5 córdobas – Nicaragua

Add to wishlist

Non-circulating coins

Commemoration: Ibero-American Series III - Dances and Customs

Series: Ibero-American

Nicaragua

Obverse

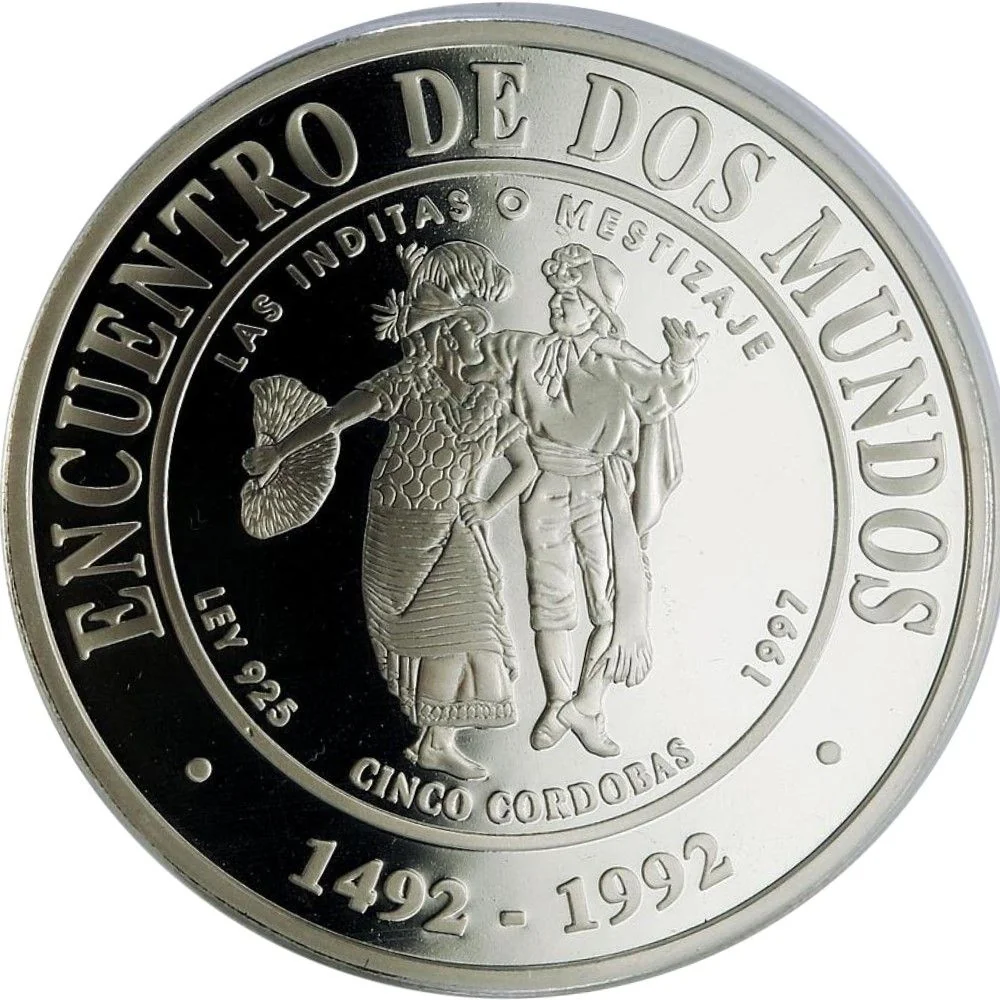

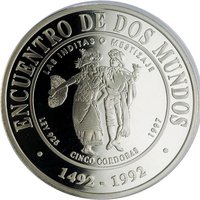

Reverse

Description:

Native woman dancing with Conquistador. Top: legend and theme. Bottom: fineness, value, date. Below: dates.

Inscription:

ENCUENTRO DE DOS MUNDOS

LAS INDITAS O MESTIZAJE

LEY 925 5 CORDOBAS 1997

1492 - 1992

LAS INDITAS O MESTIZAJE

LEY 925 5 CORDOBAS 1997

1492 - 1992

Translation:

ENCOUNTER OF TWO WORLDS

THE INDIGENOUS WOMEN OR MIXING

LAW 925 5 CORDOBAS 1997

1492 - 1992

THE INDIGENOUS WOMEN OR MIXING

LAW 925 5 CORDOBAS 1997

1492 - 1992

Script: Latin

Language: Spanish

Edge

Reeded

Categories

| Art> Dance |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint of Madrid | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1997 | — | 6,000 | Proof |

Historical background

In 1997, Nicaragua's currency situation was defined by the ongoing stabilization of the Córdoba Oro (NIO), following a period of extreme hyperinflation and economic turmoil in the late 1980s and early 1990s. A pivotal reform occurred in 1991 with the introduction of a new "gold córdoba," which was pegged to the US dollar at a fixed rate of 5:1 (5 córdobas = 1 USD) as part of a strict stabilization program under President Violeta Chamorro. By 1997, this fixed exchange rate regime remained firmly in place, providing a crucial anchor for prices and helping to curb the inflationary psychology that had devastated the economy.

The stability of the córdoba was artificially maintained by the Central Bank of Nicaragua, which required tight monetary discipline and significant foreign exchange reserves. This policy succeeded in bringing inflation down from over 13,000% in 1990 to approximately 12.4% in 1996, with it falling further to around 7.2% in 1997. However, this stability came with significant trade-offs. The overvalued fixed exchange rate made Nicaraguan exports less competitive and contributed to a persistent and growing trade deficit. The economy remained heavily dollarized, with many major transactions, bank deposits, and real estate deals conducted in US dollars, limiting the effectiveness of domestic monetary policy.

Overall, the currency situation in 1997 reflected a fragile equilibrium. While the fixed rate was hailed for ending hyperinflation and restoring basic macroeconomic order, it also masked underlying structural weaknesses. The economy was highly dependent on foreign aid and remittances to maintain the peg, and concerns were growing about the sustainability of the policy amidst low productivity and high poverty. Thus, 1997 represented a point of calibrated stability, but one that stored vulnerabilities for future economic challenges.

The stability of the córdoba was artificially maintained by the Central Bank of Nicaragua, which required tight monetary discipline and significant foreign exchange reserves. This policy succeeded in bringing inflation down from over 13,000% in 1990 to approximately 12.4% in 1996, with it falling further to around 7.2% in 1997. However, this stability came with significant trade-offs. The overvalued fixed exchange rate made Nicaraguan exports less competitive and contributed to a persistent and growing trade deficit. The economy remained heavily dollarized, with many major transactions, bank deposits, and real estate deals conducted in US dollars, limiting the effectiveness of domestic monetary policy.

Overall, the currency situation in 1997 reflected a fragile equilibrium. While the fixed rate was hailed for ending hyperinflation and restoring basic macroeconomic order, it also masked underlying structural weaknesses. The economy was highly dependent on foreign aid and remittances to maintain the peg, and concerns were growing about the sustainability of the policy amidst low productivity and high poverty. Thus, 1997 represented a point of calibrated stability, but one that stored vulnerabilities for future economic challenges.

Series: Ibero-American

💎 Very Rare