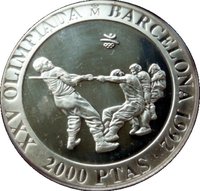

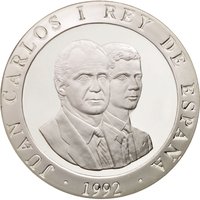

2000 Pesetas – Spain

Spain

Context

Year: 1992

Issuer: Spain

Ruler: Juan Carlos I

Currency:

(1868—2001)

Demonetization: 31 December 2001

Total mintage: 50,000

Material

References

KM: #Click to copy to clipboard914

Numista: #68946

Value

Exchange value: 2000 ESP

Bullion value: $69.23

Inflation-adjusted value: 4841.02 ESP

Obverse

Reverse

Edge

Segmented reeding (BU)Reeded (Proof)

Categories

| Animal> Horse |

| Sport> Summer Olympic Games |

Mints

| Name | Mark |

|---|---|

| Royal Mint of Madrid | (M) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1992 | M | 13,000 | BU | |

| 1992 | M | 37,000 | Proof |

Historical background

In 1992, Spain's currency situation was defined by its pivotal yet strained participation in the European Exchange Rate Mechanism (ERM), the system designed to stabilize European currencies ahead of Economic and Monetary Union. The Spanish peseta had entered the ERM in 1989, committing to maintain its value within a narrow band against a basket of European currencies, most importantly the German Deutsche Mark. This policy was intended to import the anti-inflationary credibility of the Bundesbank, but it created significant tension as Spain's economic cycle diverged from Germany's following German reunification.

The core problem was a stark policy mismatch. To combat the inflationary effects of reunification, the Bundesbank raised interest rates aggressively. Spain, however, was mired in a recession with high unemployment, requiring lower rates to stimulate growth. To maintain the peseta's ERM parity, the Banco de España was forced to keep Spanish interest rates painfully high, exacerbating the domestic economic downturn. This situation made the peseta a target for currency speculators, who bet that Spain would be unable or unwilling to sustain the economic pain necessary to defend its fixed exchange rate.

The pressures culminated in the autumn of 1992 during the broader European currency crisis. After massive speculative attacks, the peseta was devalued within the ERM by 5% on September 17, coinciding with the devaluation of the Italian lira and the UK's exit from the mechanism. A second devaluation of 6% followed in November. These events humiliated the Spanish government but ultimately provided necessary economic relief, freeing monetary policy to address the domestic recession and highlighting the difficulties of fixed exchange rates without full fiscal and political integration.

The core problem was a stark policy mismatch. To combat the inflationary effects of reunification, the Bundesbank raised interest rates aggressively. Spain, however, was mired in a recession with high unemployment, requiring lower rates to stimulate growth. To maintain the peseta's ERM parity, the Banco de España was forced to keep Spanish interest rates painfully high, exacerbating the domestic economic downturn. This situation made the peseta a target for currency speculators, who bet that Spain would be unable or unwilling to sustain the economic pain necessary to defend its fixed exchange rate.

The pressures culminated in the autumn of 1992 during the broader European currency crisis. After massive speculative attacks, the peseta was devalued within the ERM by 5% on September 17, coinciding with the devaluation of the Italian lira and the UK's exit from the mechanism. A second devaluation of 6% followed in November. These events humiliated the Spanish government but ultimately provided necessary economic relief, freeing monetary policy to address the domestic recession and highlighting the difficulties of fixed exchange rates without full fiscal and political integration.

Series: 1992 Summer Olympics, Barcelona

⭐ Somewhat Rare