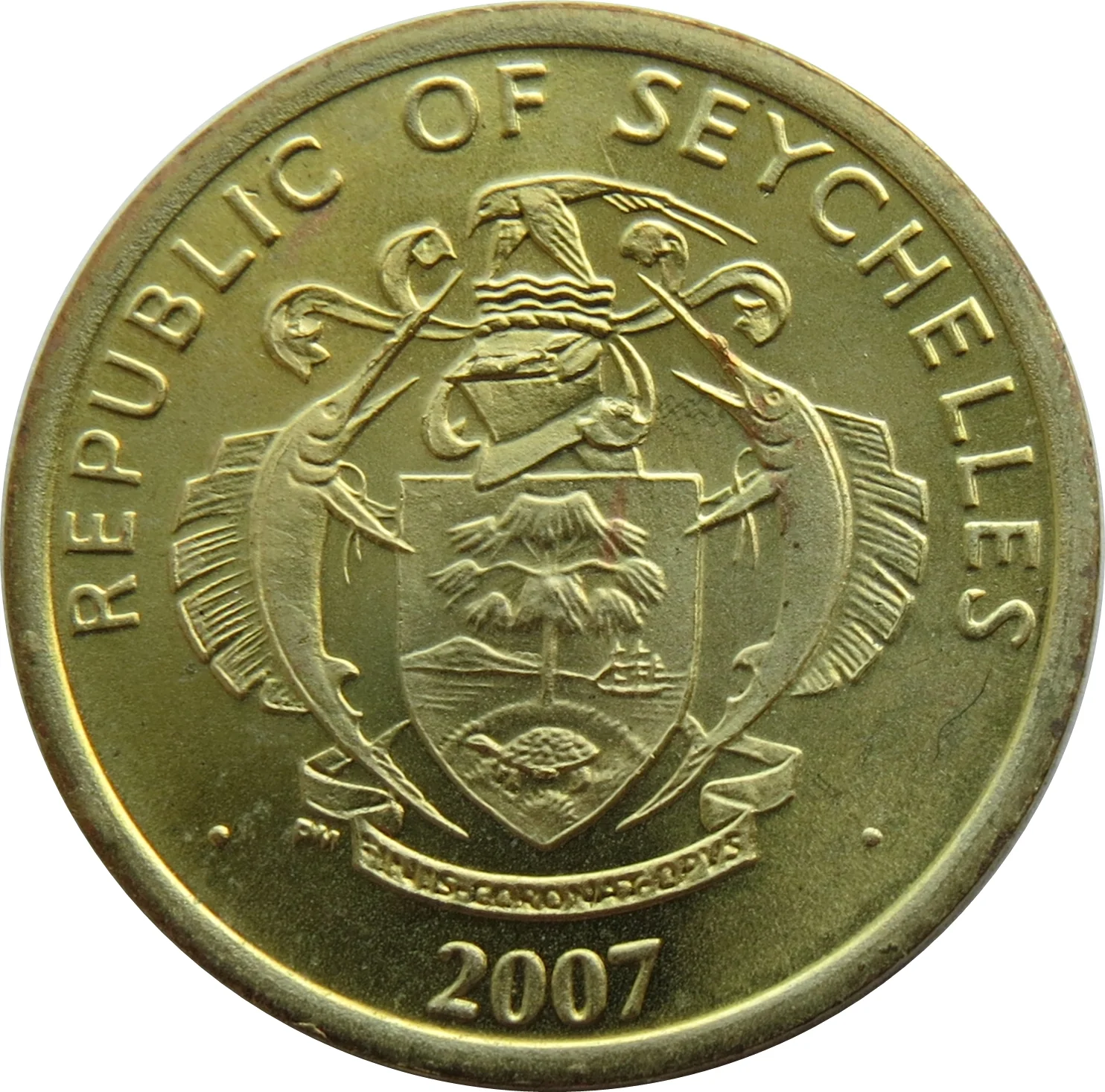

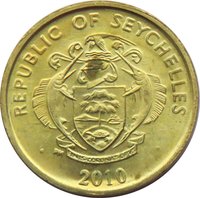

Obverse

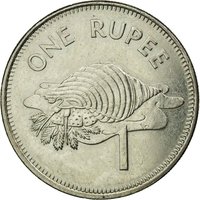

Reverse

Description:

Fresh catch, fair price.

Inscription:

10

TEN CENTS

TEN CENTS

Script: Latin

Engraver: Robert Elderton

Edge

Plain

Mints

| Name | Mark |

|---|---|

| South African Mint | — |

| Pobjoy Mint | PM |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2007 | PM | — | ||

| 2012 | — | — |

Historical background

In 2007, Seychelles was on the brink of a profound economic crisis, with its currency situation at the very heart of the turmoil. The country operated under a severely overvalued official exchange rate for the Seychellois rupee (SCR), pegged at approximately SCR 5.5 to the US dollar. This peg was unsustainable, maintained through strict foreign exchange controls that created a crippling parallel black market where the rupee traded for as little as SCR 13 to the dollar. The disparity between the official and black-market rates stifled legitimate foreign investment, encouraged capital flight, and led to critical shortages of imported goods, including fuel and food.

The root causes of this crisis were decades of persistent fiscal deficits, high public debt, and a chronic balance of payments shortfall. The government had long financed its spending by borrowing from the domestic banking system, which the Central Bank of Seychelles accommodated by printing money. This led to high inflation and eroded foreign reserves, making it impossible to defend the official peg. By 2007, foreign exchange reserves had dwindled to cover less than two weeks of imports, leaving the economy vulnerable to external shocks and unable to meet its sovereign debt obligations.

Consequently, 2008 became the pivotal year for change, with the decisions of late 2007 setting the stage. Facing imminent collapse, the government entered negotiations with the International Monetary Fund (IMF) in 2007. This culminated in a comprehensive reform program announced in November 2008, which included the decisive move to liberalize the exchange regime. The rupee was floated, leading to an immediate and significant devaluation to a market-determined rate, which initially settled around SCR 16 to the US dollar. Thus, the currency situation of 7 represented the final, unsustainable chapter of a controlled regime, necessitating the dramatic structural reforms that would follow.

The root causes of this crisis were decades of persistent fiscal deficits, high public debt, and a chronic balance of payments shortfall. The government had long financed its spending by borrowing from the domestic banking system, which the Central Bank of Seychelles accommodated by printing money. This led to high inflation and eroded foreign reserves, making it impossible to defend the official peg. By 2007, foreign exchange reserves had dwindled to cover less than two weeks of imports, leaving the economy vulnerable to external shocks and unable to meet its sovereign debt obligations.

Consequently, 2008 became the pivotal year for change, with the decisions of late 2007 setting the stage. Facing imminent collapse, the government entered negotiations with the International Monetary Fund (IMF) in 2007. This culminated in a comprehensive reform program announced in November 2008, which included the decisive move to liberalize the exchange regime. The rupee was floated, leading to an immediate and significant devaluation to a market-determined rate, which initially settled around SCR 16 to the US dollar. Thus, the currency situation of 7 represented the final, unsustainable chapter of a controlled regime, necessitating the dramatic structural reforms that would follow.

🌱 Common