10 Kuruş – Turkey

Circulating commemorative coins

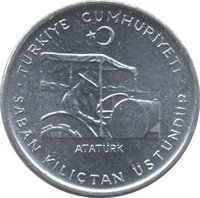

Commemoration: FAO - Agricultural Progress Series

Turkey

Context

Material

References

KM: #Click to copy to clipboard898a

Numista: #9615

Value

Exchange value: 0.10 TRL

Inflation-adjusted value: 773849.27 TRL

Obverse

Reverse

Edge

Plain

Categories

| Transportation> Truck or tractor |

| Organization> FAO |

Mints

| Name | Mark |

|---|---|

| Turkish State Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1975 | — | 517,000 |

Historical background

Turkey's currency situation in 1975 was defined by a precarious stability, marking the final phase of a fixed exchange rate regime that was becoming increasingly unsustainable. The Turkish Lira (TL) had been pegged to the US Dollar at a rate of TL 14 = $1 since the 1970 devaluation, a policy maintained by the government of Prime Minister Süleyman Demirel. This peg was artificially defended through strict capital controls and heavy reliance on foreign borrowing, particularly from the International Monetary Fund (IMF) and remittances from Turkish workers in Europe. While this provided a veneer of stability for several years, it masked deep structural problems, including high inflation, a growing trade deficit, and significant state-led industrialization efforts that strained public finances.

Beneath the surface, the economy was under severe pressure. The global oil crisis of 1973 had dramatically increased Turkey's import bill, while exports failed to keep pace, leading to a chronic balance of payments deficit. Domestically, inflation was accelerating into double digits, eroding the lira's real value and creating a powerful black market for foreign currency where the dollar traded at a significant premium. The fixed parity became divorced from economic reality, making Turkish exports increasingly uncompetitive and encouraging capital flight. The government's response was to borrow heavily abroad to finance the deficits and maintain the peg, setting the stage for a future debt crisis.

Thus, 1975 represented the calm before the storm. The rigid exchange rate was a key pillar of government policy, but it was maintained only through unsustainable short-term measures. The mounting external debt, rampant inflation, and political fragmentation of the late 1970s would soon make the fixed parity untenable. The inevitable collapse came just a few years later, leading to a major devaluation in 1979 and the full adoption of a floating exchange rate regime in the early 1980s as part of a sweeping economic stabilization program.

Beneath the surface, the economy was under severe pressure. The global oil crisis of 1973 had dramatically increased Turkey's import bill, while exports failed to keep pace, leading to a chronic balance of payments deficit. Domestically, inflation was accelerating into double digits, eroding the lira's real value and creating a powerful black market for foreign currency where the dollar traded at a significant premium. The fixed parity became divorced from economic reality, making Turkish exports increasingly uncompetitive and encouraging capital flight. The government's response was to borrow heavily abroad to finance the deficits and maintain the peg, setting the stage for a future debt crisis.

Thus, 1975 represented the calm before the storm. The rigid exchange rate was a key pillar of government policy, but it was maintained only through unsustainable short-term measures. The mounting external debt, rampant inflation, and political fragmentation of the late 1970s would soon make the fixed parity untenable. The inevitable collapse came just a few years later, leading to a major devaluation in 1979 and the full adoption of a floating exchange rate regime in the early 1980s as part of a sweeping economic stabilization program.

🌱 Common