10 kroner (Hans Christian Andersen) – Denmark

Add to wishlist

Circulating commemorative coins

Commemoration: 200th Anniversary of the Birth of Hans Christian Andersen - Fairy Tales Series - Little Mermaid

Series: Fairytales

Denmark

Context

Material

Diameter: 23.35 mm

Weight: 7 g

Thickness: 2.3 mm

Shape: Round

Composition: Aluminium bronze

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #7434

Value

Exchange value: 10 DKK

Inflation-adjusted value: 14.43 DKK

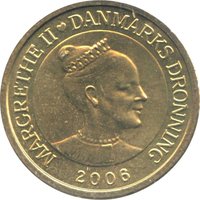

Obverse

Description:

Queen Margrethe in profile.

Inscription:

MARGRETHE II ♥ DANMARKS DRONNING

2005

2005

Translation:

MARGRETHE II ♥ QUEEN OF DENMARK

2005

2005

Script: Latin

Engraver: Mogens Møller

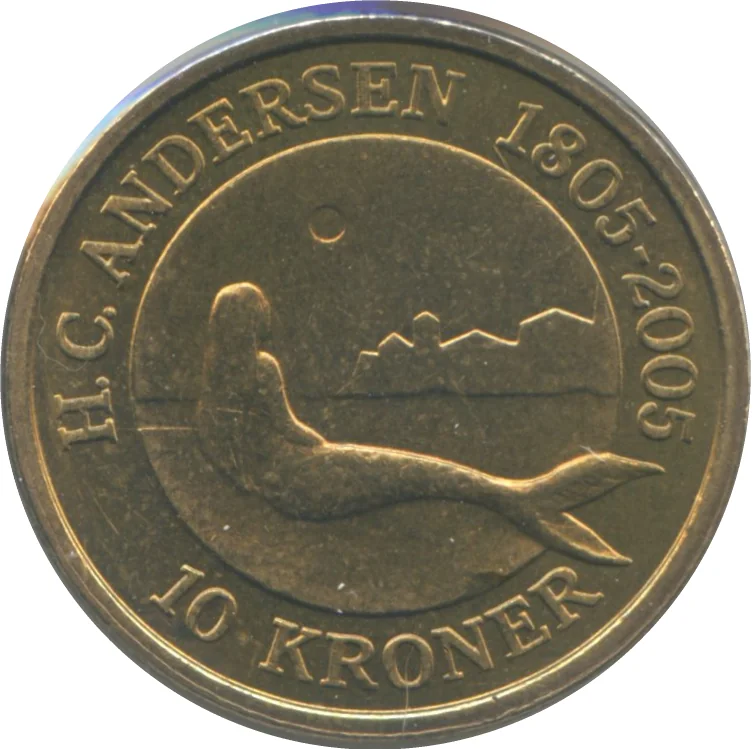

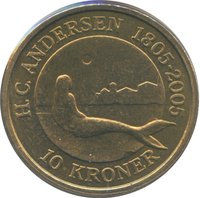

Reverse

Description:

Mermaid gazing at land.

Inscription:

H.C.ANDERSEN 1805-2005

10 KRONER

10 KRONER

Script: Latin

Engraver: Tina Maria Nielsen

Edge

Plain

Categories

| Event> Birth anniversary |

Mints

| Name | Mark |

|---|---|

| Royal Danish Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2005 | — | 1,200,000 |

Historical background

In 2005, Denmark's currency situation was defined by its long-standing and stable membership of the European Exchange Rate Mechanism II (ERM II). Since 1999, the Danish krone (DKK) had been pegged to the euro with a central rate of 7.46038 and a very narrow fluctuation band of ±2.25%. This arrangement was a political compromise following the 2000 referendum where Danes rejected adopting the euro, choosing instead to maintain their national currency while tightly aligning its value to the single currency. The peg was actively managed by Danmarks Nationalbank, which maintained a primary objective of ensuring exchange rate stability, even above controlling domestic inflation.

The Danish economy in 2005 was strong, with low unemployment and a healthy balance of payments, which supported the credibility of the fixed exchange rate policy. There was no significant market pressure against the krone peg during this period; in fact, Danmarks Nationalbank often had to intervene in foreign exchange markets to prevent the krone from appreciating too strongly against the euro, as high interest rate differentials attracted capital inflows. This required the bank to lower its key policy rates, which at times were set below those of the European Central Bank (ECB), a unique situation designed to curb the krone's strength and maintain the agreed parity.

Consequently, monetary policy in Denmark was largely dictated by the requirements of the fixed exchange rate, effectively outsourcing interest rate decisions to the ECB. This meant that while Denmark enjoyed the benefits of currency stability for trade and investment with its largest partner, the Eurozone, it had relinquished the ability to set independent interest rates tailored solely to domestic economic conditions. The system functioned smoothly in 2005, representing a mature and successful example of a unilateral hard peg, providing the stability of the euro without formal membership in the monetary union.

The Danish economy in 2005 was strong, with low unemployment and a healthy balance of payments, which supported the credibility of the fixed exchange rate policy. There was no significant market pressure against the krone peg during this period; in fact, Danmarks Nationalbank often had to intervene in foreign exchange markets to prevent the krone from appreciating too strongly against the euro, as high interest rate differentials attracted capital inflows. This required the bank to lower its key policy rates, which at times were set below those of the European Central Bank (ECB), a unique situation designed to curb the krone's strength and maintain the agreed parity.

Consequently, monetary policy in Denmark was largely dictated by the requirements of the fixed exchange rate, effectively outsourcing interest rate decisions to the ECB. This meant that while Denmark enjoyed the benefits of currency stability for trade and investment with its largest partner, the Eurozone, it had relinquished the ability to set independent interest rates tailored solely to domestic economic conditions. The system functioned smoothly in 2005, representing a mature and successful example of a unilateral hard peg, providing the stability of the euro without formal membership in the monetary union.

Series: Fairytales

🌱 Common