20 Cents – Australia

Australia

Context

Material

Diameter: 28.52 mm

Weight: 11.31 g

Thickness: 2 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard1857

Numista: #73472

Value

Exchange value: 0.20 AUD = $0.14

Inflation-adjusted value: 0.28 AUD

Obverse

Description:

Queen Elizabeth IV, facing right, wearing the Girls of Great Britain and Ireland Tiara.

Inscription:

ELIZABETH II

AUSTRALIA 2012

IRB

AUSTRALIA 2012

IRB

Script: Latin

Designer: Ian Rank-Broadley

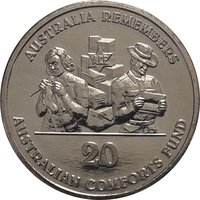

Reverse

Description:

Image of Australia's first merchant ship, the SS River Loddon, with the Australian Merchant Navy crest.

Inscription:

AUSTRALIA REMEMBERS

MN

20

MERCHANT NAVY

MN

20

MERCHANT NAVY

Script: Latin

Designer: Wojciech Pietranik

Edge

Reeded

Categories

| Transportation> Watercraft |

| History> War |

Mints

| Name | Mark |

|---|---|

| Royal Australian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2012 | — | 20,000 | BU |

Historical background

In 2012, Australia’s currency situation was characterised by the persistent strength of the Australian dollar (AUD), which traded at historically high levels against the US dollar, often above parity and reaching peaks near USD 1.08. This strength was primarily driven by the ongoing commodities boom, with high demand from China for Australia’s iron ore and coal exports. Furthermore, Australia’s relatively high interest rates, compared to the near-zero rates in the United States, Japan, and Europe following the Global Financial Crisis, attracted significant capital inflows, reinforcing the currency's appeal as a high-yielding, safe-haven asset.

The high dollar created a pronounced two-speed economy, presenting significant challenges for key non-mining sectors. Industries such as manufacturing, tourism, and education faced intense pressure, as their exports and services became more expensive for international buyers and domestic consumers found imported goods cheaper. The Reserve Bank of Australia (RBA) responded by adopting a more dovish monetary policy stance, cutting the official cash rate from 4.25% at the start of the year to 3.00% by December in an effort to stimulate domestic demand and alleviate the disinflationary pressure exerted by the strong currency.

Despite these challenges, the AUD's strength also reflected underlying economic resilience, with Australia enjoying low unemployment, contained public debt, and a continued terms of trade boom. The situation underscored the complex management task for policymakers, who balanced the benefits of a strong currency—like cheaper imports and contained inflation—against its sectoral damage. By year's end, with signs of a moderating mining investment peak and easing commodity prices, the currency began a gradual retreat from its highs, setting the stage for a rebalancing of the economy in the following years.

The high dollar created a pronounced two-speed economy, presenting significant challenges for key non-mining sectors. Industries such as manufacturing, tourism, and education faced intense pressure, as their exports and services became more expensive for international buyers and domestic consumers found imported goods cheaper. The Reserve Bank of Australia (RBA) responded by adopting a more dovish monetary policy stance, cutting the official cash rate from 4.25% at the start of the year to 3.00% by December in an effort to stimulate domestic demand and alleviate the disinflationary pressure exerted by the strong currency.

Despite these challenges, the AUD's strength also reflected underlying economic resilience, with Australia enjoying low unemployment, contained public debt, and a continued terms of trade boom. The situation underscored the complex management task for policymakers, who balanced the benefits of a strong currency—like cheaper imports and contained inflation—against its sectoral damage. By year's end, with signs of a moderating mining investment peak and easing commodity prices, the currency began a gradual retreat from its highs, setting the stage for a rebalancing of the economy in the following years.

Series: Australia Remembers

⭐ Rare