200 Escudos – Portugal

Portugal

Context

Year: 1994

Issuer: Portugal

Period:

(since 1974)

Currency:

(1911—2001)

Demonetization: 28 February 2002

Total mintage: 950,000

Material

Diameter: 36 mm

Weight: 21.1 g

Thickness: 2.8 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #Click to copy to clipboard673

Numista: #7194

Value

Exchange value: 200 PTE

Inflation-adjusted value: 409.27 PTE

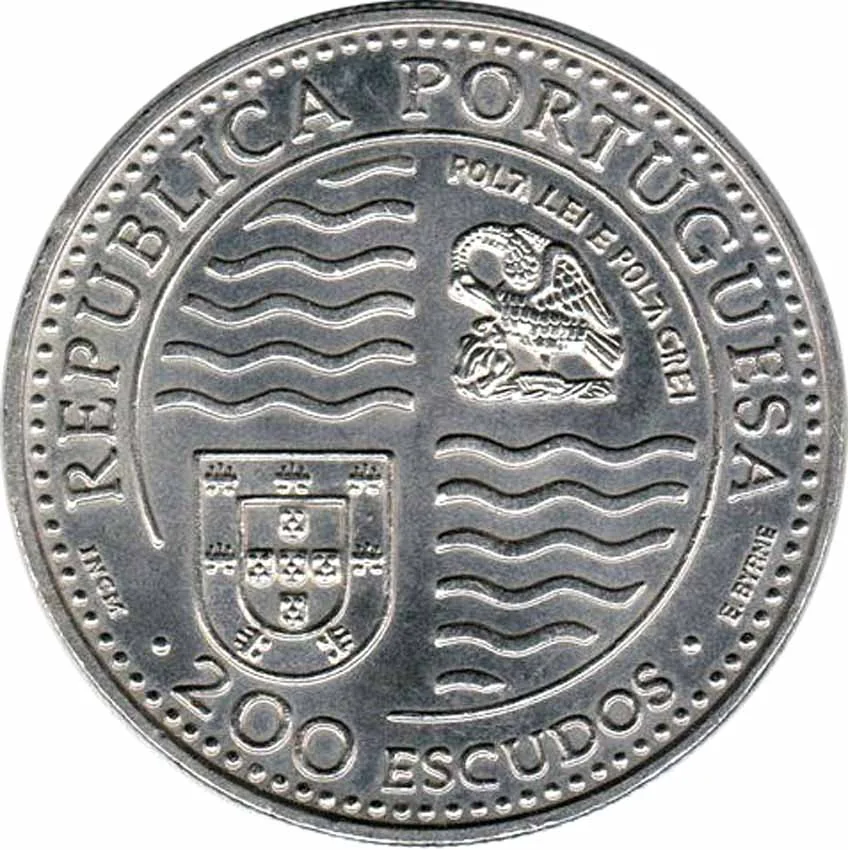

Obverse

Description:

A shield quartered: top left and bottom right feature wavy lines for navigation; bottom left displays the Portuguese coat of arms; top right shows King John II's "pelican in her piety" with the motto "Pela Lei e Pela Grei." The rim states the country and value, surrounded by a circle of pearls.

Inscription:

REPUBLICA PORTUGUESA

POLÁ LEI E POLÁ GREI

INCM · 200 ESCUDOS · E.BYRNE

POLÁ LEI E POLÁ GREI

INCM · 200 ESCUDOS · E.BYRNE

Translation:

By the Law and by the People

INCM · 200 Escudos · E.Byrne

INCM · 200 Escudos · E.Byrne

Script: Latin

Languages: Portuguese, Latin

Engraver: Eloísa Byrne

Reverse

Description:

Portrait of King João II of Portugal (d. 1495), crowned and holding a model 16th-century caravel.

Inscription:

D. JOÁO II : PRINCIPE PERFEITO : 1495·1995

Translation:

D. John II: The Perfect Prince: 1495-1995

Script: Latin

Language: Portuguese

Engraver: Eloísa Byrne

Edge

Milled

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | incm |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1994 | incm | 950,000 |

Historical background

In 1994, Portugal's currency situation was defined by its strategic and disciplined participation in the European Monetary System (EMS) and its determined march toward European Economic and Monetary Union (EMU). The country's currency, the escudo (PTE), was operating within the EMS Exchange Rate Mechanism (ERM), which required it to maintain a fixed but adjustable parity against a central European Currency Unit (ECU) and, by extension, relative stability against other member currencies, most importantly the Deutsche Mark. This period followed a significant devaluation in 1992, which had realigned the escudo's central rate to a more competitive level, and by 1994, the currency was demonstrating notable stability within its narrow fluctuation band of ±2.25%.

This stability was not accidental but the result of a concerted national policy effort. The Banco de Portugal, the country's central bank, pursued a tight monetary policy focused on inflation reduction and exchange rate stability, often shadowing the policies of the German Bundesbank to maintain credibility. High interest rates were used to defend the escudo's peg and curb domestic demand, a necessary but painful strategy that came with the economic cost of subdued growth. The primary driver was political: fulfilling the Maastricht Treaty convergence criteria on inflation, interest rates, budget deficits, and exchange rate stability was the paramount national objective to secure Portugal's place in the first wave of the single European currency.

Consequently, the currency landscape in 1994 was one of transition and preparation. The escudo was effectively in a "hard currency" regime, serving as a training ground for the impending loss of monetary sovereignty. Financial markets and institutions were beginning to adapt to a future without the escudo, while the government's fiscal austerity measures aimed to rein in the public deficit to meet the Maastricht targets. Thus, the story of the escudo in 1994 is one of a currency being carefully managed not for its own long-term future, but to ensure its orderly retirement and Portugal's entry into the Eurozone, which was ultimately achieved on January 1, 1999.

This stability was not accidental but the result of a concerted national policy effort. The Banco de Portugal, the country's central bank, pursued a tight monetary policy focused on inflation reduction and exchange rate stability, often shadowing the policies of the German Bundesbank to maintain credibility. High interest rates were used to defend the escudo's peg and curb domestic demand, a necessary but painful strategy that came with the economic cost of subdued growth. The primary driver was political: fulfilling the Maastricht Treaty convergence criteria on inflation, interest rates, budget deficits, and exchange rate stability was the paramount national objective to secure Portugal's place in the first wave of the single European currency.

Consequently, the currency landscape in 1994 was one of transition and preparation. The escudo was effectively in a "hard currency" regime, serving as a training ground for the impending loss of monetary sovereignty. Financial markets and institutions were beginning to adapt to a future without the escudo, while the government's fiscal austerity measures aimed to rein in the public deficit to meet the Maastricht targets. Thus, the story of the escudo in 1994 is one of a currency being carefully managed not for its own long-term future, but to ensure its orderly retirement and Portugal's entry into the Eurozone, which was ultimately achieved on January 1, 1999.

Series: V-Portuguese Discoveries

🌱 Very Common