500 guaraníes – Paraguay

Add to wishlist

Paraguay

Context

Years: 2006–2019

Issuer: Paraguay

Issuing organization: Central Bank of Paraguay

Period:

(since 1811)

Currency:

(since 1944)

Total mintage: 92,000,000

Material

Diameter: 23 mm

Weight: 4.8 g

Thickness: 1.7 mm

Shape: Round

Composition: Nickel-steel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #7615

Value

Exchange value: 500 PYG

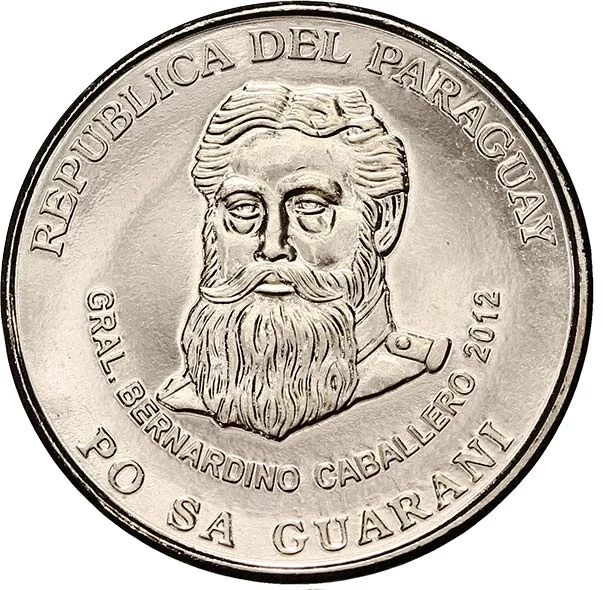

Obverse

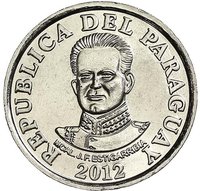

Reverse

Edge

Plain

Categories

| Person> Politician |

| Building |

| Person> Military leader |

Mints

| Name | Mark |

|---|---|

| Casa de Moneda de Chile | — |

| Kremnica | — |

| Mint of Poland | — |

| Royal Canadian Mint of Winnipeg | — |

| South African Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2006 | — | 12,000,000 | ||

| 2007 | — | 25,000,000 | ||

| 2008 | — | 15,000,000 | ||

| 2011 | — | 20,000,000 | ||

| 2012 | — | 20,000,000 | ||

| 2014 | — | — | ||

| 2016 | — | — | ||

| 2019 | — | — |

Historical background

In 2006, Paraguay's currency situation was characterized by a prolonged period of relative stability for the Guaraní (PYG) within a managed floating exchange rate regime. The Central Bank of Paraguay (BCP) intervened in the foreign exchange market primarily to smooth out excessive volatility rather than to defend a fixed parity. This period followed the significant turbulence of the late 1990s and early 2000s, which included a banking crisis and a sharp devaluation. By 2006, the economy was experiencing moderate growth, supported by strong agricultural exports, particularly soybeans, which generated a steady inflow of US dollars. This commodity-driven dollar inflow helped support the guaraní's value and provided the central bank with growing international reserves.

However, this stability was not without underlying pressures. A persistent challenge was, and remains, the high degree of dollarization within the financial system. While the guaraní was used for everyday transactions, a significant portion of bank loans (over 50%) and deposits were denominated in US dollars, exposing borrowers and the financial sector to exchange rate risk. Furthermore, the economy was highly sensitive to external shocks, such as fluctuations in commodity prices and the economic conditions of neighboring giants Brazil and Argentina. Inflation, though moderating from earlier highs, remained a concern, ending 2006 at around 9.3%, which influenced the BCP's monetary policy decisions regarding interest rates and liquidity management.

Overall, the 2006 currency landscape reflected a fragile equilibrium. The guaraní benefited from favorable terms of trade and increased reserve buffers, allowing the BCP to maintain a stable nominal exchange rate. Yet, this stability was contingent on continued strong export performance and prudent fiscal policy. The deep-seated structural issue of dollarization limited the effectiveness of monetary policy and meant that long-term currency stability was closely tied to building deeper confidence in the guaraní and developing the local currency financial market, challenges that would extend well beyond 2006.

However, this stability was not without underlying pressures. A persistent challenge was, and remains, the high degree of dollarization within the financial system. While the guaraní was used for everyday transactions, a significant portion of bank loans (over 50%) and deposits were denominated in US dollars, exposing borrowers and the financial sector to exchange rate risk. Furthermore, the economy was highly sensitive to external shocks, such as fluctuations in commodity prices and the economic conditions of neighboring giants Brazil and Argentina. Inflation, though moderating from earlier highs, remained a concern, ending 2006 at around 9.3%, which influenced the BCP's monetary policy decisions regarding interest rates and liquidity management.

Overall, the 2006 currency landscape reflected a fragile equilibrium. The guaraní benefited from favorable terms of trade and increased reserve buffers, allowing the BCP to maintain a stable nominal exchange rate. Yet, this stability was contingent on continued strong export performance and prudent fiscal policy. The deep-seated structural issue of dollarization limited the effectiveness of monetary policy and meant that long-term currency stability was closely tied to building deeper confidence in the guaraní and developing the local currency financial market, challenges that would extend well beyond 2006.

Series: 2006 Paraguay circulation coins

🌱 Very Common