½ dollar – United States

Add to wishlist

United States

Context

Years: 1971–2025

Issuer: United States

Period:

(since 1776)

Currency:

(since 1785)

Subdivision: ½ dollar = 50 Cents

Total mintage: 2,582,911,403

Material

References

KM: #

Numista: #6918

Value

Exchange value: ½ USD = $0.50

Inflation-adjusted value: 4.13 USD

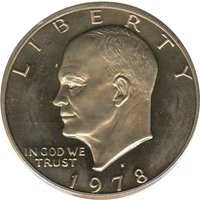

Obverse

Description:

JFK portrait left, date below.

Inscription:

LIBERTY

GR

IN GOD WE TRUST

D

2023

GR

IN GOD WE TRUST

D

2023

Script: Latin

Designer and engraver: Gilroy Roberts

Reverse

Description:

U.S. presidential seal: An eagle with a shield on its chest holds an olive branch and arrows, with "E PLURIBUS UNUM" in its beak, encircled by 50 stars.

Inscription:

UNITED STATES OF AMERICA

E PLURIBUS UNUM

FG

HALF DOLLAR

E PLURIBUS UNUM

FG

HALF DOLLAR

Translation:

UNITED STATES OF AMERICA

OUT OF MANY, ONE

FG

HALF DOLLAR

OUT OF MANY, ONE

FG

HALF DOLLAR

Script: Latin

Designer and engraver: Frank Gasparro

Edge

Reeded

Categories

| Animal> Bird> Eagle |

| Person> Politician |

| Symbols> Coat of Arms |

| Object> Cold weapons |

Mints

| Name | Mark |

|---|---|

| United States Mint of Philadelphia | — |

| United States Mint of Denver | D |

| United States Mint of Philadelphia | P |

| United States Mint of San Francisco | S |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1971 | — | 155,640,000 | ||

