Obverse

Description:

Spanish coat of arms elements: castle (Castile), lion (León), four pallets (Aragon), chains (Navarre), pomegranate (Granada), with external yoke and arrows.

Inscription:

1 PESETA

Script: Latin

Engraver: Carlos Mingo López

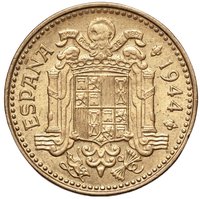

Reverse

Description:

Spanish coat of arms featuring a yoke and arrows.

Inscription:

ESPAÑA ✤ 1944 ✤

UNA GRANDE LIBRE

PLUS ULTRA

UNA GRANDE LIBRE

PLUS ULTRA

Translation:

One Great Free

Further Beyond

Further Beyond

Script: Latin

Language: Spanish

Engraver: Carlos Mingo López

Edge

Reeded

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint of Madrid | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1944 | — | 150,000,000 |

Historical background

In 1944, Spain's currency situation was a direct reflection of the country's profound economic isolation and the legacy of the devastating Spanish Civil War (1936-1939). The official currency, the peseta, was severely weakened and controlled by the autarkic economic policies of General Francisco Franco's regime. The government maintained an artificially strong official exchange rate, but this bore little relation to reality. A vast and essential black market for foreign currency, particularly the US dollar and British pound, operated openly, with exchange rates there being several times higher than the official rate. This duality crippled legitimate foreign trade and investment, as the regime lacked the gold and hard currency reserves to support its financial position on the world stage.

Domestically, the economy was characterized by scarcity, rationing, and inflation, though the latter was partially suppressed by price controls. The money supply had expanded significantly during and after the Civil War to finance the Nationalist side and post-war reconstruction, leading to persistent monetary overhang. Industrial and agricultural production remained below pre-1936 levels, causing a shortage of goods that further undermined the peseta's real value. The regime's policy of economic self-sufficiency (autarky) prevented meaningful recovery, as Spain was largely cut off from the Marshall Plan and other post-war European recovery initiatives due to Franco's political alignment with the defeated Axis powers.

Internationally, Spain was a financial pariah. Excluded from the Bretton Woods system established that same year and from the nascent International Monetary Fund, the peseta was a non-convertible currency with no standing in international finance. This isolation forced bilateral barter agreements for essential imports. The situation began a very slow shift only later in 1944, as Allied victory became certain, prompting Franco to make tentative gestures toward economic liberalization to ensure the regime's survival, though the fundamental currency weaknesses would persist for years.

Domestically, the economy was characterized by scarcity, rationing, and inflation, though the latter was partially suppressed by price controls. The money supply had expanded significantly during and after the Civil War to finance the Nationalist side and post-war reconstruction, leading to persistent monetary overhang. Industrial and agricultural production remained below pre-1936 levels, causing a shortage of goods that further undermined the peseta's real value. The regime's policy of economic self-sufficiency (autarky) prevented meaningful recovery, as Spain was largely cut off from the Marshall Plan and other post-war European recovery initiatives due to Franco's political alignment with the defeated Axis powers.

Internationally, Spain was a financial pariah. Excluded from the Bretton Woods system established that same year and from the nascent International Monetary Fund, the peseta was a non-convertible currency with no standing in international finance. This isolation forced bilateral barter agreements for essential imports. The situation began a very slow shift only later in 1944, as Allied victory became certain, prompting Franco to make tentative gestures toward economic liberalization to ensure the regime's survival, though the fundamental currency weaknesses would persist for years.

🌱 Very Common