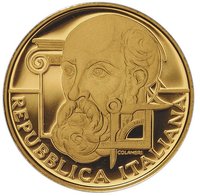

Obverse

Description:

Europe depicted as a ship sailing under the EU's twelve stars. Left: issue year. Right: "RI" monogram. Bottom center: author's name.

Inscription:

2008 RI

E. L. FRAPICCINI

E. L. FRAPICCINI

Translation:

Edward Louis Frapiccini

Script: Latin

Engraver: Ettore Lorenzo Frapiccini

Reverse

Description:

Vermeer's "The Lacemaker" masterpiece. At right, its value and mint mark.

Inscription:

EUROPA DELLE ARTI

20

EURO

R

J. VERMEER

20

EURO

R

J. VERMEER

Script: Latin

Engraver: Ettore Lorenzo Frapiccini

Edge

Categories

| Art> Painting |

| Art> Handicraft |

| Transportation> Watercraft |

Mints

| Name | Mark |

|---|---|

| Rome | R |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2008 | R | 2,011 | Proof |

Historical background

In 2008, Italy entered the global financial crisis already burdened by deep-seated economic vulnerabilities, but with a unique monetary shield: as a member of the Eurozone, it used the euro. This meant the country did not face a direct currency crisis or speculative attacks on the lira, as it had in the 1990s. However, the single currency also removed key national tools for adjustment. The Bank of Italy could not devalue the currency to boost competitiveness, nor could it set independent interest rates tailored to Italy's low-growth economy. Instead, monetary policy was set by the European Central Bank (ECB) for the entire Eurozone, which often did not align with Italy's specific needs, particularly as the crisis intensified.

The core of Italy's "currency situation" was therefore a competitiveness crisis within the Eurozone. Years of stagnant productivity, rigid labor markets, and rising unit labor costs had eroded its export competitiveness against core Eurozone partners like Germany. This loss of internal competitiveness, often called a "real exchange rate" misalignment, resulted in persistent trade deficits and sluggish growth. The euro acted as a straitjacket, locking Italy into a high-value currency regime that magnified these structural weaknesses. As the global crisis triggered a recession, these long-standing problems erupted into a sovereign debt crisis, with investor fears over high public debt (over 100% of GDP) leading to soaring borrowing costs for the Italian government.

Consequently, by the end of 2008, the situation was one of acute tension within the monetary union. Italy was reliant on the stability of the euro but was increasingly seen as a potential weak link, testing the solidarity of the Eurozone. The crisis shifted focus from currency markets to bond markets, where spreads between Italian and German government bonds (the BTP-Bund spread) widened dramatically. This marked the beginning of the European sovereign debt crisis, where Italy's struggle was not with its own currency collapsing, but with the risk of being priced out of the very currency union it depended upon, prompting eventual interventions by the ECB to preserve the euro's integrity.

The core of Italy's "currency situation" was therefore a competitiveness crisis within the Eurozone. Years of stagnant productivity, rigid labor markets, and rising unit labor costs had eroded its export competitiveness against core Eurozone partners like Germany. This loss of internal competitiveness, often called a "real exchange rate" misalignment, resulted in persistent trade deficits and sluggish growth. The euro acted as a straitjacket, locking Italy into a high-value currency regime that magnified these structural weaknesses. As the global crisis triggered a recession, these long-standing problems erupted into a sovereign debt crisis, with investor fears over high public debt (over 100% of GDP) leading to soaring borrowing costs for the Italian government.

Consequently, by the end of 2008, the situation was one of acute tension within the monetary union. Italy was reliant on the stability of the euro but was increasingly seen as a potential weak link, testing the solidarity of the Eurozone. The crisis shifted focus from currency markets to bond markets, where spreads between Italian and German government bonds (the BTP-Bund spread) widened dramatically. This marked the beginning of the European sovereign debt crisis, where Italy's struggle was not with its own currency collapsing, but with the risk of being priced out of the very currency union it depended upon, prompting eventual interventions by the ECB to preserve the euro's integrity.

Series: Europe of Arts

✨ Legendary