| 1971 | D | 302,097,424 | ||

| 1971 | S | 3,244,183 | Proof | |

| 1972 | D | 141,890,000 | ||

| 1972 | — | 153,180,000 | ||

| 1972 | S | 3,267,667 | Proof | |

| 1973 | — | 64,964,000 | ||

| 1973 | D | 83,171,400 | ||

| 1973 | S | 2,767,624 | Proof | |

| 1974 | — | 201,596,000 | ||

| 1974 | D | 79,066,300 | ||

| 1974 | S | 2,617,350 | Proof | |

| 1977 | — | 43,598,000 | ||

| 1977 | D | 31,449,106 | ||

| 1977 | S | 3,251,152 | Proof | |

| 1978 | — | 14,350,000 | ||

| 1978 | D | 13,765,799 | ||

| 1978 | S | 3,127,788 | Proof | |

| 1979 | — | 68,312,000 | ||

| 1979 | D | 15,815,422 | ||

| 1979 | S | 3,677,175 | Proof | |

| 1980 | D | 33,456,449 | ||

| 1980 | P | 44,134,000 | ||

| 1980 | S | 3,547,030 | Proof | |

| 1981 | D | 27,839,533 | ||

| 1981 | P | 29,544,000 | ||

| 1981 | S | 4,063,083 | Proof | |

| 1982 | D | 13,140,102 | ||

| 1982 | P | 10,819,000 | ||

| 1982 | S | 3,857,479 | Proof | |

| 1983 | — | — | ||

| 1983 | D | 32,472,244 | ||

| 1983 | P | 34,139,000 | ||

| 1983 | S | 3,279,126 | Proof | |

| 1984 | D | 26,262,158 | ||

| 1984 | S | 3,065,110 | Proof | |

| 1984 | P | 26,029,000 | ||

| 1985 | D | 19,814,034 | ||

| 1985 | P | 18,706,962 | ||

| 1985 | S | 3,962,138 | Proof | |

| 1986 | D | 15,336,145 | ||

| 1986 | P | 13,107,633 | ||

| 1986 | S | 2,411,180 | Proof | |

| 1987 | D | 2,890,758 | BU | |

| 1987 | P | 2,890,758 | BU | |

| 1987 | S | 4,407,728 | Proof | |

| 1988 | P | 13,626,000 | ||

| 1988 | D | 12,000,096 | ||

| 1988 | S | 3,262,948 | Proof | |

| 1989 | D | 23,000,216 | ||

| 1989 | P | 24,542,000 | ||

| 1989 | S | 3,220,194 | Proof | |

| 1990 | D | 20,096,242 | ||

| 1990 | P | 22,780,000 | ||

| 1990 | S | 3,299,559 | Proof | |

| 1991 | D | 15,054,678 | ||

| 1991 | P | 14,874,000 | ||

| 1991 | S | 2,867,787 | Proof | |

| 1992 | D | 17,000,106 | ||

| 1992 | P | 17,628,000 | ||

| 1992 | S | 2,858,981 | Proof | |

| 1993 | D | 15,000,006 | ||

| 1993 | P | 15,510,000 | ||

| 1993 | S | 2,633,439 | Proof | |

| 1994 | D | 23,828,110 | ||

| 1994 | P | 23,718,000 | ||

| 1994 | S | 2,484,594 | Proof | |

| 1995 | D | 26,288,000 | ||

| 1995 | P | 26,496,000 | ||

| 1995 | S | 2,010,384 | Proof | |

| 1996 | D | 24,744,000 | ||

| 1996 | P | 24,442,000 | ||

| 1996 | S | 2,085,191 | Proof | |

| 1997 | D | 19,876,000 | ||

| 1997 | P | 20,882,000 | ||

| 1997 | S | 1,975,000 | Proof | |

| 1998 | D | 15,064,000 | ||

| 1998 | P | 15,646,000 | ||

| 1998 | S | 2,078,494 | Proof | |

| 1999 | D | 10,682,000 | ||

| 1999 | P | 8,900,000 | ||

| 1999 | S | 2,557,897 | Proof | |

| 2000 | D | 19,466,000 | ||

| 2000 | P | 22,600,000 | ||

| 2000 | S | 3,082,944 | Proof | |

| 2001 | D | 19,504,000 | ||

| 2001 | P | 21,200,000 | ||

| 2001 | S | 2,235,000 | Proof | |

| 2002 | D | 2,500,000 | BU | |

| 2002 | P | 3,100,000 | BU | |

| 2002 | S | 2,268,913 | Proof | |

| 2003 | D | 2,500,000 | BU | |

| 2003 | P | 2,500,000 | BU | |

| 2003 | S | 2,076,165 | Proof | |

| 2004 | D | 2,900,000 | BU | |

| 2004 | P | 2,900,000 | BU | |

| 2004 | S | 1,789,488 | Proof | |

| 2005 | D | 1,160,000 | ||

| 2005 | D | 3,500,000 | BU | |

| 2005 | P | 3,800,000 | BU | |

| 2005 | P | 1,160,000 | ||

| 2005 | S | 2,275,000 | Proof | |

| 2006 | D | 2,000,000 | BU | |

| 2006 | D | 847,361 | ||

| 2006 | P | 2,400,000 | BU | |

| 2006 | P | 847,361 | ||

| 2006 | S | 1,934,965 | Proof | |

| 2007 | D | 2,400,000 | BU | |

| 2007 | D | 895,628 | ||

| 2007 | P | 2,400,000 | BU | |

| 2007 | P | 895,628 | ||

| 2007 | S | 1,384,797 | Proof | |

| 2008 | D | 1,700,000 | BU | |

| 2008 | D | 745,464 | ||

| 2008 | P | 1,700,000 | BU | |

| 2008 | P | 745,464 | ||

| 2008 | S | 1,377,424 | Proof | |

| 2009 | D | 1,900,000 | BU | |

| 2009 | D | 784,614 | ||

| 2009 | P | 1,900,000 | BU | |

| 2009 | P | 784,614 | ||

| 2009 | S | 1,477,967 | Proof | |

| 2010 | D | 1,800,000 | BU | |

| 2010 | D | 583,897 | ||

| 2010 | P | 1,700,000 | BU | |

| 2010 | P | 583,897 | ||

| 2010 | S | 1,103,950 | Proof | |

| 2011 | D | 1,700,000 | BU | |

| 2011 | P | 1,750,000 | BU | |

| 2011 | S | 1,098,835 | Proof | |

| 2012 | D | 1,700,000 | BU | |

| 2012 | P | 1,800,000 | BU | |

| 2012 | S | 794,002 | Proof | |

| 2013 | S | 821,031 | Proof | |

| 2013 | D | 4,600,000 | BU | |

| 2013 | P | 5,000,000 | BU | |

| 2014 | D | 2,100,000 | ||

| 2014 | P | 2,500,000 | BU | |

| 2014 | P | 197,608 | ||

| 2014 | S | 767,977 | Proof | |

