20 zlotys – Poland

Add to wishlist

Non-circulating coins

Commemoration: Polish konik horse (Equus caballus gmelini)

Series: World Animals

Poland

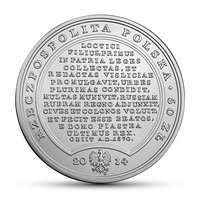

Obverse

Description:

Polish eagle with country name above, denomination below, and date beneath the eagle.

Inscription:

RZECZPOSPOLITA POLSKA

mw

2014

ZŁ 20 ZŁ

mw

2014

ZŁ 20 ZŁ

Translation:

REPUBLIC OF POLAND

mw

2014

20 ZŁOTYCH

mw

2014

20 ZŁOTYCH

Script: Latin

Language: Polish

Designer: Ewa Tyc-Karpińska

Reverse

Description:

Polish Koniks grazing

Inscription:

Equus caballus gmelini

KONIK POLSKI

tarpan

KONIK POLSKI

tarpan

Script: Latin

Designer: Tadeusz Tchórzewski

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Mint of Poland | (MW) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2014 | MW | 45,000 | Proof |

Historical background

In 2014, Poland's currency situation was characterized by a period of significant volatility for the Polish złoty (PLN), driven primarily by external geopolitical shocks. The year began with relative stability, but the escalation of the Russia-Ukraine conflict in early 2014 sent shockwaves through Central and Eastern European financial markets. As a neighboring country, Poland was perceived by investors as being exposed to regional instability, leading to capital outflows and sustained pressure on the złoty. The currency weakened notably against both the euro and the US dollar, with market sentiment overshadowing Poland's solid domestic economic fundamentals, which included steady growth and contained inflation.

The National Bank of Poland (NBP) faced a complex policy dilemma. While the weakening złoty boosted export competitiveness, it also raised the risk of imported inflation. The central bank's primary tool, the reference interest rate, was already at a historic low of 2.50% following a series of cuts in 2012-2013 to stimulate growth. Throughout 2014, the NBP held rates steady, opting for verbal interventions and occasional foreign exchange market operations to smooth excessive volatility rather than aggressively defending a specific exchange rate level. Governor Marek Belka emphasized that the bank would not "defend the złoty at all costs," signaling a focus on broader monetary stability.

By the end of 2014, the situation had partially stabilized, though the złoty remained weaker than at the start of the year. The immediate market panic subsided as the direct economic impact of the Ukraine crisis on Poland proved less severe than initially feared, and the European Central Bank's moves toward quantitative easing improved sentiment toward European assets. However, the year underscored the Polish currency's sensitivity to regional geopolitical risks and set the stage for subsequent challenges, including deflationary pressures that would lead the NBP to cut interest rates further in 2015.

The National Bank of Poland (NBP) faced a complex policy dilemma. While the weakening złoty boosted export competitiveness, it also raised the risk of imported inflation. The central bank's primary tool, the reference interest rate, was already at a historic low of 2.50% following a series of cuts in 2012-2013 to stimulate growth. Throughout 2014, the NBP held rates steady, opting for verbal interventions and occasional foreign exchange market operations to smooth excessive volatility rather than aggressively defending a specific exchange rate level. Governor Marek Belka emphasized that the bank would not "defend the złoty at all costs," signaling a focus on broader monetary stability.

By the end of 2014, the situation had partially stabilized, though the złoty remained weaker than at the start of the year. The immediate market panic subsided as the direct economic impact of the Ukraine crisis on Poland proved less severe than initially feared, and the European Central Bank's moves toward quantitative easing improved sentiment toward European assets. However, the year underscored the Polish currency's sensitivity to regional geopolitical risks and set the stage for subsequent challenges, including deflationary pressures that would lead the NBP to cut interest rates further in 2015.

Series: World Animals

💎 Extremely Rare