1 ducat – Yugoslavia

Add to wishlist

Context

Years: 1931–1934

Issuer: Yugoslavia

Ruler: Alexander I

Currency:

(1918—1941)

Demonetized: Yes

Total mintage: 92,000

Material

References

KM: #

Numista: #80614

Value

Bullion value: $526.05

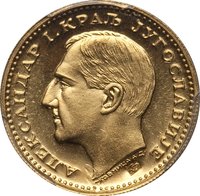

Obverse

Description:

King Alexander I, left profile.

Inscription:

АЛЕКСАНДАР I КРАЉ ЈУГОСЛАВИЈЕ

KOBНИЦA A.Д.

KOBНИЦA A.Д.

Translation:

ALEXANDER I KING OF YUGOSLAVIA

THE MINT A.D.

THE MINT A.D.

Script: Cyrillic

Language: Serbian

Engravers: Richard Placht, Joseph Prinz

Reverse

Description:

Crowned double eagle bearing a shield.

Inscription:

KRALJEVINA JUGOSLAVIJА 1931

DUKAT 1 ДУКАТ

DUKAT 1 ДУКАТ

Translation:

KINGDOM OF YUGOSLAVIA 1931

DUCAT 1 DUCAT

DUCAT 1 DUCAT

Languages: Church Slavic, Serbian

Engravers: Richard Placht, Joseph Prinz

Edge

Reeded

Categories

| Animal> Bird |

| Person> Monarch |

| Symbol> Crown |

| Symbols> Coat of Arms |

| Symbol> Double-headed eagle |

Mints

| Name | Mark |

|---|---|

| Belgrade | — |

| Münze Österreich | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1931 | k | 50,000 | ||

| 1932 | k | — | ||

| 1933 | k | 40,000 | ||

| 1934 | k | 2,000 |

Historical background

In 1931, the Kingdom of Yugoslavia was grappling with the severe global repercussions of the Great Depression, which exposed the fundamental weaknesses of its agrarian economy and its dependence on foreign capital. The national currency, the Yugoslav dinar, was under significant pressure as the crisis caused a collapse in the prices of its key agricultural exports (like grains and livestock), leading to a dramatic fall in foreign exchange earnings. This balance of payments crisis depleted the gold and foreign currency reserves of the National Bank, threatening the dinar's stability and the state's ability to service its substantial external debts, much of which was owed to French and American creditors.

The government's initial response was deflationary austerity, but by 1931, more drastic measures were required. In April, the state imposed strict foreign exchange controls, monopolizing all foreign currency transactions to prevent capital flight and conserve scarce reserves. This was followed by the "London Agreement" in July, a forced rescheduling of Yugoslavia's foreign debt, which provided temporary relief but came with stringent conditions for economic oversight by foreign creditors. These actions effectively took the country off the gold standard and moved it toward a managed, inconvertible currency, marking a decisive shift from a liberal economic model to a state-directed system.

Consequently, the dinar's international convertibility was suspended, and its value was no longer solely dictated by market forces but by administrative decree. The economy became increasingly insular, with trade relying more on bilateral clearing agreements with other Central European states. While these emergency measures staved off immediate financial collapse, they entrenched economic statism, reduced market efficiency, and contributed to a prolonged period of low domestic investment and industrial stagnation throughout the 1930s, setting a precedent for greater state intervention in the economy.

The government's initial response was deflationary austerity, but by 1931, more drastic measures were required. In April, the state imposed strict foreign exchange controls, monopolizing all foreign currency transactions to prevent capital flight and conserve scarce reserves. This was followed by the "London Agreement" in July, a forced rescheduling of Yugoslavia's foreign debt, which provided temporary relief but came with stringent conditions for economic oversight by foreign creditors. These actions effectively took the country off the gold standard and moved it toward a managed, inconvertible currency, marking a decisive shift from a liberal economic model to a state-directed system.

Consequently, the dinar's international convertibility was suspended, and its value was no longer solely dictated by market forces but by administrative decree. The economy became increasingly insular, with trade relying more on bilateral clearing agreements with other Central European states. While these emergency measures staved off immediate financial collapse, they entrenched economic statism, reduced market efficiency, and contributed to a prolonged period of low domestic investment and industrial stagnation throughout the 1930s, setting a precedent for greater state intervention in the economy.

⭐ Rare