5 florin – Aruba

Add to wishlist

Netherlands

Context

Material

Diameter: 23.45 mm

Weight: 8.4 g

Thickness: 2.7 mm

Shape: Round

Composition: Aluminium bronze

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #67080

Value

Exchange value: 5 AWG

Inflation-adjusted value: 6.56 AWG

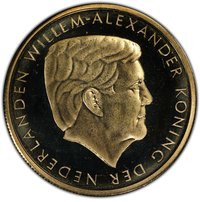

Obverse

Description:

State, coat-of-arms, mint mark, value, year.

Inscription:

ARUBA

2016

5

FLORIN

2016

5

FLORIN

Translation:

ARUBA

2016

5

FLORIN

2016

5

FLORIN

Script: Latin

Languages: English, Papiamento

Reverse

Edge

Reeded edges with smooth center channel containing inscription

Legend:

GOD ZIJ MET ONS

Translation:

God be with us

Language: Dutch

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Dutch Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2014 | — | — | ||

| 2015 | — | — | ||

| 2016 | — | — | ||

| 2023 | — | — |

Historical background

In 2014, Aruba's currency situation was defined by its longstanding and stable use of the Aruban florin (AWG), which has been pegged to the United States dollar at a fixed rate of 1.79 AWG to 1 USD since 1986. This peg, managed by the Central Bank of Aruba (CBA), provided a crucial anchor for price stability and economic predictability on the island. The system functioned through a currency board-like arrangement, requiring foreign reserve backing for the local currency in circulation, which helped maintain strong international confidence and facilitated the vital tourism and trade sectors, both heavily oriented toward the U.S. economy.

The year 2014 saw this regime face ongoing, but manageable, pressures. The global financial crisis of 2008-2009 and subsequent recessions had impacted Aruba's key tourism industry, leading to budget deficits and a gradual decline in the official foreign exchange reserves that back the currency peg. While reserves remained at adequate levels, the Central Bank of Aruba continued to emphasize the need for fiscal discipline to sustain the peg. The government's efforts to consolidate public finances were viewed as essential to maintaining the credibility of the fixed exchange rate, which was considered non-negotiable for the island's economic stability.

Consequently, monetary policy in 2014 was largely subordinated to maintaining the dollar peg, limiting the Central Bank's ability to use interest rates for domestic stimulus. The focus remained on preserving sufficient foreign reserves and managing liquidity within the banking system. The stable exchange rate continued to benefit the import-dependent economy by controlling inflation and providing certainty for businesses and investors, even as it required careful economic management to address underlying fiscal challenges and ensure the peg's long-term sustainability.

The year 2014 saw this regime face ongoing, but manageable, pressures. The global financial crisis of 2008-2009 and subsequent recessions had impacted Aruba's key tourism industry, leading to budget deficits and a gradual decline in the official foreign exchange reserves that back the currency peg. While reserves remained at adequate levels, the Central Bank of Aruba continued to emphasize the need for fiscal discipline to sustain the peg. The government's efforts to consolidate public finances were viewed as essential to maintaining the credibility of the fixed exchange rate, which was considered non-negotiable for the island's economic stability.

Consequently, monetary policy in 2014 was largely subordinated to maintaining the dollar peg, limiting the Central Bank's ability to use interest rates for domestic stimulus. The focus remained on preserving sufficient foreign reserves and managing liquidity within the banking system. The stable exchange rate continued to benefit the import-dependent economy by controlling inflation and providing certainty for businesses and investors, even as it required careful economic management to address underlying fiscal challenges and ensure the peg's long-term sustainability.

🌱 Fairly Common