5 Sovereigns – United Kingdom

United Kingdom

Context

Material

References

KM: #Click to copy to clipboard1368

Numista: #79906

Value

Exchange value: 5 GBP = $6.77

Bullion value: $6104.50

Inflation-adjusted value: 7.08 GBP

Obverse

Description:

Butler effigy of Elizabeth II, limited release.

Inscription:

ELIZABETH II·DEI·GRA·REGINA·FID·DEF

JB

JB

Translation:

Elizabeth II by the Grace of God Queen Defender of the Faith

Script: Latin

Language: Latin

Engraver: James Butler

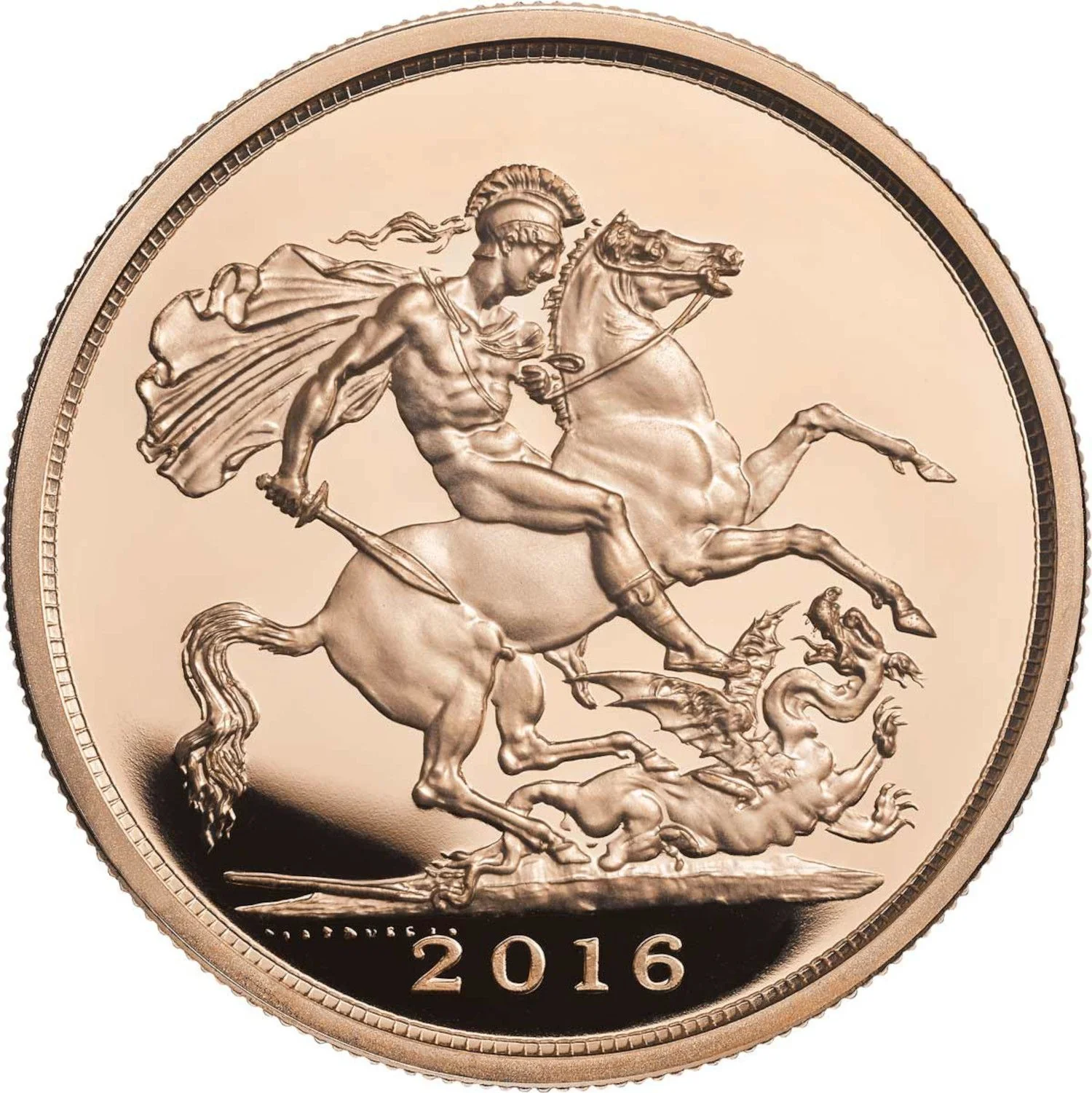

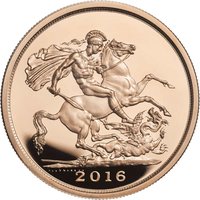

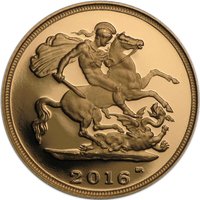

Reverse

Description:

St. George slaying the dragon; designer's name and date below.

Inscription:

PISTRUCCI.

2016

2016

Script: Latin

Designer: Benedetto Pistrucci

Edge

Milled

Categories

| Mythology> Fantastic animal |

| Animal> Horse |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2016 | — | 573 | Proof |

Historical background

The United Kingdom's currency situation in 2016 was dominated by the political and economic shockwaves of the EU referendum on 23 June. In the months leading up to the vote, the pound sterling was relatively stable, trading around $1.45 against the US dollar, as markets anticipated a narrow victory for the "Remain" campaign. However, the unexpected result in favour of "Leave" triggered an immediate and severe market reaction. On 24 June, the pound experienced its largest one-day fall in history against the dollar since the era of free-floating exchange rates began, plummeting over 8% to a 31-year low below $1.33. This dramatic devaluation reflected acute investor anxiety over the UK's future trading relationships, access to the single market, and overall economic prospects outside the European Union.

Following the initial crash, sterling remained under intense pressure throughout the second half of the year, becoming highly sensitive to political developments and statements regarding the government's approach to the impending Brexit negotiations. In October, a "flash crash" saw the pound briefly tumble a further 6% against the dollar in Asian trading, highlighting its new-found volatility. By year-end, sterling had settled around 16% lower against the dollar and 12% lower against the euro compared to its pre-referendum levels. This sustained weakness had a dual impact: it increased the cost of imports, contributing to a rise in inflation that would materialise in 2017, but it also provided a temporary boost to the competitiveness of UK exports and the attractiveness of UK assets for foreign investors.

