6 Pence – United Kingdom

United Kingdom

Context

Years: 1937–1946

Issuer: United Kingdom

Ruler: George VI

Currency:

(1158—1970)

Demonetization: 30 June 1980

Total mintage: 321,665,204

Material

References

KM: #Click to copy to clipboard852

Numista: #1125

Value

Bullion value: $4.05

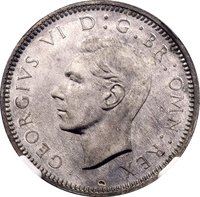

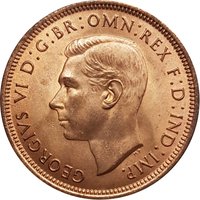

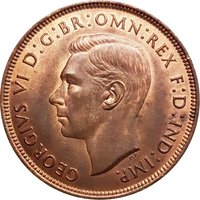

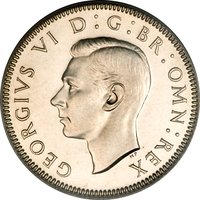

Obverse

Description:

King George VI, uncrowned, left-facing portrait, legend encircling.

Inscription:

GEORGIVS VI D:G:BR:OMN:REX

HP

HP

Translation:

George VI by the Grace of God King of all the Britains

Defender of the Faith Emperor of India

Defender of the Faith Emperor of India

Script: Latin

Language: Latin

Engraver: Thomas Humphrey Paget

Reverse

Description:

Royal cypher divides date, legend above, value below.

Inscription:

FID·DEF· ·IND·IMP

19 GRI 46

K · G

SIXPENCE

19 GRI 46

K · G

SIXPENCE

Translation:

Faith Defender · Indian Emperor

19 GRI 46

K · G

SIXPENCE

19 GRI 46

K · G

SIXPENCE

Script: Latin

Engraver: George Kruger Gray

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1937 | — | 22,302,500 | ||

| 1937 | — | 4 | Proof | |

| 1938 | — | 13,402,700 | ||

| 1938 | — | — | Proof | |

| 1939 | — | — | Proof | |

| 1939 | — | 28,670,300 | ||

| 1940 | — | 20,875,100 | ||

| 1940 | — | — | Proof | |

| 1941 | — | 23,186,600 | ||

| 1941 | — | — | Proof | |

| 1942 | — | 44,942,700 | ||

| 1942 | — | — | Proof | |

| 1943 | — | 46,927,100 | ||

| 1943 | — | — | Proof | |

| 1944 | — | 37,952,600 | ||

| 1944 | — | — | Proof | |

| 1945 | — | 39,939,200 | ||

| 1945 | — | — | Proof | |

| 1946 | — | — | Proof | |

| 1946 | — | 43,466,400 |

Historical background

In 1937, the United Kingdom's currency was underpinned by the Sterling Area, an informal monetary bloc where member nations pegged their currencies to the British pound and held their reserves in London. This system, which had evolved after Britain left the Gold Standard in 1931, granted the UK significant economic influence and provided a zone of exchange rate stability for its trading partners, particularly within the Empire. The pound itself was a managed currency, with its value influenced by the Treasury and the Bank of England through the Exchange Equalisation Account, established in 1932 to smooth out volatile fluctuations without being tied to a fixed gold price.

Domestically, the economy was in a state of cautious recovery from the Great Depression, but this was overshadowed by growing rearmament expenditures due to rising geopolitical tensions in Europe. Chancellor of the Exchequer Sir John Simon was grappling with the need to fund a rapidly expanding military budget while trying to avoid inflationary pressure on the pound. The currency's external value was relatively stable but vulnerable, as the government's "cheap money" policy of low interest rates, maintained to stimulate business investment, also risked capital outflows if confidence wavered.

Overall, the sterling in 1937 was in a period of precarious equilibrium. It benefited from the stability of the Sterling Area and controlled management, yet it faced underlying strains from the dual pressures of massive rearmament and a delicate balance of payments. The financial authorities were effectively walking a tightrope, prioritising domestic economic stability and defence preparedness over a return to international monetary orthodoxy, a position that would be severely tested in the coming war years.

Domestically, the economy was in a state of cautious recovery from the Great Depression, but this was overshadowed by growing rearmament expenditures due to rising geopolitical tensions in Europe. Chancellor of the Exchequer Sir John Simon was grappling with the need to fund a rapidly expanding military budget while trying to avoid inflationary pressure on the pound. The currency's external value was relatively stable but vulnerable, as the government's "cheap money" policy of low interest rates, maintained to stimulate business investment, also risked capital outflows if confidence wavered.

Overall, the sterling in 1937 was in a period of precarious equilibrium. It benefited from the stability of the Sterling Area and controlled management, yet it faced underlying strains from the dual pressures of massive rearmament and a delicate balance of payments. The financial authorities were effectively walking a tightrope, prioritising domestic economic stability and defence preparedness over a return to international monetary orthodoxy, a position that would be severely tested in the coming war years.

🌱 Very Common