50 centimos – Costa Rica

Add to wishlist

Costa Rica

Context

Years: 1982–1990

Issuer: Costa Rica

Issuing organization: Central Bank of Costa Rica

Period:

(since 1948)

Currency:

(since 1896)

Demonetized: Yes

Total mintage: 102,000,000

Material

Diameter: 19 mm

Weight: 2.2 g

Thickness: 1.1 mm

Shape: Round

Composition: Stainless steel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #6833

Value

Exchange value: 0.50 CRC

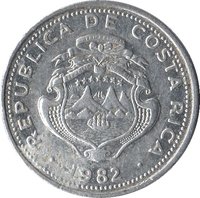

Obverse

Description:

Costa Rica's coat of arms features seven stars for its provinces, three volcanoes for its mountain ranges, and two ships between oceans, with a sunrise. Design details like letter spacing, rim style, and ship size vary.

Inscription:

REPUBLICA DE COSTA RICA

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

1983

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

1983

Translation:

REPUBLIC OF COSTA RICA

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

1983

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

1983

Script: Latin

Language: Spanish

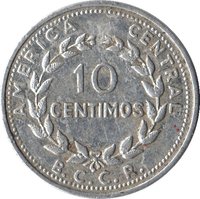

Reverse

Edge

Plain

Categories

| Transportation> Watercraft |

| Geography> Mountain |

| Symbols> Coat of Arms |

| Symbol> Wreath |

Mints

| Name | Mark |

|---|---|

| Casa da Moeda do Brasil | — |

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1982 | — | 12,000,000 | ||

| 1983 | — | 24,000,000 | ||

| 1984 | — | 42,000,000 | ||

| 1990 | — | 24,000,000 |

Historical background

In 1982, Costa Rica faced a severe currency and economic crisis, marking one of the most difficult periods in its modern financial history. The nation was grappling with the compounded effects of the 1979 oil shock, a global recession that slashed demand for its key exports like coffee and bananas, and a legacy of high public spending and foreign borrowing from the 1970s. This perfect storm led to a massive balance of payments deficit, critically low international reserves, and an unsustainable external debt burden, pushing the country to the brink of default.

The currency situation was characterized by a profound overvaluation of the Costa Rican colón under a rigid fixed exchange rate system. The official rate was artificially maintained, creating a wide and growing gap with the black-market rate, which reflected the currency's true depreciated value. This disparity fueled capital flight, crippled legitimate exports, and created severe distortions in the economy. By late 1981, the government had exhausted its reserves defending the peg, leading to a foreign exchange crisis where essential imports, including medicines and spare parts, became scarce.

In response, the government of President Luis Alberto Monge, inaugurated in May 1982, was forced to implement drastic stabilization measures under guidance from the International Monetary Fund (IMF). The cornerstone was a major devaluation of the colón and the abandonment of the fixed exchange rate in favor of a crawling peg system, allowing for periodic adjustments. This was accompanied by painful austerity, including cuts to public subsidies and social spending. These actions, while stabilizing the currency and restoring IMF and international creditor confidence, came at a significant social cost, plunging many Costa Ricans into poverty and setting the stage for a long and difficult period of economic adjustment.

The currency situation was characterized by a profound overvaluation of the Costa Rican colón under a rigid fixed exchange rate system. The official rate was artificially maintained, creating a wide and growing gap with the black-market rate, which reflected the currency's true depreciated value. This disparity fueled capital flight, crippled legitimate exports, and created severe distortions in the economy. By late 1981, the government had exhausted its reserves defending the peg, leading to a foreign exchange crisis where essential imports, including medicines and spare parts, became scarce.

In response, the government of President Luis Alberto Monge, inaugurated in May 1982, was forced to implement drastic stabilization measures under guidance from the International Monetary Fund (IMF). The cornerstone was a major devaluation of the colón and the abandonment of the fixed exchange rate in favor of a crawling peg system, allowing for periodic adjustments. This was accompanied by painful austerity, including cuts to public subsidies and social spending. These actions, while stabilizing the currency and restoring IMF and international creditor confidence, came at a significant social cost, plunging many Costa Ricans into poverty and setting the stage for a long and difficult period of economic adjustment.

🌱 Very Common