The Bank of England responded to the post-referendum uncertainty by implementing a significant monetary policy package in August. This included cutting the Bank Rate to a new historic low of 0.25%, expanding quantitative easing, and introducing a Term Funding Scheme to ensure the rate cut passed through to the real economy. Governor Mark Carney emphasised that the measures were intended to support confidence and cushion the expected economic slowdown, not as a direct response to the currency's fall. Thus, 2016 concluded with the pound in a fundamentally weaker position, establishing a new, lower trading range that reflected the market's repricing of the UK's long-term economic outlook in the face of an unprecedented and complex Brexit process.

Following the initial crash, sterling remained under intense pressure throughout the second half of the year, becoming highly sensitive to political developments and statements regarding the government's approach to the impending Brexit negotiations. In October, a "flash crash" saw the pound briefly tumble a further 6% against the dollar in Asian trading, highlighting its new-found volatility. By year-end, sterling had settled around 16% lower against the dollar and 12% lower against the euro compared to its pre-referendum levels. This sustained weakness had a dual impact: it increased the cost of imports, contributing to a rise in inflation that would materialise in 2017, but it also provided a temporary boost to the competitiveness of UK exports and the attractiveness of UK assets for foreign investors.

The Bank of England responded to the post-referendum uncertainty by implementing a significant monetary policy package in August. This included cutting the Bank Rate to a new historic low of 0.25%, expanding quantitative easing, and introducing a Term Funding Scheme to ensure the rate cut passed through to the real economy. Governor Mark Carney emphasised that the measures were intended to support confidence and cushion the expected economic slowdown, not as a direct response to the currency's fall. Thus, 2016 concluded with the pound in a fundamentally weaker position, establishing a new, lower trading range that reflected the market's repricing of the UK's long-term economic outlook in the face of an unprecedented and complex Brexit process.

Series: Sovereign series

✨ Legendary