10 Gulden (Liberation) – Netherlands

Circulating commemorative coins

Commemoration: 25th Anniversary of Liberation

Netherlands

Context

Year: 1970

Issuer: Netherlands

Ruler: Juliana

Currency:

(1817—2001)

Demonetized: Yes

Total mintage: 6,000,040

Material

References

KM: #Click to copy to clipboard195

Numista: #7946

Value

Exchange value: 10 NLG

Bullion value: $51.11

Inflation-adjusted value: 58.31 NLG

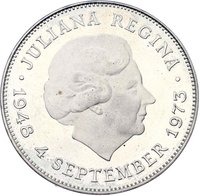

Obverse

Description:

Queen Juliana facing right

Inscription:

JULIANA KONINGIN DER NEDERLANDEN •

W

W

Translation:

Juliana Queen of the Netherlands •

Script: Latin

Language: Dutch

Engraver: Ludwig Oswald Wenckebach

Reverse

Edge

Mints

| Name | Mark |

|---|---|

| Royal Dutch Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1970 | — | 5,980,000 | ||

| 1970 | — | 40 | Proof | |

| 1970 | — | 20,000 | Prooflike |

Historical background

In the early 1970s, the Netherlands operated within the Bretton Woods system of fixed exchange rates, pegging the Dutch guilder to the US dollar. This period was one of significant international monetary turbulence. The system came under severe strain as the United States, facing inflation and trade deficits, suspended the dollar's convertibility into gold in August 1971 (the "Nixon Shock"). This event effectively ended the Bretton Woods system and forced a realignment of global currencies, leading to the Smithsonian Agreement later that year, which established new fixed parities.

Domestically, the guilder was considered a strong and stable "hard currency," a reputation the Dutch central bank (De Nederlandsche Bank) guarded fiercely through conservative monetary policy. However, the collapse of the fixed-rate regime presented a challenge. To maintain regional stability, the Netherlands chose to closely shadow the West German Deutsche Mark, its most important trading partner. This policy decision was a pragmatic move, acknowledging Germany's economic dominance in Europe and the desire to shield Dutch trade from excessive currency fluctuation, effectively placing the guilder within the emerging "German Mark zone."

By 1972, the Netherlands joined the European "snake in the tunnel" arrangement, an early attempt at European monetary cooperation that aimed to limit fluctuations between member currencies. The guilder's participation was characterized by its close alignment with the Deutsche Mark, a relationship that would define Dutch monetary policy for decades. This era set the crucial precedent for the Netherlands' full commitment to later European Exchange Rate Mechanism (ERM) and, ultimately, its adoption of the euro, framing the 1970s as a pivotal transition from dollar-linked stability to a future anchored within a European monetary framework.

Domestically, the guilder was considered a strong and stable "hard currency," a reputation the Dutch central bank (De Nederlandsche Bank) guarded fiercely through conservative monetary policy. However, the collapse of the fixed-rate regime presented a challenge. To maintain regional stability, the Netherlands chose to closely shadow the West German Deutsche Mark, its most important trading partner. This policy decision was a pragmatic move, acknowledging Germany's economic dominance in Europe and the desire to shield Dutch trade from excessive currency fluctuation, effectively placing the guilder within the emerging "German Mark zone."

By 1972, the Netherlands joined the European "snake in the tunnel" arrangement, an early attempt at European monetary cooperation that aimed to limit fluctuations between member currencies. The guilder's participation was characterized by its close alignment with the Deutsche Mark, a relationship that would define Dutch monetary policy for decades. This era set the crucial precedent for the Netherlands' full commitment to later European Exchange Rate Mechanism (ERM) and, ultimately, its adoption of the euro, framing the 1970s as a pivotal transition from dollar-linked stability to a future anchored within a European monetary framework.

🌱 Common