10 pesos uruguayos – Uruguay

Add to wishlist

Circulating commemorative coins

Commemoration: Bicentenario del Reglamento de Tierras de 1815

Uruguay

Context

Material

References

KM: #

Numista: #75972

Value

Exchange value: 10 UYU

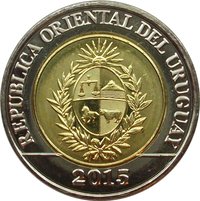

Obverse

Reverse

Description:

Head of a mixed-heritage Gaucho. Below, a quote from Artigas expresses the ideal of equitable rule. Value at bottom.

Inscription:

BICENTENARIO DEL REGLAMENTO DE TIERRAS DE 1815

"Los más infelices serán

los más privilegiados"

$ 10

"Los más infelices serán

los más privilegiados"

$ 10

Translation:

Bicentennial of the Land Regulation of 1815

"The most unfortunate shall be

the most privileged"

$ 10

"The most unfortunate shall be

the most privileged"

$ 10

Script: Latin

Language: Spanish

Edge

Plain

Categories

| Object> Hat |

| Mustache/Beard |

| Symbols> Coat of Arms |

| Symbol> Sun |

| Symbol> Wreath |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2015 | — | 10,000,000 |

Historical background

In 2015, Uruguay's currency situation was characterized by a significant and sustained appreciation of the Uruguayan peso against the US dollar, a trend that had been ongoing since 2003. The peso strengthened from approximately 30 pesos per dollar in the early 2000s to around 24 pesos per dollar by mid-2015. This appreciation was driven by strong capital inflows, high prices for the country's key commodity exports (notably soybeans and beef), and a period of robust economic growth that boosted investor confidence. However, this strength created notable headwinds for the export-oriented sectors of the economy, as Uruguayan goods became more expensive on the international market.

The government of President Tabaré Vázquez, who took office in March 2015, faced the dual challenge of managing this currency pressure while confronting rising inflation, which hovered near the upper limit of the central bank's target range at around 8-9%. The Central Bank of Uruguay (BCU) intervened in the foreign exchange market throughout the year, purchasing US dollars to build international reserves and temper the peso's rise. These interventions aimed to alleviate the competitiveness strain on exporters and the tourism sector without fully reversing the appreciation trend, which also helped curb imported inflation.

By the end of 2015, the currency dynamics began to shift as external conditions changed. A slowdown in major economies like Brazil and China, coupled with a strengthening US dollar and falling global commodity prices, started to reverse the peso's long rally. This shift set the stage for a period of gradual depreciation in the following years, moving the policy focus from curbing appreciation to managing volatility and containing the inflationary effects of a weaker peso.

The government of President Tabaré Vázquez, who took office in March 2015, faced the dual challenge of managing this currency pressure while confronting rising inflation, which hovered near the upper limit of the central bank's target range at around 8-9%. The Central Bank of Uruguay (BCU) intervened in the foreign exchange market throughout the year, purchasing US dollars to build international reserves and temper the peso's rise. These interventions aimed to alleviate the competitiveness strain on exporters and the tourism sector without fully reversing the appreciation trend, which also helped curb imported inflation.

By the end of 2015, the currency dynamics began to shift as external conditions changed. A slowdown in major economies like Brazil and China, coupled with a strengthening US dollar and falling global commodity prices, started to reverse the peso's long rally. This shift set the stage for a period of gradual depreciation in the following years, moving the policy focus from curbing appreciation to managing volatility and containing the inflationary effects of a weaker peso.

🌱 Common