25 Kuruş – Turkey

Turkey

Context

Material

Diameter: 19.5 mm

Weight: 3 g

Thickness: 1.4 mm

Shape: Round

Composition: Nickel brass

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard880

Numista: #7854

Value

Exchange value: 0.25 TRL

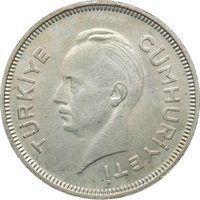

Obverse

Reverse

Edge

Inscripted

Legend:

* T.C. *

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1944 | — | 20,000,000 | ||

| 1945 | — | 5,328,000 | ||

| 1946 | — | 2,672,000 |

Historical background

In 1944, Turkey's currency situation was defined by a tightly controlled and stable lira, a stark contrast to the inflationary pressures that would emerge in later decades. This stability was a deliberate outcome of the nation's unique position during World War II. While maintaining a policy of armed neutrality, Turkey pursued a state-directed economic model known as étatism. The government, through the Central Bank of the Republic of Turkey (established in 1930), maintained strict control over foreign exchange, gold reserves, and the money supply, effectively insulating the Turkish lira from the global turmoil.

This control was exercised via a complex system of multiple exchange rates. Different rates were applied to various sectors (like essential imports versus luxury goods) and types of transactions, a mechanism designed to conserve scarce foreign currency, manage the balance of payments, and steer economic activity according to state priorities. The primary goal was not free-market equilibrium but ensuring the financing of critical imports and maintaining monetary stability, which was largely successful during this period.

Consequently, the official exchange rate in 1944 was pegged at a fixed and highly overvalued level of 1.28 Turkish lira to 1 US dollar, a rate set in 1941 and maintained until 1946. This artificial peg, combined with strict capital controls, masked underlying economic pressures. While it provided short-term stability, it created distortions, encouraged a black market for foreign currency, and stored up problems. The post-war period would soon force a reckoning, leading to a major devaluation in 1946 as Turkey moved to align its currency with market realities and integrate into the new Bretton Woods international financial system.

This control was exercised via a complex system of multiple exchange rates. Different rates were applied to various sectors (like essential imports versus luxury goods) and types of transactions, a mechanism designed to conserve scarce foreign currency, manage the balance of payments, and steer economic activity according to state priorities. The primary goal was not free-market equilibrium but ensuring the financing of critical imports and maintaining monetary stability, which was largely successful during this period.

Consequently, the official exchange rate in 1944 was pegged at a fixed and highly overvalued level of 1.28 Turkish lira to 1 US dollar, a rate set in 1941 and maintained until 1946. This artificial peg, combined with strict capital controls, masked underlying economic pressures. While it provided short-term stability, it created distortions, encouraged a black market for foreign currency, and stored up problems. The post-war period would soon force a reckoning, leading to a major devaluation in 1946 as Turkey moved to align its currency with market realities and integrate into the new Bretton Woods international financial system.

🌱 Common