¼ Dollar – United States

Circulating commemorative coins

Commemoration: South Dakota

United States

Context

Year: 2006

Issuer: United States

Period:

(since 1776)

Currency:

(since 1785)

Subdivision: ¼ Dollar = 25 Cents

Total mintage: 513,682,428

Material

References

KM: #Click to copy to clipboard386

Numista: #643

Value

Exchange value: ¼ USD = $0.25

Inflation-adjusted value: 0.41 USD

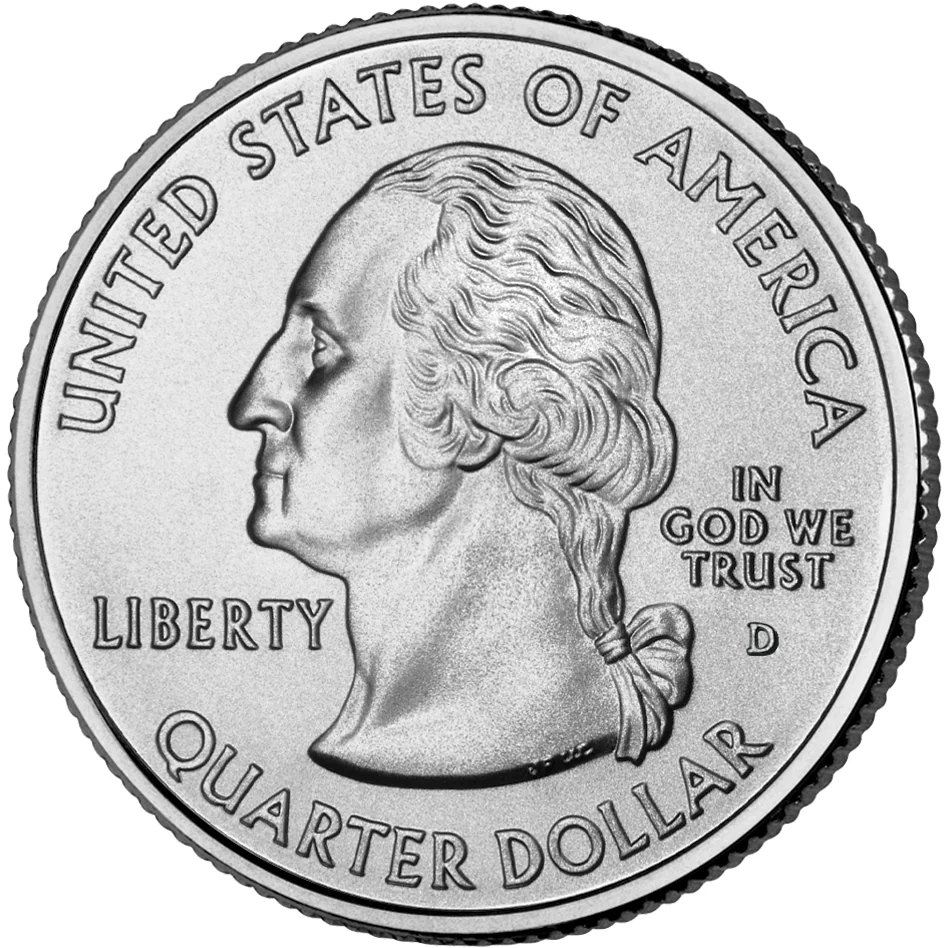

Obverse

Description:

Left-profile portrait of George Washington with "IN GOD WE TRUST" and "LIBERTY," surrounded by the face value and "UNITED STATES OF AMERICA."

Inscription:

UNITED STATES OF AMERICA

IN

GOD WE

TRUST

LIBERTY S

JF WC

QUARTER DOLLAR

IN

GOD WE

TRUST

LIBERTY S

JF WC

QUARTER DOLLAR

Script: Latin

Engravers: John Flanagan, William Cousins

Reverse

Description:

Mount Rushmore, the Ring-necked Pheasant, and wheat.

Inscription:

SOUTH DAKOTA

1889

JM

2006

E PLURIBUS UNUM

1889

JM

2006

E PLURIBUS UNUM

Translation:

SOUTH DAKOTA

1889

JM

2006

OUT OF MANY, ONE

1889

JM

2006

OUT OF MANY, ONE

Script: Latin

Engravers: John Mercanti, Michael Leidel

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| United States Mint of Denver | D |

| United States Mint of Philadelphia | P |

| United States Mint of San Francisco | S |

Historical background

In 2006, the United States currency situation was characterized by a period of relative stability for the U.S. dollar on foreign exchange markets, but underlying concerns about long-term fiscal health were growing. The dollar experienced a modest decline against major currencies like the euro, but this was part of a controlled, multi-year adjustment rather than a crisis. This environment was largely shaped by the Federal Reserve, which, under Chairman Ben Bernanke, had concluded a two-year cycle of interest rate hikes, bringing the federal funds rate to 5.25% by mid-year. This policy aimed to cool an overheating housing market and contain inflationary pressures, which were being fueled by high energy prices.

Domestically, the economy was in a transitional phase. While GDP growth remained positive, the housing market—which had been a primary engine of growth—was showing clear signs of peaking and beginning its downturn. The subprime mortgage crisis was emerging but was not yet recognized as a systemic threat. Inflation hovered around 3-4%, driven largely by rising costs for oil and commodities, which kept the Federal Reserve vigilant about price stability even as growth showed signs of moderating.

Looking outward, the U.S. continued to finance significant current account and trade deficits through substantial capital inflows from foreign investors and central banks, particularly from Asia. This "global savings glut" helped maintain demand for dollar-denominated assets like Treasury bonds, keeping long-term interest rates relatively low despite Fed tightening. However, economists and policymakers increasingly warned that these persistent imbalances—large deficits coupled with rising debt—posed a risk to the dollar's value and global financial stability in the longer term, setting the stage for the severe stresses that would emerge in 2007-2008.

Domestically, the economy was in a transitional phase. While GDP growth remained positive, the housing market—which had been a primary engine of growth—was showing clear signs of peaking and beginning its downturn. The subprime mortgage crisis was emerging but was not yet recognized as a systemic threat. Inflation hovered around 3-4%, driven largely by rising costs for oil and commodities, which kept the Federal Reserve vigilant about price stability even as growth showed signs of moderating.

Looking outward, the U.S. continued to finance significant current account and trade deficits through substantial capital inflows from foreign investors and central banks, particularly from Asia. This "global savings glut" helped maintain demand for dollar-denominated assets like Treasury bonds, keeping long-term interest rates relatively low despite Fed tightening. However, economists and policymakers increasingly warned that these persistent imbalances—large deficits coupled with rising debt—posed a risk to the dollar's value and global financial stability in the longer term, setting the stage for the severe stresses that would emerge in 2007-2008.

🌱 Very Common