3 Pence – United Kingdom

United Kingdom

Context

Years: 1927–1936

Issuer: United Kingdom

Ruler: George V

Currency:

(1158—1970)

Demonetized: Yes

Total mintage: 38,011,304

Material

References

KM: #Click to copy to clipboard831

Numista: #5650

Value

Bullion value: $2.05

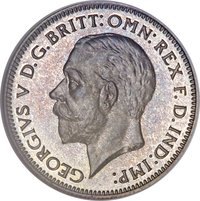

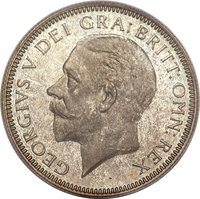

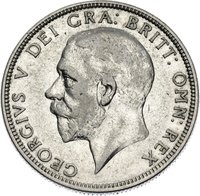

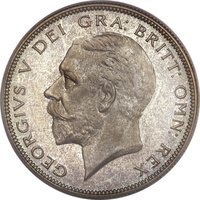

Obverse

Description:

Modified left-facing portrait of George V, encircled by legend.

Inscription:

GEORGIVS V D.G.BRITT:OMN:REX F.D.IND:IMP:

BM

BM

Translation:

George V, by the Grace of God, King of all the Britains, Defender of the Faith, Emperor of India.

Script: Latin

Language: Latin

Engraver: Edgar Bertram MacKennal

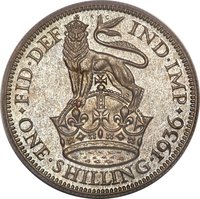

Reverse

Description:

Three oak sprigs with acorns, value above, date below.

Inscription:

THREE· ·PENCE·

G

1936

G

1936

Script: Latin

Engraver: George Kruger Gray

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1927 | — | 4 | Proof | |

| 1928 | — | 1,302,100 | ||

| 1928 | — | — | Proof | |

| 1930 | — | 1,319,400 | ||

| 1930 | — | — | Proof | |

| 1931 | — | — | Proof | |

| 1931 | — | 6,251,900 | ||

| 1932 | — | — | Proof | |

| 1932 | — | 5,887,300 | ||

| 1933 | — | 5,578,500 | ||

| 1933 | — | — | Proof | |

| 1934 | — | 7,405,900 | ||

| 1934 | — | — | Proof | |

| 1935 | — | 7,027,600 | ||

| 1935 | — | — | Proof | |

| 1936 | — | 3,238,600 | ||

| 1936 | — | — | Proof |

Historical background

In 1927, the United Kingdom's currency situation was dominated by the aftermath of its 1925 decision to return to the Gold Standard at the pre-war parity of £1 = $4.86. Championed by Chancellor of the Exchequer Winston Churchill, this move aimed to restore London's financial prestige and price stability. However, the chosen parity overvalued sterling by an estimated 10-15%, making British exports prohibitively expensive on the world market. This crippled key industries like coal, textiles, and shipbuilding, leading to stagnant growth, persistent unemployment, and social unrest, most notably the 1926 General Strike.

The policy created a difficult balancing act for the Bank of England. To maintain gold reserves and defend the fixed exchange rate, it was forced to keep interest rates relatively high, which further stifled domestic investment and economic recovery. This "hard money" stance attracted short-term capital flows but came at the cost of long-term industrial health. Consequently, the UK economy in 1927 was characterised by a stark dichotomy: financial orthodoxy and stability in the City of London contrasted sharply with industrial decline and deflationary pressure in the regions.

Internationally, the situation created tensions, particularly with the United States and France. The UK resented the lower interest rates and rising gold reserves in New York and Paris, believing the Federal Reserve and the Banque de France were not playing by the unwritten rules of the Gold Standard to ease global conditions. By 1927, these pressures led to a secret conference at Long Island, where U.S. authorities agreed to lower rates to help sterling, a temporary fix that merely postponed the system's inherent crisis. Thus, the currency regime of 1927 was fundamentally unstable, laying the groundwork for the severe financial strains that would culminate in the UK's forced abandonment of the Gold Standard in 1931.

The policy created a difficult balancing act for the Bank of England. To maintain gold reserves and defend the fixed exchange rate, it was forced to keep interest rates relatively high, which further stifled domestic investment and economic recovery. This "hard money" stance attracted short-term capital flows but came at the cost of long-term industrial health. Consequently, the UK economy in 1927 was characterised by a stark dichotomy: financial orthodoxy and stability in the City of London contrasted sharply with industrial decline and deflationary pressure in the regions.

Internationally, the situation created tensions, particularly with the United States and France. The UK resented the lower interest rates and rising gold reserves in New York and Paris, believing the Federal Reserve and the Banque de France were not playing by the unwritten rules of the Gold Standard to ease global conditions. By 1927, these pressures led to a secret conference at Long Island, where U.S. authorities agreed to lower rates to help sterling, a temporary fix that merely postponed the system's inherent crisis. Thus, the currency regime of 1927 was fundamentally unstable, laying the groundwork for the severe financial strains that would culminate in the UK's forced abandonment of the Gold Standard in 1931.

🌱 Very Common