| 2015 | D | 2,300,000 | BU | |

| 2015 | P | 2,300,000 | BU | |

| 2015 | S | 711,952 | Proof | |

| 2016 | P | 2,100,000 | BU | |

| 2016 | D | 2,100,000 | BU | |

| 2016 | S | 621,384 | Proof | |

| 2017 | D | 2,900,000 | BU | |

| 2017 | P | 1,800,000 | BU | |

| 2017 | S | 225,000 | ||

| 2017 | S | 592,890 | Proof | |

| 2018 | D | 1,900,000 | BU | |

| 2018 | P | 1,900,000 | BU | |

| 2018 | S | 535,221 | Proof | |

| 2019 | D | 1,700,000 | BU | |

| 2019 | D | 50,000 | ||

| 2019 | P | 1,700,000 | BU | |

| 2019 | S | 100,000 | Proof | |

| 2020 | D | 3,400,000 | BU | |

| 2020 | P | 2,300,000 | BU | |

| 2020 | S | — | Proof | |

| 2021 | D | 7,700,000 | ||

| 2021 | P | 5,400,000 | ||

| 2021 | S | — | Proof | |

| 2022 | D | 4,900,000 | ||

| 2022 | P | 4,800,000 | ||

| 2022 | S | — | Proof | |

| 2023 | D | 27,800,000 | ||

| 2023 | P | 30,200,000 | ||

| 2023 | S | — | Proof | |

| 2024 | D | 21,900,000 | ||

| 2024 | P | 15,700,000 | ||

| 2024 | S | — | Proof | |

| 2025 | D | — | ||

| 2025 | P | — | ||

| 2025 | S | — | Proof |

Historical background

In 1971, the United States faced a mounting international monetary crisis rooted in the Bretton Woods system established after World War II. This system had fixed global currencies to the U.S. dollar, which was in turn convertible to gold at $35 per ounce for foreign governments. However, by the late 1960s, persistent U.S. trade deficits, heavy military and social spending, and a loss of competitive advantage had led to an overabundance of dollars in foreign hands. Nations like France and West Germany began exchanging their dollar reserves for gold, causing a severe drain on U.S. gold stocks, which fell from over $20 billion in the 1950s to roughly $10 billion by 1971.

Domestically, President Richard Nixon was confronting "stagflation"—a troubling combination of rising inflation and economic stagnation. The fixed exchange rate system was seen as a constraint, as it prevented the devaluation of the dollar to make U.S. exports more competitive. Facing a run on gold and pressure on the dollar, Nixon convened his top economic advisors at Camp David in secret. On August 15, 1971, he announced a sweeping New Economic Policy, with its centerpiece being the unilateral suspension of the dollar's convertibility into gold. This dramatic move, known as the "Nixon Shock," effectively ended the Bretton Woods system and severed the final link between major world currencies and a tangible gold standard.

The immediate aftermath saw the world's currencies transition to a regime of floating exchange rates, where market forces largely determined their value. While the move protected U.S. gold reserves and provided short-term economic stimulus, it also ushered in an era of greater currency volatility and global inflation in the following years. The decision fundamentally reshaped the global financial order, establishing the U.S. dollar as a fiat currency—backed by government decree and confidence in the U.S. economy rather than by gold—and cementing its role as the world's dominant reserve currency.

Domestically, President Richard Nixon was confronting "stagflation"—a troubling combination of rising inflation and economic stagnation. The fixed exchange rate system was seen as a constraint, as it prevented the devaluation of the dollar to make U.S. exports more competitive. Facing a run on gold and pressure on the dollar, Nixon convened his top economic advisors at Camp David in secret. On August 15, 1971, he announced a sweeping New Economic Policy, with its centerpiece being the unilateral suspension of the dollar's convertibility into gold. This dramatic move, known as the "Nixon Shock," effectively ended the Bretton Woods system and severed the final link between major world currencies and a tangible gold standard.

The immediate aftermath saw the world's currencies transition to a regime of floating exchange rates, where market forces largely determined their value. While the move protected U.S. gold reserves and provided short-term economic stimulus, it also ushered in an era of greater currency volatility and global inflation in the following years. The decision fundamentally reshaped the global financial order, establishing the U.S. dollar as a fiat currency—backed by government decree and confidence in the U.S. economy rather than by gold—and cementing its role as the world's dominant reserve currency.

🌱 Very Common