2 euro (Galileo Galilei) – Italy

Add to wishlist

Circulating commemorative coins

Commemoration: 450th Anniversary of the Birth of Galileo Galilei

Italy

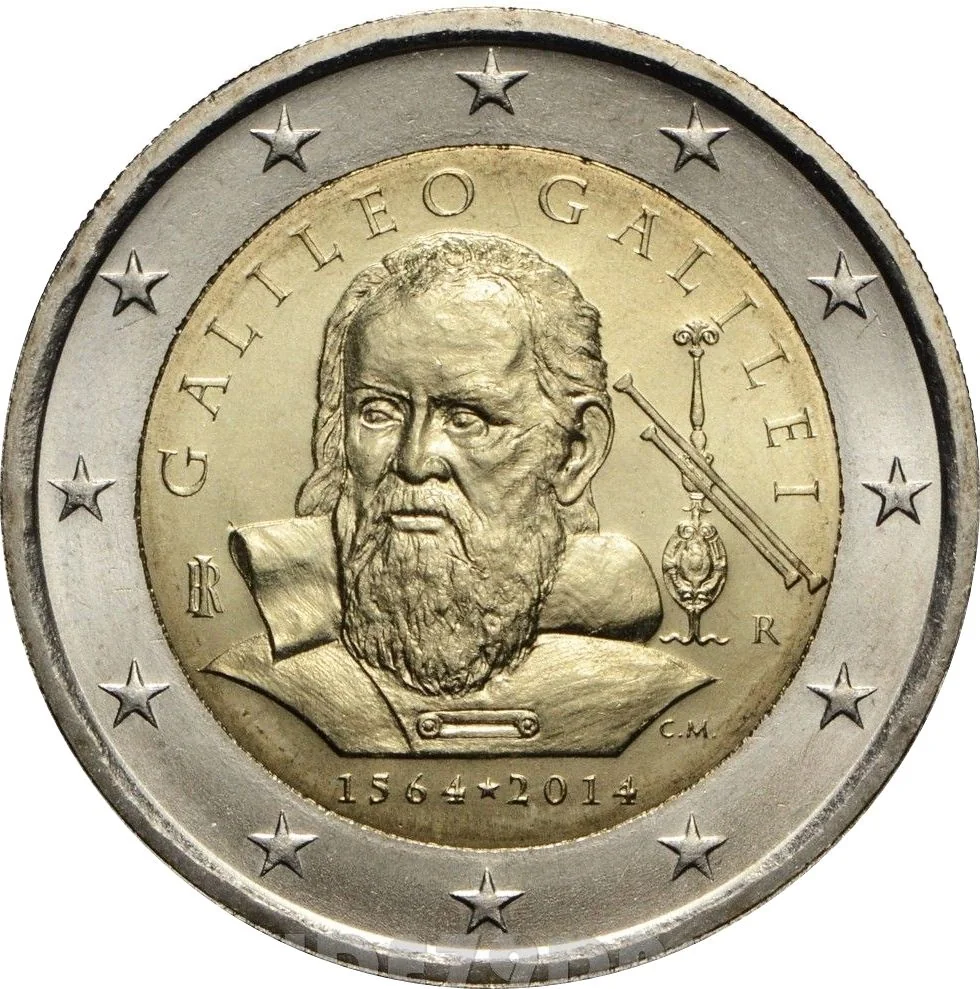

Obverse

Description:

Galileo's portrait from Sustermans' 1636 painting. Above: GALILEO GALILEI. Right: Rome mint mark/telescope/author monogram. Left: Italian Republic monogram 'RI'. Below: 1564-2014. Outer ring features the 12 EU stars.

Inscription:

GALILEO GALILEI

RI R

C.M.

1564·2014

RI R

C.M.

1564·2014

Translation:

GALILEO GALILEI

KING OF ROME

C.M.

1564·2014

KING OF ROME

C.M.

1564·2014

Script: Latin

Engraver: Claudia Momoni

Reverse

Edge

Finely ribbed with edge lettering: six times the sequence "2 * * " alternately upright and inverted

Legend:

2 * 2 * 2 * 2 * 2 * 2 *

Categories

| Event> Birth anniversary |

| Map |

| Science |

Mints

| Name | Mark |

|---|---|

| Rome | R |

Historical background

In 2014, Italy’s currency situation was defined by its membership in the Eurozone, having adopted the euro (EUR) in 1999 (physically in 2002). The country was therefore subject to the monetary policy set by the European Central Bank (ECB), which focused on low inflation and price stability for the entire currency bloc. This framework removed Italy's ability to devalue its own currency or set independent interest rates, tools that could have been used to boost competitiveness during a period of economic stagnation. The primary financial context was the aftermath of the Eurozone sovereign debt crisis, with Italy under significant market pressure due to its massive public debt, which exceeded 130% of GDP.

Domestically, the currency situation was a point of political and public debate. The prolonged recession following the 2008 global financial crisis and the 2011-2012 debt crisis fueled a rise in euroscepticism. Some political figures and segments of the public questioned the benefits of the euro, arguing that the fixed exchange rate and tight monetary policy hampered Italy's recovery and export potential by keeping the currency stronger than a hypothetical reinstated lira might have been. However, a return to a national currency was widely seen as economically catastrophic, likely triggering capital flight, a debt crisis (as most debt was denominated in euros), and severe inflation.

The year 2014 saw a shift as the ECB, under new President Mario Draghi, moved toward more aggressive monetary stimulus to combat deflationary risks and support the fragile Eurozone economy. This included cutting key interest rates to historic lows and announcing plans for quantitative easing (QE), which was ultimately launched in early 2015. These actions helped lower Italy's sovereign borrowing costs and provided crucial liquidity, temporarily easing the immediate pressure on the currency union and offering Italy some breathing room for much-needed structural reforms, which remained largely unaddressed.

Domestically, the currency situation was a point of political and public debate. The prolonged recession following the 2008 global financial crisis and the 2011-2012 debt crisis fueled a rise in euroscepticism. Some political figures and segments of the public questioned the benefits of the euro, arguing that the fixed exchange rate and tight monetary policy hampered Italy's recovery and export potential by keeping the currency stronger than a hypothetical reinstated lira might have been. However, a return to a national currency was widely seen as economically catastrophic, likely triggering capital flight, a debt crisis (as most debt was denominated in euros), and severe inflation.

The year 2014 saw a shift as the ECB, under new President Mario Draghi, moved toward more aggressive monetary stimulus to combat deflationary risks and support the fragile Eurozone economy. This included cutting key interest rates to historic lows and announcing plans for quantitative easing (QE), which was ultimately launched in early 2015. These actions helped lower Italy's sovereign borrowing costs and provided crucial liquidity, temporarily easing the immediate pressure on the currency union and offering Italy some breathing room for much-needed structural reforms, which remained largely unaddressed.

Series: Italy 2 euro commemoratives

🌱 Very Common