5 centavos – Nicaragua

Add to wishlist

Nicaragua

Context

Year: 2002

Issuer: Nicaragua

Issuing organization: Central Bank of Nicaragua

Period:

(since 1854)

Currency:

(since 1991)

Material

References

KM: #

Numista: #6097

Value

Exchange value: 0.05 NIO

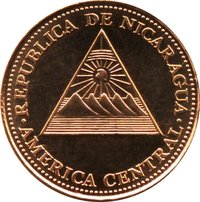

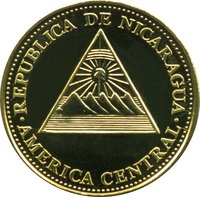

Obverse

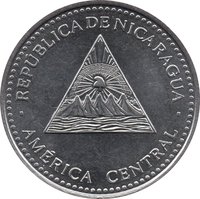

Reverse

Edge

Plain

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2002 | — | — |

Historical background

In 2002, Nicaragua's currency situation was defined by the coexistence of two legal tenders: the Nicaraguan córdoba (NIO) and the United States dollar. This official dollarization, implemented in 1991 following a period of hyperinflation and economic turmoil in the 1980s, had created a dual-currency system. The U.S. dollar served as the primary medium for large transactions, savings, and foreign trade, while the córdoba remained in circulation for everyday, small-scale purchases, particularly outside major urban centers. The Central Bank of Nicaragua maintained a crawling peg exchange rate regime, allowing the córdoba to depreciate slowly and predictably against the dollar to maintain export competitiveness.

The economy was still grappling with the aftermath of Hurricane Mitch in 1998 and a severe drought in 1999, which constrained growth and government finances. While dollarization had successfully ended hyperinflation—bringing annual inflation down to single digits—it also limited the central bank's ability to act as a lender of last resort and conduct independent monetary policy. The financial system was largely dollarized, with a significant majority of bank deposits and loans denominated in U.S. dollars, which introduced credit risks for borrowers earning income in córdobas, such as farmers and small business owners.

Overall, the currency framework in 2002 provided relative macroeconomic stability but exposed structural vulnerabilities. The fixed, crawling exchange rate required careful management of foreign reserves to maintain confidence, and the high level of financial dollarization made the economy sensitive to fluctuations in the córdoba's value. This environment set the stage for a move towards greater exchange rate flexibility, which would culminate in 2019 with the adoption of a full-fledged crawling peg system with bands, and later, in 2021, with the introduction of a new series of córdoba banknotes as part of a broader monetary reform.

The economy was still grappling with the aftermath of Hurricane Mitch in 1998 and a severe drought in 1999, which constrained growth and government finances. While dollarization had successfully ended hyperinflation—bringing annual inflation down to single digits—it also limited the central bank's ability to act as a lender of last resort and conduct independent monetary policy. The financial system was largely dollarized, with a significant majority of bank deposits and loans denominated in U.S. dollars, which introduced credit risks for borrowers earning income in córdobas, such as farmers and small business owners.

Overall, the currency framework in 2002 provided relative macroeconomic stability but exposed structural vulnerabilities. The fixed, crawling exchange rate required careful management of foreign reserves to maintain confidence, and the high level of financial dollarization made the economy sensitive to fluctuations in the córdoba's value. This environment set the stage for a move towards greater exchange rate flexibility, which would culminate in 2019 with the adoption of a full-fledged crawling peg system with bands, and later, in 2021, with the introduction of a new series of córdoba banknotes as part of a broader monetary reform.

🌱 Common