20 Kwanzas – Angola

Circulating commemorative coins

Commemoration: Queen Njinga A Mbande (1582-1663)

Angola

Obverse

Description:

Portrait of Queen Njinga facing right.

Inscription:

REPÚBLICA DE ANGOLA

1582 1663

RAINHA NJINGA A MBANGE

1582 1663

RAINHA NJINGA A MBANGE

Translation:

REPUBLIC OF ANGOLA

1582 1663

QUEEN NJINGA OF MBANDE

1582 1663

QUEEN NJINGA OF MBANDE

Script: Latin

Languages: Portuguese, Kimbundu

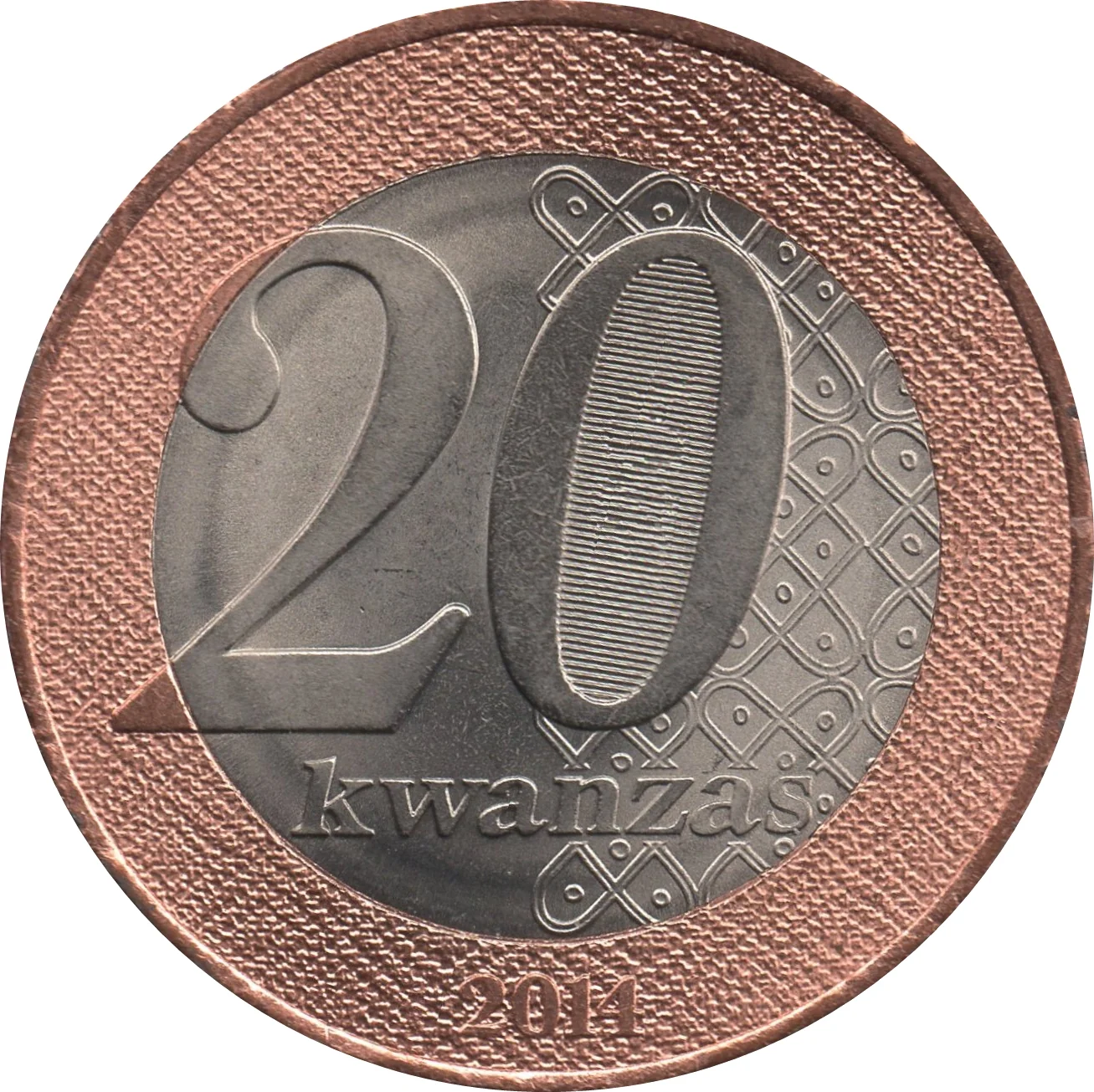

Reverse

Description:

Large "20" with "BNA" inside the zero, set within a textile-patterned border.

Inscription:

20

kwanzas

2014

kwanzas

2014

Script: Latin

Edge

Reeded Sections

Categories

| Event> Death anniversary |

| Person> Monarch |

Mints

| Name | Mark |

|---|---|

| Moscow Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2014 | — | — |

Historical background

In 2014, Angola's currency situation was defined by significant pressure on the kwanza (AOA) and a heavy reliance on oil revenues, which accounted for over 95% of export earnings and roughly 70% of government income. The year was marked by a sharp decline in global oil prices beginning in mid-2014, which exposed the structural vulnerabilities of the Angolan economy. This external shock rapidly depleted foreign exchange reserves and created a growing imbalance between the official exchange rate, pegged to the US dollar by the National Bank of Angola (BNA), and a thriving black-market rate where the kwanza was far weaker.

The government's response was a classic "defend the peg" strategy, which included draining reserves to support the official rate and implementing strict capital controls to limit dollar outflows. These controls made it extremely difficult for businesses to access foreign currency for importing essential goods, from machinery to foodstuffs, leading to widespread shortages and fueling inflation. Consequently, a large parallel market for dollars emerged, creating a multi-tiered currency system where the privileged with connections accessed dollars at the strong official rate while most others faced a much weaker informal rate, distorting the entire economy.

By the end of 2014, the unsustainable pressure was clear. The disparity between the official and parallel market rates widened dramatically, foreign reserves continued to fall, and inflation was accelerating. This tense environment set the stage for the major devaluations and monetary policy shifts that would follow in 2015, as the BNA began to reluctantly adjust the peg in the face of persistent low oil prices. The year 2014 thus represented the beginning of a prolonged currency crisis, highlighting the profound risks of an economy overwhelmingly dependent on a single volatile commodity.

The government's response was a classic "defend the peg" strategy, which included draining reserves to support the official rate and implementing strict capital controls to limit dollar outflows. These controls made it extremely difficult for businesses to access foreign currency for importing essential goods, from machinery to foodstuffs, leading to widespread shortages and fueling inflation. Consequently, a large parallel market for dollars emerged, creating a multi-tiered currency system where the privileged with connections accessed dollars at the strong official rate while most others faced a much weaker informal rate, distorting the entire economy.

By the end of 2014, the unsustainable pressure was clear. The disparity between the official and parallel market rates widened dramatically, foreign reserves continued to fall, and inflation was accelerating. This tense environment set the stage for the major devaluations and monetary policy shifts that would follow in 2015, as the BNA began to reluctantly adjust the peg in the face of persistent low oil prices. The year 2014 thus represented the beginning of a prolonged currency crisis, highlighting the profound risks of an economy overwhelmingly dependent on a single volatile commodity.

🌱 Common