100 Escudos – Portugal

Circulating commemorative coins

Commemoration: International Year of Disabled Persons

Series: System 1981-2001

Portugal

Context

Year: 1984

Issuer: Portugal

Period:

(since 1974)

Currency:

(1911—2001)

Demonetized: Yes

Total mintage: 10,000

Material

Diameter: 34 mm

Weight: 17 g

Thickness: 2.4 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #Click to copy to clipboard625

Numista: #7165

Value

Exchange value: 100 PTE

Inflation-adjusted value: 712.97 PTE

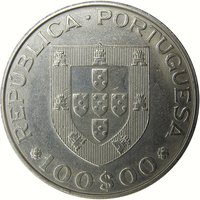

Obverse

Description:

Heraldic emblem

Inscription:

REPUBLICA·PORTUGUESA

100$00

100$00

Translation:

Portuguese Republic

100$00

100$00

Script: Latin

Language: Portuguese

Engraver: Armando Matos Simões

Reverse

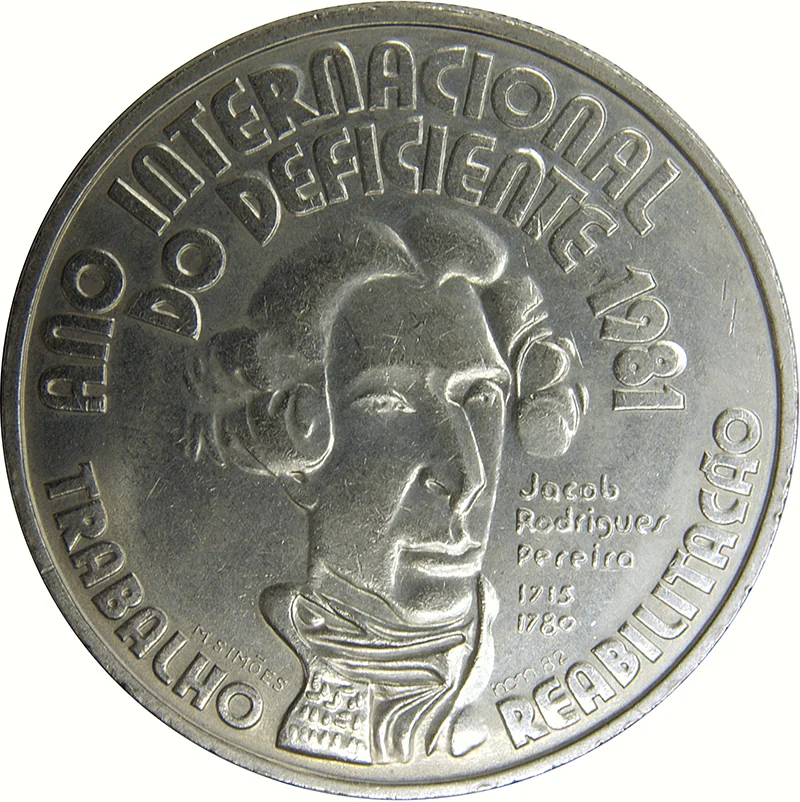

Description:

Stylized head, quarter-right view.

Inscription:

ANO INTERNATIONAL DO DEFICIENTE 1981

TRABALHO REABILITACÃO

Jacob

Rodrigues

Pereira

1715

1780

M. SIMÕES incm82

TRABALHO REABILITACÃO

Jacob

Rodrigues

Pereira

1715

1780

M. SIMÕES incm82

Translation:

International Year of the Disabled Person 1981

Work Rehabilitation

Jacob

Rodrigues

Pereira

1715

1780

M. SIMÕES incm82

Work Rehabilitation

Jacob

Rodrigues

Pereira

1715

1780

M. SIMÕES incm82

Script: Latin

Language: Portuguese

Engraver: Armando Matos Simões

Edge

Milled

Categories

| Symbols> Coat of Arms |

| Health |

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1984 | — | 10,000 |

Historical background

In 1984, Portugal's currency situation was defined by its ongoing transition from the authoritarian Estado Novo regime and its integration into the European Economic Community (EEC). The national currency was the Portuguese escudo (PTE), which operated under a managed float but was effectively pegged to a basket of currencies, heavily weighted toward the US dollar and the Deutsche Mark. This peg was managed by the Bank of Portugal to provide stability and control inflation, which remained a persistent challenge following the economic turbulence and oil shocks of the 1970s.

The broader economic context was one of structural adjustment and modernization, driven by the conditions of Portugal's 1977 IMF loan and its impending full EEC membership in 1986. The escudo was subject to periodic devaluations to maintain export competitiveness and correct external imbalances. In 1983, a major 12% devaluation had been implemented as part of a stringent austerity package, and the currency's value in 1984 was still reflecting those corrective measures. High public debt, a large state-owned sector, and political instability following the 1974 Carnation Revolution continued to pressure the escudo's stability and Portugal's foreign exchange reserves.

Looking forward, 1984 was a year of preparation for deeper European integration. Policymakers were aligning monetary and fiscal policies with EEC partners, laying the groundwork for future participation in the European Monetary System (EMS), which Portugal would join in 1992. Thus, the escudo's management in 1984 was not just about immediate economic stability, but also a strategic stepping stone toward eventually replacing the national currency with the euro decades later, embedding Portugal firmly within the European financial architecture.

The broader economic context was one of structural adjustment and modernization, driven by the conditions of Portugal's 1977 IMF loan and its impending full EEC membership in 1986. The escudo was subject to periodic devaluations to maintain export competitiveness and correct external imbalances. In 1983, a major 12% devaluation had been implemented as part of a stringent austerity package, and the currency's value in 1984 was still reflecting those corrective measures. High public debt, a large state-owned sector, and political instability following the 1974 Carnation Revolution continued to pressure the escudo's stability and Portugal's foreign exchange reserves.

Looking forward, 1984 was a year of preparation for deeper European integration. Policymakers were aligning monetary and fiscal policies with EEC partners, laying the groundwork for future participation in the European Monetary System (EMS), which Portugal would join in 1992. Thus, the escudo's management in 1984 was not just about immediate economic stability, but also a strategic stepping stone toward eventually replacing the national currency with the euro decades later, embedding Portugal firmly within the European financial architecture.

Series: System 1981-2001

🌱 Very Common