10 Kuruş – Turkey

Circulating commemorative coins

Commemoration: FAO - Agricultural Progress Series

Turkey

Context

Material

References

KM: #Click to copy to clipboard898

Numista: #1134

Value

Exchange value: 0.10 TRL

Inflation-adjusted value: 1500612.04 TRL

Obverse

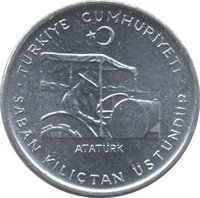

Description:

Atatürk driving a tractor right. KM#898.1: thicker, 3.5 g. KM#898.2: thinner, 2.5 g.

Inscription:

ATATÜRK

Translation:

Father of the Turks

Script: Latin

Language: Turkish

Engraver: İ. Avni Kumuk

Reverse

Edge

Plain

Categories

| Person> Military leader |

| Person> Politician |

| Organization> FAO |

| Transportation> Truck or tractor |

Mints

| Name | Mark |

|---|---|

| Turkish State Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1971 | — | 630,000 | ||

| 1972 | — | 500,000 | ||

| 1973 | — | 10,000 | ||

| 1974 | — | 605,000 |

Historical background

Turkey's currency situation in 1971 was a critical juncture in its post-war economic history, characterized by a severe balance of payments crisis and the culmination of an unsustainable, state-led industrialization model. The decade prior had seen rapid growth under import-substitution policies, but this was financed by heavy external borrowing and chronic trade deficits. By 1970, foreign exchange reserves were nearly depleted, inflation was rising, and the fixed exchange rate of 9 Turkish lira to 1 US dollar, maintained since 1960, had become wildly overvalued, crippling exports and encouraging a black market for foreign currency.

The crisis came to a head in 1971, forcing the government to implement a major devaluation and seek stabilization. On August 9, 1971, Turkey was compelled to devalue the lira by 66%, setting a new rate of 14 lira to the dollar. This drastic measure was a condition for securing a crucial stabilization loan from the International Monetary Fund (IMF) and the Organisation for Economic Co-operation and Development (OECD), which Turkey urgently needed to service its foreign debt and finance essential imports. The devaluation was part of a broader austerity package aimed at reducing domestic demand and liberalizing the tightly controlled economy.

The 1971 devaluation marked a symbolic end to the era of fixed parity and exposed the fragility of Turkey's inward-looking economic strategy. While the immediate liquidity crisis was alleviated, the structural problems remained largely unaddressed, setting the stage for the even more severe oil shock-induced crises of the late 1970s. Consequently, 1971 is remembered not as a resolution, but as a painful prelude to a decade of escalating inflation, political instability, and a definitive shift toward outward-oriented policies that would only fully materialize in the 1980s.

The crisis came to a head in 1971, forcing the government to implement a major devaluation and seek stabilization. On August 9, 1971, Turkey was compelled to devalue the lira by 66%, setting a new rate of 14 lira to the dollar. This drastic measure was a condition for securing a crucial stabilization loan from the International Monetary Fund (IMF) and the Organisation for Economic Co-operation and Development (OECD), which Turkey urgently needed to service its foreign debt and finance essential imports. The devaluation was part of a broader austerity package aimed at reducing domestic demand and liberalizing the tightly controlled economy.

The 1971 devaluation marked a symbolic end to the era of fixed parity and exposed the fragility of Turkey's inward-looking economic strategy. While the immediate liquidity crisis was alleviated, the structural problems remained largely unaddressed, setting the stage for the even more severe oil shock-induced crises of the late 1970s. Consequently, 1971 is remembered not as a resolution, but as a painful prelude to a decade of escalating inflation, political instability, and a definitive shift toward outward-oriented policies that would only fully materialize in the 1980s.

🌱 Very Common