50 Francs – Belgium

Circulating commemorative coins

Commemoration: Brussels Exposition and Railway Centennial

Belgium

Context

Year: 1935

Issuer: Belgium

Ruler: Leopold III

Currency:

(1832—2001)

Demonetization: 2 June 1939

Total mintage: 140,436

Material

References

KM: #Click to copy to clipboard106.1

Numista: #7421

Value

Exchange value: 50 BEF

Bullion value: $42.11

Obverse

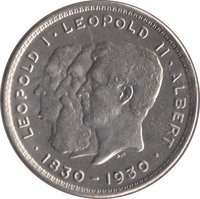

Description:

Saint Michael standing winged on a dragon, dividing value. French text encircles the scene.

Inscription:

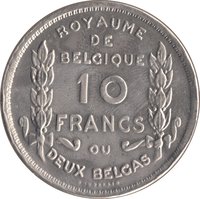

ROYAUME DE BELGIQUE

EXPOSITION DE BRUXELLES

50 FR

EXPOSITION DE BRUXELLES

50 FR

Translation:

Kingdom of Belgium

Brussels Exhibition

50 Francs

Brussels Exhibition

50 Francs

Script: Latin

Language: French

Engraver: Paul Wissaert

Reverse

Description:

Brussels Expo construction years. French text in a semicircle.

Inscription:

CENTENAIRE DES CHEMINS DE FER BELGES

1835 - 1935

1835 - 1935

Translation:

Centenary of the Belgian Railways

1835 - 1935

1835 - 1935

Script: Latin

Language: French

Engraver: Paul Wissaert

Edge

Plain with incused lettering

Legend:

SOUS LE REGNE DU ROI LEOPOLD III

Translation:

Under the Reign of King Leopold III

Language: French

Categories

| Person> Religious figure |

| Object> Cold weapons |

| Mythology> Fantastic animal |

| Object> Armour |

Mints

| Name | Mark |

|---|---|

| Royal Mint of Belgium | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1935 | — | 140,436 |

Historical background

In 1935, Belgium was grappling with the severe economic consequences of the Great Depression, which had exposed the fragility of its financial system and currency. The Belgian franc, which had been painstakingly stabilized and pegged to gold in 1926 after a period of hyperinflation, came under intense speculative pressure. A significant overvaluation, combined with the deflationary policies of the "Gold Bloc" (a group of European nations, including Belgium, committed to maintaining the gold standard), crippled Belgian exports and deepened industrial recession, leading to widespread bankruptcies and high unemployment.

The crisis culminated in the spring of 1935, forcing a fundamental policy shift. Under the new government of Prime Minister Paul van Zeeland, and with crucial advice from monetary expert Maurice Frère, Belgium was forced to abandon the gold standard in March 1935. This decisive move involved a devaluation of the franc by 28%, a measure designed to restore competitiveness, stimulate exports, and break the cycle of deflation. The devaluation was accompanied by a comprehensive reform package, including the creation of the Bank of Belgium (to replace the old National Bank) and the Office of Rediscount and Guarantee, aimed at recapitalizing banks and restoring confidence in the financial sector.

The 1935 devaluation proved to be a turning point for the Belgian economy. It successfully ended the deflationary spiral and marked the beginning of a slow but tangible recovery, distinguishing Belgium from other Gold Bloc countries that resisted devaluation for longer. The episode underscored the limitations of the international gold standard during economic crises and established a new framework for Belgian monetary policy, prioritizing domestic economic stability over a rigid peg to gold. This pragmatic approach would shape Belgium's financial governance in the decades to follow.

The crisis culminated in the spring of 1935, forcing a fundamental policy shift. Under the new government of Prime Minister Paul van Zeeland, and with crucial advice from monetary expert Maurice Frère, Belgium was forced to abandon the gold standard in March 1935. This decisive move involved a devaluation of the franc by 28%, a measure designed to restore competitiveness, stimulate exports, and break the cycle of deflation. The devaluation was accompanied by a comprehensive reform package, including the creation of the Bank of Belgium (to replace the old National Bank) and the Office of Rediscount and Guarantee, aimed at recapitalizing banks and restoring confidence in the financial sector.

The 1935 devaluation proved to be a turning point for the Belgian economy. It successfully ended the deflationary spiral and marked the beginning of a slow but tangible recovery, distinguishing Belgium from other Gold Bloc countries that resisted devaluation for longer. The episode underscored the limitations of the international gold standard during economic crises and established a new framework for Belgian monetary policy, prioritizing domestic economic stability over a rigid peg to gold. This pragmatic approach would shape Belgium's financial governance in the decades to follow.

🌟 Uncommon