10 rubles – Russian Federation

Add to wishlist

Circulating commemorative coins

Commemoration: Historical cities of Russia series: Azov

Series: Ancient Towns of Russia

Russia

Context

Year: 2008

Country: Russia

Issuer: Russian Federation

Period:

(since 1991)

Currency:

(since 1998)

Total mintage: 5,000,000

Material

Diameter: 27 mm

Weight: 8.4 g

Thickness: 2.1 mm

Shape: Round

Techniques: Latent image, Milled

Alignment: Medal alignment

flip

References

Value

Exchange value: 10 RUB

Inflation-adjusted value: 43.27 RUB

Obverse

Description:

At the disc's center is the face value "10 РУБЛЕЙ". Inside the "0", hidden images of "10" and "РУБ" appear as the angle changes. The mint mark is below. The ring reads "БАНК РОССИИ" above and "2008 г." below, with stylized plant branches extending onto the disc from the sides.

Inscription:

БАНК РОССИИ

10

РУБЛЕЙ

ММД

2008

10

РУБЛЕЙ

ММД

2008

Translation:

BANK OF RUSSIA

10

RUBLES

MMD

2008

10

RUBLES

MMD

2008

Script: Cyrillic

Language: Russian

Designer and engraver: Alexander Vasilyevich Baklanov

Reverse

Description:

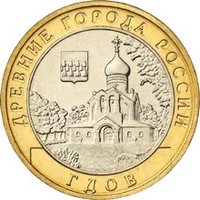

The disc features a panorama of the town under the Azov coat of arms, encircled by the inscriptions "ДРЕВНИЕ ГОРОДА РОССИИ" above and "АЗОВ" below.

Inscription:

ДРЕВНИЕ ГОРОДА РОССИИ

АЗОВ

АЗОВ

Translation:

Ancient Cities of Russia

Azov

Azov

Script: Cyrillic

Language: Russian

Engraver: Elena Ivanovna Novikova

Designer: Anton Dmitrievich Schablykin

Edge

Categories

| Building> Religious building |

| Geography> Town |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Moscow Mint | (ММД) |

| Saint Petersburg | (СПМД) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2008 | ММД | 2,500,000 | ||

| 2008 | СПМД | 2,500,000 | BU |

Historical background

The Russian Federation entered 2008 with a currency situation characterized by significant strength and stability, largely driven by a prolonged boom in global oil and gas prices. The Russian ruble was effectively managed within a crawling peg against a dual-currency basket (55% USD, 45% EUR), allowing for gradual, controlled appreciation. This policy, combined with massive capital inflows, led to a substantial accumulation of foreign exchange reserves, which peaked at nearly $600 billion in mid-2008—the third-largest in the world at the time. This robust position created an atmosphere of confidence, with authorities focused on fighting inflation and reducing the dollarization of the economy.

However, the global financial crisis dramatically reversed this situation in the latter half of the year. As oil prices collapsed from historic highs of over $140 per barrel to around $40 by year's end, and global credit markets froze, Russia faced a perfect storm. Investor confidence evaporated, leading to massive capital flight estimated at $130 billion in the last quarter alone. Intense pressure on the ruble forced the Central Bank of Russia (CBR) to intervene heavily, spending over $200 billion of its reserves in a costly defense of the currency's trading band to prevent a disorderly devaluation and a banking crisis.

By December 2008, the unsustainable drain on reserves compelled the CBR to enact a controlled, stepwise devaluation of the ruble. It gradually widened the trading band for the dual-currency basket 19 times, allowing the ruble to depreciate by approximately 30% against the USD since its summer peak. This move marked a stark end to the era of a strong, managed ruble, transitioning the economy into a period of crisis management, recession, and a new reality of a significantly weaker national currency as 2009 began.

However, the global financial crisis dramatically reversed this situation in the latter half of the year. As oil prices collapsed from historic highs of over $140 per barrel to around $40 by year's end, and global credit markets froze, Russia faced a perfect storm. Investor confidence evaporated, leading to massive capital flight estimated at $130 billion in the last quarter alone. Intense pressure on the ruble forced the Central Bank of Russia (CBR) to intervene heavily, spending over $200 billion of its reserves in a costly defense of the currency's trading band to prevent a disorderly devaluation and a banking crisis.

By December 2008, the unsustainable drain on reserves compelled the CBR to enact a controlled, stepwise devaluation of the ruble. It gradually widened the trading band for the dual-currency basket 19 times, allowing the ruble to depreciate by approximately 30% against the USD since its summer peak. This move marked a stark end to the era of a strong, managed ruble, transitioning the economy into a period of crisis management, recession, and a new reality of a significantly weaker national currency as 2009 began.

Series: Ancient Towns of Russia

🌱 Common