¼ dinar – Libya

Add to wishlist

Libya

Context

Year: 2014

Islamic (Hijri) Year:: 1435

Issuer: Libya

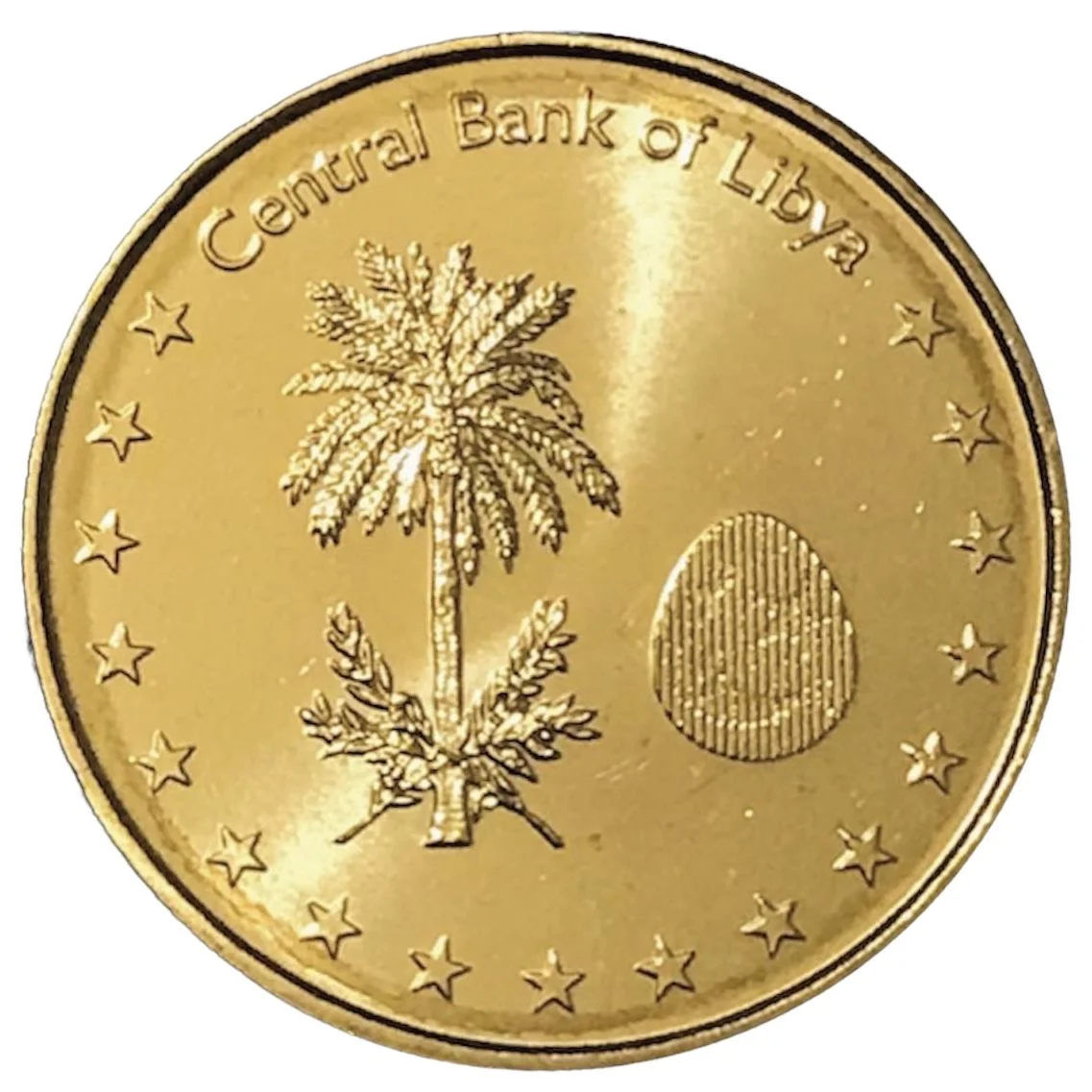

Issuing organization: Central Bank of Libya

Period:

(since 2011)

Currency:

(since 1971)

Material

Diameter: 26 mm

Weight: 6.55 g

Thickness: 2 mm

Shape: Round

Composition: Nordic gold

Magnetic: No

Techniques: Latent image, Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #58463

Value

Exchange value: ¼ LYD

Obverse

Reverse

Edge

Milled

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2014 | — | — |

Historical background

Following the 2011 revolution and the fall of the Gaddafi regime, Libya entered a period of deepening political and institutional fracture. By 2014, this division crystallized into two rival governments: the internationally recognized House of Representatives (HoR) based in the east, aligned with General Khalifa Haftar's Libyan National Army (LNA), and the General National Congress (GNC) in the west, supported by various militias in Tripoli. This political split directly paralysed the state's financial institutions, most critically the Central Bank of Libya (CBL) in Tripoli and the Libyan Investment Authority (LIA), the national sovereign wealth fund.

The currency situation became a critical battleground in this conflict. While the CBL in Tripoli maintained nominal unity and control over the printing of the Libyan dinar (LYD), rival authorities sought to access funds and leverage monetary policy. A major crisis emerged from the HoR's attempt to access oil revenues and foreign currency outside the Tripoli-based CBL's authority, leading to a blockade of key oil ports that slashed national income. Simultaneously, liquidity dried up within the country; banks faced severe shortages of cash, imposing strict withdrawal limits on citizens and businesses, while a growing black market for foreign currency, especially US dollars, flourished.

Consequently, a significant and persistent gap opened between the official exchange rate (approximately 1.25 LYD to 1 USD) and the black-market rate, which by late 2014 had depreciated to over 2.0 LYD to 1 USD. This disparity encouraged widespread corruption and arbitrage, as those with access to official rates could profit massively. The currency crisis severely eroded public purchasing power, fueled inflation for imported goods, and became a tool of economic warfare, with each political bloc attempting to control financial resources to strangle the other, ultimately deepening the humanitarian and economic distress for the Libyan population.

The currency situation became a critical battleground in this conflict. While the CBL in Tripoli maintained nominal unity and control over the printing of the Libyan dinar (LYD), rival authorities sought to access funds and leverage monetary policy. A major crisis emerged from the HoR's attempt to access oil revenues and foreign currency outside the Tripoli-based CBL's authority, leading to a blockade of key oil ports that slashed national income. Simultaneously, liquidity dried up within the country; banks faced severe shortages of cash, imposing strict withdrawal limits on citizens and businesses, while a growing black market for foreign currency, especially US dollars, flourished.

Consequently, a significant and persistent gap opened between the official exchange rate (approximately 1.25 LYD to 1 USD) and the black-market rate, which by late 2014 had depreciated to over 2.0 LYD to 1 USD. This disparity encouraged widespread corruption and arbitrage, as those with access to official rates could profit massively. The currency crisis severely eroded public purchasing power, fueled inflation for imported goods, and became a tool of economic warfare, with each political bloc attempting to control financial resources to strangle the other, ultimately deepening the humanitarian and economic distress for the Libyan population.

🌱 Common