2 milliemes – Libya

Add to wishlist

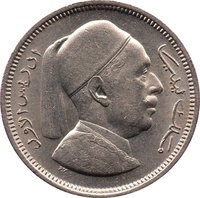

Libya

Obverse

Description:

Idris I, right-facing

Inscription:

إدريس الأول ملك ليبيا

P.V.

P.V.

Translation:

Idris I King of Libya

P.V.

P.V.

Language: Arabic

Engraver: Paul Vincze

Reverse

Description:

Crown over wreath with value above date.

Inscription:

٢

مليمان

١٩٥٢

مليمان مليمان

TWO MILLIÈMES

مليمان

١٩٥٢

مليمان مليمان

TWO MILLIÈMES

Translation:

Two Milliemes

1952

Milliemes Milliemes

1952

Milliemes Milliemes

Language: Arabic

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1952 | — | 6,650,000 | ||

| 1952 | — | 32 | Proof |

Historical background

Following its independence in 1951, the Kingdom of Libya faced the immediate and complex challenge of establishing a unified national currency. The territory, formed from the former Italian colonies of Tripolitania and Cyrenaica and the French-administered Fezzan, was a mosaic of circulating currencies. The Italian lira, the British military authority pound (used in Tripolitania and Cyrenaica), the Algerian franc (used in Fezzan), and even the Egyptian pound all competed in daily transactions, creating significant economic confusion and hindering trade and governance.

To resolve this, the new government, with crucial technical assistance from the United Nations, moved swiftly. The Libyan Currency Commission was established in 1951, empowered to issue a distinct national currency. In 1952, the Libyan pound (often abbreviated as £L) was introduced, replacing the multitude of foreign currencies at fixed rates. It was pegged to the British pound sterling at par (1:1), a reflection of both the British administrative legacy and the desire for stability through linkage to a major international reserve currency.

The successful introduction of the Libyan pound in 1952 was a foundational achievement for the young state. It symbolized tangible economic sovereignty, provided a critical tool for unified fiscal policy, and laid the necessary monetary groundwork for national development. This single currency system facilitated internal trade, simplified government budgeting and revenue collection, and marked Libya's first major step toward a coherent national economy.

To resolve this, the new government, with crucial technical assistance from the United Nations, moved swiftly. The Libyan Currency Commission was established in 1951, empowered to issue a distinct national currency. In 1952, the Libyan pound (often abbreviated as £L) was introduced, replacing the multitude of foreign currencies at fixed rates. It was pegged to the British pound sterling at par (1:1), a reflection of both the British administrative legacy and the desire for stability through linkage to a major international reserve currency.

The successful introduction of the Libyan pound in 1952 was a foundational achievement for the young state. It symbolized tangible economic sovereignty, provided a critical tool for unified fiscal policy, and laid the necessary monetary groundwork for national development. This single currency system facilitated internal trade, simplified government budgeting and revenue collection, and marked Libya's first major step toward a coherent national economy.

Series: 1952 Libya circulation coins

🌱 Common