20 Sen – Brunei

Brunei

Context

Years: 1977–1993

Issuer: Brunei

Ruler: Hassanal Bolkiah

Currency:

(since 1967)

Total mintage: 22,397,000

Material

References

KM: #Click to copy to clipboard18

Numista: #6802

Value

Exchange value: 0.20 BND

Obverse

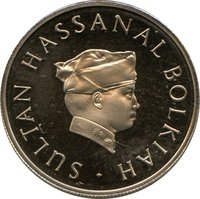

Description:

Sultan Hassanal Bolkiah of Brunei facing right.

Inscription:

SULTAN HASSANAL BOLKIAH ·

Script: Latin

Reverse

Description:

A vertical oblong design featuring a local tree motif, year, and denomination. "Government of Brunei."

Inscription:

KERAJAAN BRUNEI 1979

· 20 SEN ·

· 20 SEN ·

Script: Latin

Engraver: Christopher Ironside

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

| Singapore Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1977 | — | 1,200,000 | ||

| 1978 | — | 720,000 | ||

| 1979 | — | 1,060,000 | ||

| 1979 | — | 10,000 | Proof | |

| 1980 | — | 1,540,000 | ||

| 1981 | — | 2,140,000 | ||

| 1982 | — | 120,000 | ||

| 1983 | — | 1,350,000 | ||

| 1984 | — | 750,000 | ||

| 1984 | — | 3,000 | Proof | |

| 1985 | — | 1,000,000 | ||

| 1985 | — | — | Proof | |

| 1986 | — | 2,639,000 | ||

| 1986 | — | 7,000 | Proof | |

| 1987 | — | 2,400,000 | ||

| 1988 | — | 560,000 | ||

| 1989 | — | 500,000 | ||

| 1990 | — | 720,000 | ||

| 1991 | — | 725,000 | ||

| 1992 | — | 2,432,000 | ||

| 1993 | — | 2,521,000 |

Historical background

In 1977, Brunei's currency situation was fundamentally defined by its long-standing and exclusive monetary integration with Singapore. Since 1967, the two nations, alongside Malaysia until 1973, participated in the Currency Interchangeability Agreement. This meant the Brunei dollar and the Singapore dollar were pegged at par (1:1) and were mutually accepted as customary tender within each other's territories. For Brunei, a small protectorate not yet fully independent, this arrangement provided immediate monetary stability and credibility by anchoring its currency to the larger and more diversified Singaporean economy, which managed the shared foreign exchange reserves.

The system operated smoothly in 1977, underpinning Brunei's growing economic confidence as it harnessed immense revenues from its burgeoning oil and liquefied natural gas (LNG) exports. The petrodollar wealth, managed by the Brunei Investment Agency (established in 1983), meant the Sultanate faced no balance of payments pressures and maintained substantial foreign reserves. This financial strength negated any need to reconsider the currency arrangement, as Brunei benefited from Singapore's disciplined monetary policy and established financial infrastructure without the administrative burden of managing an independent central bank or exchange rate policy.

Therefore, the backdrop of 1977 was one of exceptional stability and passive benefit. The currency interchangeability provided a secure platform for economic planning and international trade, while the nation's hydrocarbon wealth insulated it from external shocks. This successful arrangement solidified a path dependency, setting the stage for its continuation long after Brunei's full independence in 1984, remaining a cornerstone of its financial policy to the present day.

The system operated smoothly in 1977, underpinning Brunei's growing economic confidence as it harnessed immense revenues from its burgeoning oil and liquefied natural gas (LNG) exports. The petrodollar wealth, managed by the Brunei Investment Agency (established in 1983), meant the Sultanate faced no balance of payments pressures and maintained substantial foreign reserves. This financial strength negated any need to reconsider the currency arrangement, as Brunei benefited from Singapore's disciplined monetary policy and established financial infrastructure without the administrative burden of managing an independent central bank or exchange rate policy.

Therefore, the backdrop of 1977 was one of exceptional stability and passive benefit. The currency interchangeability provided a secure platform for economic planning and international trade, while the nation's hydrocarbon wealth insulated it from external shocks. This successful arrangement solidified a path dependency, setting the stage for its continuation long after Brunei's full independence in 1984, remaining a cornerstone of its financial policy to the present day.

Series: 1977 Brunei circulation coins

🌱 Very Common