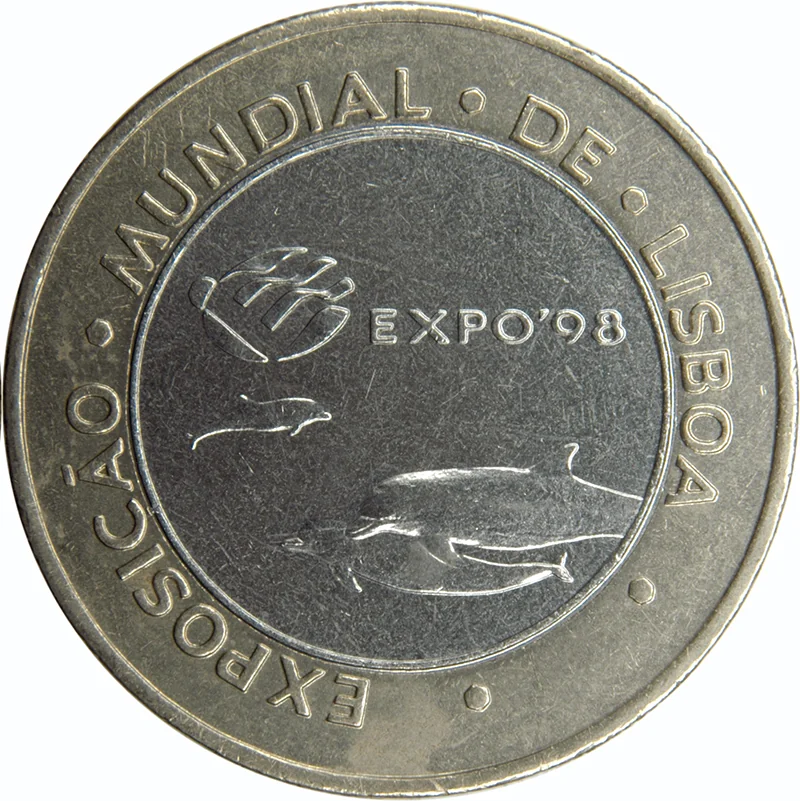

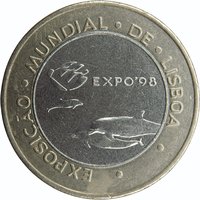

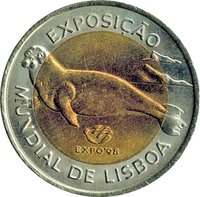

Reverse

Description:

Dolphin trio

Inscription:

· EXPOSICĀO · MUNDIAL · DE · LISBOA ·

EXPO'98

EXPO'98

Translation:

WORLD EXHIBITION OF LISBON

EXPO'98

EXPO'98

Script: Latin

Language: Portuguese

Engraver: José Simão

Edge

Alternating plain and milled sections

Categories

| Animal> Marine mammal |

| Symbols> Coat of Arms |

| Event> Fair |

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | INCM |

Mintings

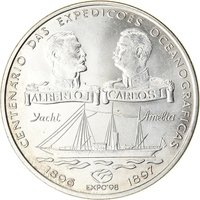

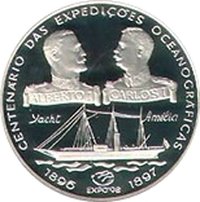

Historical background

In 1997, Portugal was in a period of significant monetary transition, firmly on the path toward European Economic and Monetary Union (EMU). The country was a committed member of the European Union's Exchange Rate Mechanism (ERM), which required it to maintain its currency, the escudo, within a narrow band of fluctuation against other European currencies, particularly the German Deutsche Mark. This discipline was crucial for meeting the strict convergence criteria—including targets for inflation, interest rates, budget deficits, and public debt—outlined in the Maastricht Treaty for adopting a single European currency.

Domestically, the government, led by Prime Minister António Guterres, pursued tight fiscal and monetary policies to ensure qualification for the first wave of the euro. Inflation and interest rates had fallen dramatically from their highs in the early 1990s, but challenges remained, particularly regarding the public debt-to-GDP ratio, which was among the highest in the EU. The escudo was stable, having been devalued within the ERM in 1992 and 1995, and by 1997 it was operating without serious tension, as markets were confident in Portugal's euro adoption prospects.

Thus, the currency situation in 1997 was one of anticipation and preparation. The escudo was effectively functioning as a proxy for the future euro, with its value pegged through the ERM. National and economic discourse was focused not on exchange rate policy but on the irreversible process of "euroization," involving public information campaigns and logistical planning for the physical introduction of euro notes and coins, which would ultimately occur on January 1, 2002, after a fixed conversion rate was set in 1999.

Domestically, the government, led by Prime Minister António Guterres, pursued tight fiscal and monetary policies to ensure qualification for the first wave of the euro. Inflation and interest rates had fallen dramatically from their highs in the early 1990s, but challenges remained, particularly regarding the public debt-to-GDP ratio, which was among the highest in the EU. The escudo was stable, having been devalued within the ERM in 1992 and 1995, and by 1997 it was operating without serious tension, as markets were confident in Portugal's euro adoption prospects.

Thus, the currency situation in 1997 was one of anticipation and preparation. The escudo was effectively functioning as a proxy for the future euro, with its value pegged through the ERM. National and economic discourse was focused not on exchange rate policy but on the irreversible process of "euroization," involving public information campaigns and logistical planning for the physical introduction of euro notes and coins, which would ultimately occur on January 1, 2002, after a fixed conversion rate was set in 1999.

Series: System 1981-2001

🌱 Very Common