Obverse

Description:

Seychelles' coat of arms with the date beneath.

Inscription:

REPUBLIC OF SEYCHELLES

2010

2010

Script: Latin

Reverse

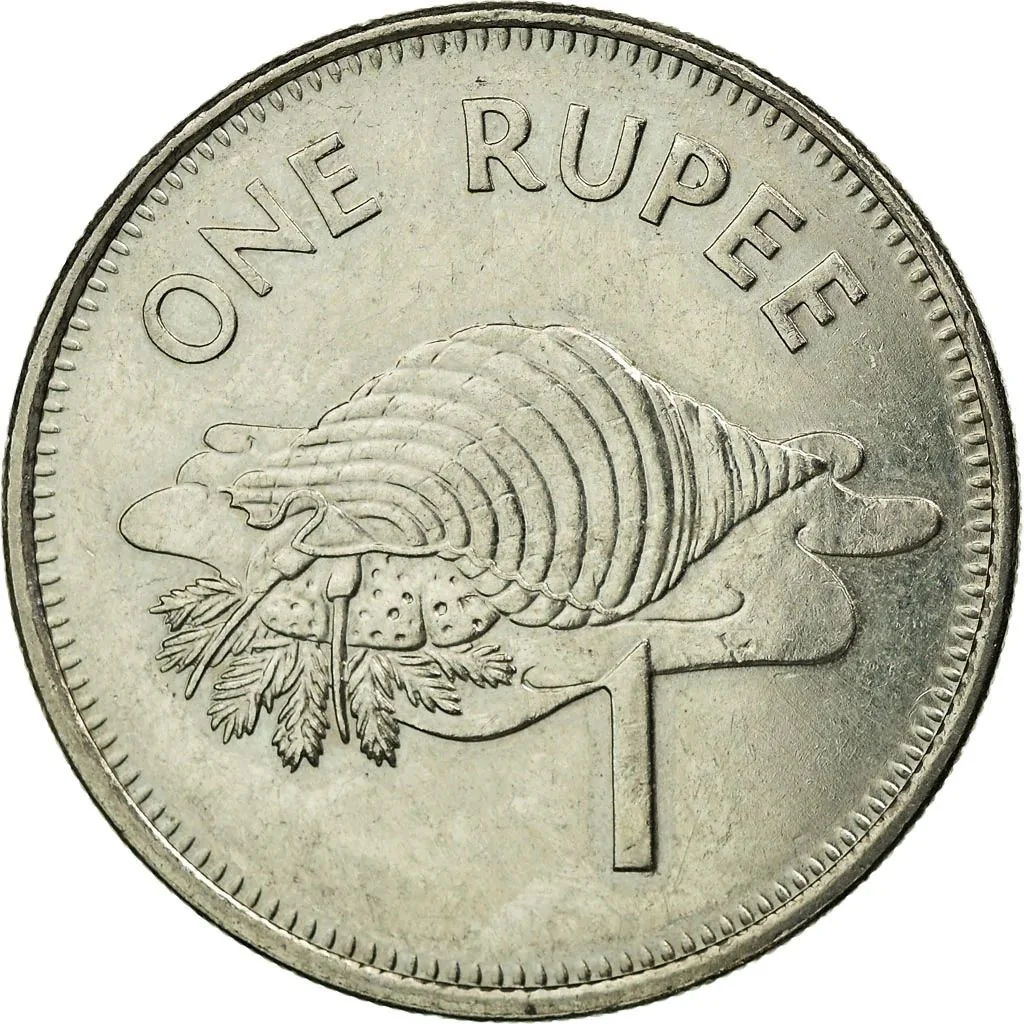

Description:

Triton Conch shell divides the denomination into words above and numerals below.

Inscription:

ONE RUPEE

1

1

Script: Latin

Engraver: Suzanne Danielli

Edge

Reeded

Categories

| Animal> Bird |

| Animal> Fish |

| Animal> Marine invertebrate |

| Symbol> Shell |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2010 | — | — |

Historical background

In 2010, Seychelles was in the midst of a profound economic transformation following a severe balance of payments crisis in 2008. The government, under President James Michel, had embarked on a bold and rigorous reform program supported by a two-year, $31 million Stand-By Arrangement with the International Monetary Fund (IMF). A cornerstone of this reform was the liberalization of the foreign exchange market in November 2008, which abandoned a fixed exchange rate and allowed the Seychellois rupee (SCR) to float. By 2010, the rupee had stabilized after an initial sharp devaluation, trading around SCR 12 to the US dollar, a significant adjustment from the previous artificially pegged rate of SCR 5.5.

The currency float, combined with strict fiscal discipline and the removal of most exchange controls, was yielding positive results by 2010. Foreign exchange reserves, which had been nearly depleted, were being rebuilt, providing a critical buffer for the import-dependent island nation. This restored confidence in the currency and enabled a functioning interbank market for foreign exchange. The situation marked a dramatic shift from the days of chronic shortages and a thriving black market, as businesses and citizens could now legally access foreign currency for transactions.

Consequently, 2010 represented a year of consolidation and emerging recovery. The IMF completed its final review under the Stand-By Arrangement in July, noting that the reforms had "yielded impressive results." While challenges remained, including high public debt and vulnerability to external shocks, the currency situation was no longer in crisis. The successful stabilization of the rupee laid the foundation for the subsequent economic growth, driven by a rebound in the crucial tourism and fisheries sectors, setting Seychelles on a more sustainable macroeconomic path.

The currency float, combined with strict fiscal discipline and the removal of most exchange controls, was yielding positive results by 2010. Foreign exchange reserves, which had been nearly depleted, were being rebuilt, providing a critical buffer for the import-dependent island nation. This restored confidence in the currency and enabled a functioning interbank market for foreign exchange. The situation marked a dramatic shift from the days of chronic shortages and a thriving black market, as businesses and citizens could now legally access foreign currency for transactions.

Consequently, 2010 represented a year of consolidation and emerging recovery. The IMF completed its final review under the Stand-By Arrangement in July, noting that the reforms had "yielded impressive results." While challenges remained, including high public debt and vulnerability to external shocks, the currency situation was no longer in crisis. The successful stabilization of the rupee laid the foundation for the subsequent economic growth, driven by a rebound in the crucial tourism and fisheries sectors, setting Seychelles on a more sustainable macroeconomic path.

🌱 Common