100 dollars – Canada

Add to wishlist

Non-circulating coins

Commemoration: XVth Winter Olympic Games in Calgary, Alberta

Series: 1988 Winter Olympics, Calgary

Canada

Context

Material

References

KM: #

Numista: #58274

Value

Exchange value: 100 CAD

Bullion value: $1204.08

Inflation-adjusted value: 246.70 CAD

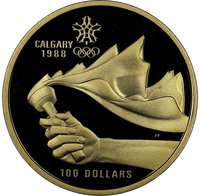

Obverse

Description:

Bust of Queen Elizabeth II at age 37, wearing a tiara and facing right.

Inscription:

ELIZABETH II CANADA 1987

Script: Latin

Designer: Arnold Machin

Reverse

Description:

Arm holding an Olympic torch; its stylized flames create mountain silhouettes, with value below.

Inscription:

CALGARY

1988

100 DOLLARS

1988

100 DOLLARS

Script: Latin

Engraver: Ago Aarand

Designer: Friedrich Peter

Edge

Lettered

Legend:

XV OLYMPIC WINTER GAMES - XVES JEUX OLYMPIQUES D'HIVER

Categories

| Sport> Winter Olympic Games |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Ottawa | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1987 | — | — | ||

| 1987 | — | 145,175 | Proof |

Historical background

In 1987, Canada's currency situation was characterized by a period of significant volatility and strategic intervention, set against the backdrop of the Plaza and Louvre Accords. Following the 1985 Plaza Accord, where major economies agreed to depreciate the US dollar, the Canadian dollar (CAD) experienced a sharp and rapid appreciation, soaring from historic lows near 69 US cents in 1986 to over 77 cents by early 1987. This surge, driven by strong commodity prices and capital inflows, threatened to undermine the competitiveness of Canadian exports, a critical pillar of the national economy. The Bank of Canada, under Governor John Crow, was thus navigating a complex environment of managing inflationary pressures while mitigating the negative trade impacts of a strong currency.

The pivotal international development was the Louvre Accord of February 1987, where G7 nations, including Canada, agreed to stabilize exchange rates and halt the US dollar's decline. For Canada, this meant committing to intervene in foreign exchange markets to keep the CAD within an undisclosed target range against the US dollar, believed to be roughly between 72 and 78 US cents. Throughout the year, the Bank of Canada actively bought US dollars to curb the CAD's strength, amassing substantial foreign exchange reserves. This period marked a clear, though temporary, shift towards a more managed float, as monetary policy was directly influenced by the exchange rate target alongside domestic inflation goals.

Domestically, the currency volatility in 1987 intersected with rising concerns over inflation and a shift in monetary policy doctrine. Governor Crow began publicly emphasizing price stability as the paramount objective, laying the groundwork for the eventual adoption of explicit inflation targets in 1991. The strong currency helped dampen import prices but also squeezed manufacturers and exporters. Consequently, 1987 stands as a transitional year where Canada actively participated in a coordinated, but ultimately unsustainable, international effort to manage exchange rates, while its own central bank was gradually moving toward a more rigid, inflation-focused mandate that would define monetary policy in the decades to follow.

The pivotal international development was the Louvre Accord of February 1987, where G7 nations, including Canada, agreed to stabilize exchange rates and halt the US dollar's decline. For Canada, this meant committing to intervene in foreign exchange markets to keep the CAD within an undisclosed target range against the US dollar, believed to be roughly between 72 and 78 US cents. Throughout the year, the Bank of Canada actively bought US dollars to curb the CAD's strength, amassing substantial foreign exchange reserves. This period marked a clear, though temporary, shift towards a more managed float, as monetary policy was directly influenced by the exchange rate target alongside domestic inflation goals.

Domestically, the currency volatility in 1987 intersected with rising concerns over inflation and a shift in monetary policy doctrine. Governor Crow began publicly emphasizing price stability as the paramount objective, laying the groundwork for the eventual adoption of explicit inflation targets in 1991. The strong currency helped dampen import prices but also squeezed manufacturers and exporters. Consequently, 1987 stands as a transitional year where Canada actively participated in a coordinated, but ultimately unsustainable, international effort to manage exchange rates, while its own central bank was gradually moving toward a more rigid, inflation-focused mandate that would define monetary policy in the decades to follow.

Series: 1988 Winter Olympics, Calgary

💎 Very Rare